EM Inflation – Elusive Targets

03 June 2022

Read Time 2 MIN

EM inflation is now expected to peak in Q2/Q3, but return to the official targets might not happen until late 2023.

EM Inflation Peaks

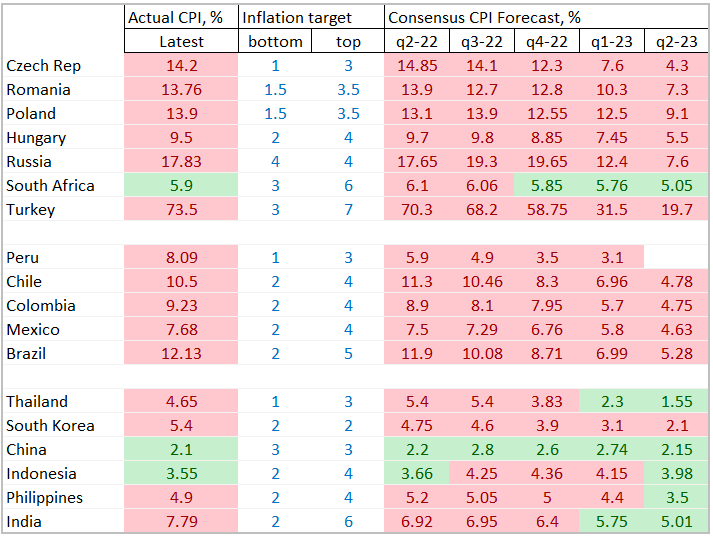

The expected emerging markets (EM) inflation peak keeps shifting to the future, with the latest consensus forecasts pointing to Q2/Q3 as the new horizon (see chart below). Ensuing disinflation – provided this scenario materializes – does not mean a speedy return to the official targets. And we are not talking about such obvious outliers as Turkey (where headline inflation surged to 73.5% year-on-year in May) or Russia. Most EMEA and LATAM are expected to stay outside the target ranges at least until the second half of 2023 – despite a supportive high base effect!

Pace Of EM Rate Hikes

The numbers provide a strong argument for the continuation of rate hikes. But they also give more ammunition to the supporters of “marathon” tightening cycles with a slower pace of rate hikes – it’s disinflation after all, and GDP growth is also moderating. Analysts often point to Brazil as an important litmus test – the central bank is expected to raise its policy rate only by 50bsp at the next meeting, despite headline inflation still in double digits. But one can also argue that Brazil is an exception rather than the rule – it has by far the highest ex-ante real policy rate among major EMs, which is already above the neutral rate (=the policy stance is actually restrictive). High real rates and the improving growth outlook suggest that Brazil’s local debt should remain an interesting proposition to EM Fixed Income investors.

EM Asia Tightening – Catching Up With The Rest Of EM

Real policy rates adjusted by expected inflation (ex-ante) are particularly low (negative) in EM Asia - a latecomer to policy tightening. Inflation still looks relatively benign compared to other regions and also compared to history, but it is grinding higher – forcing the market to adjust its policy rate expectations accordingly. Thailand is now expected to begin liftoff in the next three months. The consensus sees another rate hike (+50bps) in India next week, and the Philippines can also tighten more at the end of the month. Stay tuned!

Chart at a Glance: At Least A Year Before EM Inflation Is Back to Targets

Source: Bloomberg LP

Related Insights

Related Insights

10 febrero 2026

06 marzo 2025

20 febrero 2025

10 febrero 2026

La erosión del valor de la moneda vuelve a estar en el centro de atención. A continuación, analizamos qué lo está impulsando, qué podría revertirlo y cómo estamos posicionando las carteras en ambos escenarios.

07 abril 2025

Los aranceles de Trump avivan los temores de una guerra comercial, impulsando la volatilidad del mercado, el riesgo inflacionario y la amenaza de una recesión. Ante posibles represalias globales, el crecimiento a corto plazo corre un riesgo evidente.

06 marzo 2025

Los aranceles de Trump, la próxima fase de la IA y una posible revalorización del oro estadounidense podrían sacudir los mercados; los inversores que se adelanten a estas transiciones estarán mejor posicionados.

20 febrero 2025

El avance de la IA en China, la persistente inflación, el rendimiento superior del oro y el aumento de la demanda energética ponen de relieve un panorama de inversión cambiante.

16 enero 2025

En 2025, superar los problemas significa equilibrar la innovación tecnológica, las coberturas contra la inflación, los cambios energéticos y los riesgos derivados de los recortes del gasto y la inflación.