Welcome to VanEck

Select Investor Type

20 March 2020

While the outcome of this most recent market sell-off and related pandemic are yet-to-be-seen, we remain optimistic about the outlook for gold and gold stocks in the near-term. Much of the market movement in gold prices is relatively easy to explain, while gold companies continue to exhibit, we believe, truly compelling fundamentals and valuations. With respect to the pandemic, companies are taking all precautions, and although we do anticipate that some operations will be impacted, discussions we have had with companies indicate that every effort is being made to ensure inventories, supply lines, employee health and back-up redundancies are in place to sustain production.

Below is a summary of our most recent takeaways.

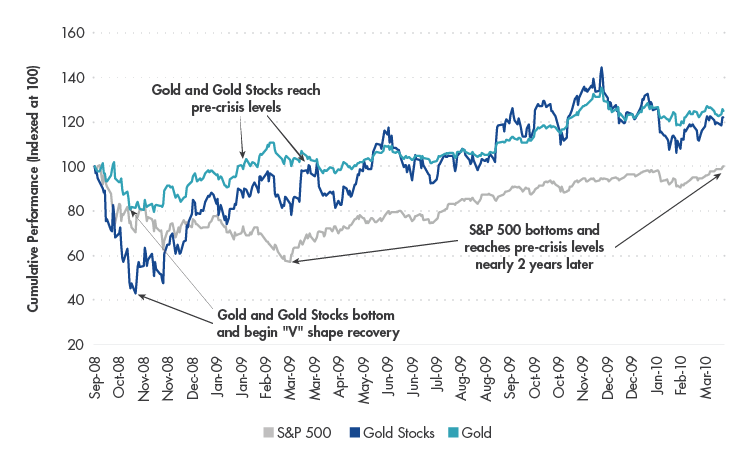

Source: VanEck, Bloomberg. Data as of March 2020. “S&P 500” represented by the S&P 500 Index TR (SPXT). “Gold Stocks” represented by the NYSE Arca Gold Miners Index Net Total Return (GDMNTR). “Gold” represented by gold spot prices.

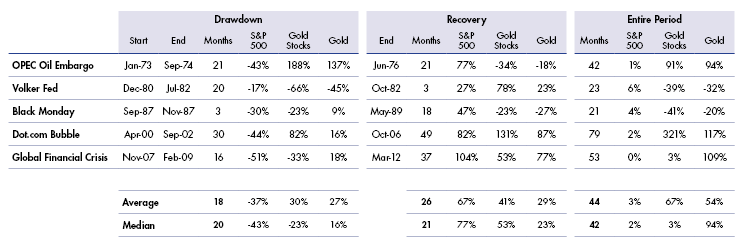

Source: VanEck, Bloomberg. Data as of March 2020. Index returns are cumulative. “S&P 500” represented by the S&P 500 TR Index (SPXT). “Gold Stocks” represented by Barron’s Gold Mining Index (BGMI) from January 1973 to inception date of the Philadelphia Gold and Silver Index (XAUTR) in January 1984 and XAUTR to the inception of the NYSE Arca Gold Miners Index Net Total Return (GDMNTR) in October 1993. “Gold” represented by gold spot prices

We believe that gold stocks, generally speaking, remain in fundamentally good shape.

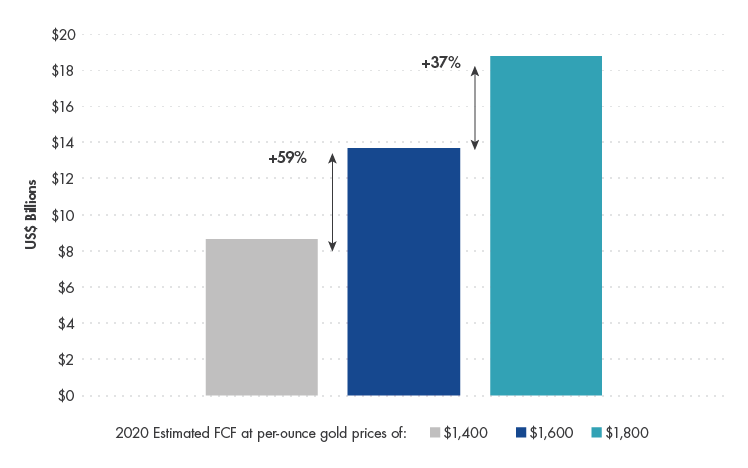

Source: VanEck, Bloomberg. Data as of March 2020. “Senior” miners defined by production levels of approximately 1.5-6.0 million ounces of gold per year (“Mid-Tier” approximately 0.3-1.5 million ounces per year).

This is a marketing communication. Please refer to the prospectus of the UCITS and to the KID before making any final investment decisions.

This information originates from VanEck (Europe) GmbH, which has been appointed as distributor of VanEck products in Europe by the Management Company VanEck Asset Management B.V., incorporated under Dutch law and registered with the Dutch Authority for the Financial Markets (AFM). VanEck (Europe) GmbH with registered address at Kreuznacher Str. 30, 60486 Frankfurt, Germany, is a financial services provider regulated by the Federal Financial Supervisory Authority in Germany (BaFin).

The information is intended only to provide general and preliminary information to investors and shall not be construed as investment, legal or tax advice VanEck (Europe) GmbH, VanEck Switzerland AG, VanEck Securities UK Limited and their associated and affiliated companies (together “VanEck”) assume no liability with regards to any investment, divestment or retention decision taken by the investor on the basis of this information. The views and opinions expressed are those of the author(s) but not necessarily those of VanEck. Opinions are current as of the publication date and are subject to change with market conditions. Certain statements contained herein may constitute projections, forecasts and other forward-looking statements, which do not reflect actual results. Information provided by third party sources is believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Brokerage or transaction fees may apply.

All performance information is based on historical data and does not predict future returns. Investing is subject to risk, including the possible loss of principal.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of VanEck.

© VanEck (Europe) GmbH / VanEck Asset Management B.V.

15 December 2025