About Defaults - Russia and More?

25 May 2022

Read Time 2 MIN

U.S. Treasury closes the debt payment loophole for Russia. EM central banks keep an eye on the policy rate differential with the U.S. Fed.

Russia Sovereign Default

The U.S. Treasury closed the loophole (a special Office of Foreign Assets Control (OFAC) waiver) that allowed U.S. banks and individuals to receive bond payments from the Russian government. With Russia’s technical default looming, some commentators argued that this creates an international precedent that can complicate the lives of sovereign borrowers down the road. An aspect that might be more relevant in the near-term is the impact on Russia’s corporate debt, which is several orders of magnitude larger than sovereign debt. Yes, it is not huge as percentage of GDP, and it is very concentrated in several sectors, but broken financing and supply chains will push Russia’s potential growth trajectory lower in the coming years.

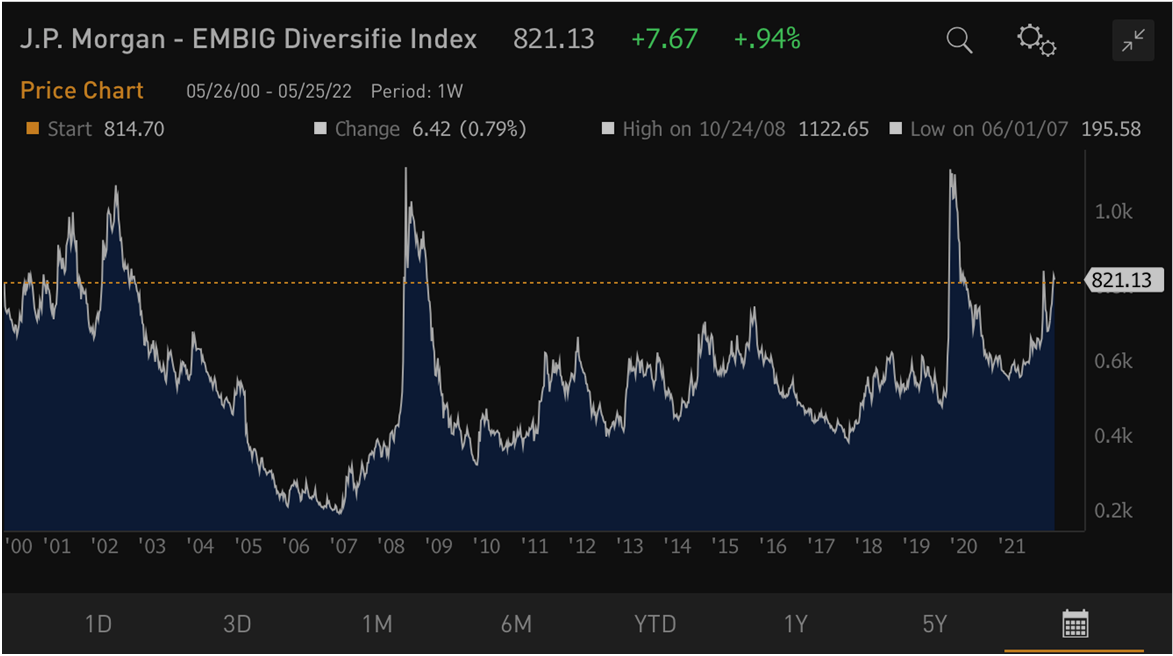

Frontier EM Spreads, Default Risks

Russia is not the only emerging markets (EM) where the default drumbeat is getting louder. Several low-income (or frontier) EMs are either in distressed territory or getting close, being hit by exogenous shocks and rising global rates. The current EM High Yield spread (J.P. Morgan’s EMBIG Diversified HY Index) is the widest since 2002/03 (with the exception of the global financial crisis and the pandemic crisis – see chart below). By contrast, EM Investment Grade spread (J.P. Morgan’s EMBIG Diversified IG Index) is still close to historic lows. Of course, individual countries’ circumstances are different (EM is not a monolith), but if the current trends continue, we expect to hear more calls to extend the G20 Common Framework for debt treatment. From the investment perspective, it is also important that several countries in this group are talking to the IMF about new programs and loans – disbursements and news about structural reforms tend to improve sentiment and compress spreads.

EM Central Banks And U.S. Fed Decoupling

And talking about rising global rates, the U.S. Federal Reserve’s (Fed’s) minutes will be scrutinized this afternoon for signs of either confirming the +50bps pace of rate hikes or perhaps expanding it to +75bps. It’s not just “we the market” who are watching the Fed – many EM central banks do the same (despite being way ahead in the current tightening cycle). Mexico’s deputy governor, Jonathan Heath, said yesterday that they cannot decouple from the Fed and might need to widen the policy rate differential in order to maintain restrictive stance. Stay tuned!

Chart at a Glance: “Fragile” EM Spreads Are Widening

Source: Bloomberg LP

Related Insights

Related Insights

10 febrero 2026

06 marzo 2025

20 febrero 2025

10 febrero 2026

La erosión del valor de la moneda vuelve a estar en el centro de atención. A continuación, analizamos qué lo está impulsando, qué podría revertirlo y cómo estamos posicionando las carteras en ambos escenarios.

07 abril 2025

Los aranceles de Trump avivan los temores de una guerra comercial, impulsando la volatilidad del mercado, el riesgo inflacionario y la amenaza de una recesión. Ante posibles represalias globales, el crecimiento a corto plazo corre un riesgo evidente.

06 marzo 2025

Los aranceles de Trump, la próxima fase de la IA y una posible revalorización del oro estadounidense podrían sacudir los mercados; los inversores que se adelanten a estas transiciones estarán mejor posicionados.

20 febrero 2025

El avance de la IA en China, la persistente inflación, el rendimiento superior del oro y el aumento de la demanda energética ponen de relieve un panorama de inversión cambiante.

16 enero 2025

En 2025, superar los problemas significa equilibrar la innovación tecnológica, las coberturas contra la inflación, los cambios energéticos y los riesgos derivados de los recortes del gasto y la inflación.