Global Rates – No Pause For You?

03 November 2022

Read Time 2 MIN

Global Tightening Cycles

Developed markets (DM) doves are backing off for now, following yesterday’s 75bps hike by the U.S. Federal Reserve (Fed) and Chairman Powell’s “I am the boss” press conference, which scared the daylights out of many risky assets. The Fed Funds Futures effectively added one more 25bps rate hike in 2023, bringing the expected terminal rate to 5.16%. The European Central Bank (ECB) terminal rate expectations moved above 3%. Several ECB speakers said today that hikes should not be affected by political noise and that the policy rate should rise much higher.

EM Asia Inflation Pressures

Against this backdrop, today’s off-cycle central bank meeting in India raised concerns that there will be another emergency rate hike there. But it turned out that the central bank simply wanted (was asked?) to explain to the government why it missed the inflation target for three quarters in a row. A larger rate hike, however, seems imminent in the Philippines. The central bank signaled once again that it might raise its policy rate by 75bps on November 17 – moving in step with the Fed – due to inflation concerns (the October print is out this evening). Unlike the Philippines, central banks in Indonesia and Malaysia might have more policy room for the dovish pivot. The Bank Indonesia pointed out that the second round of inflationary effects was not as strong as initially feared. The central bank of Malaysia stated that it was not on a “pre-set course” after today’s expected 25bps rate hike.

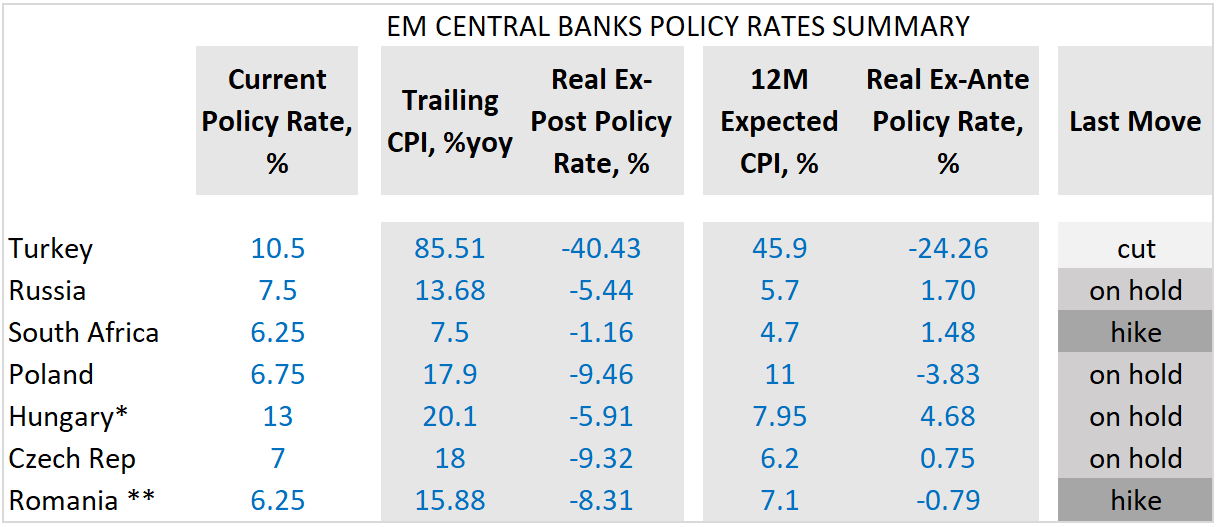

EM Peak Rates

The “data dependent” argument was also made by the governor of the Peruvian central bank, inviting suggestions that it might stay on hold already next week, joining Brazil and (maybe) Chile. While LATAM is contemplating exits from the tightening cycles, most of EMEA is already there (see chart below). The region now has only two active “hikers” – South Africa and Hungary (shadow hikes) – and today’s “on hold” decision by the Czech national bank confirmed the status quo. The next important milestone for the region is Poland’s rate-setting meeting. The central bank surprised the markets by keeping the policy rate unchanged in September. Still, inflation accelerated more than expected last month, and the market continues to price in more hikes on a 12-month horizon. Stay tuned!

Chart at a Glance: EMEA Doves Come in Droves

Source: VanEck Research; Bloomberg LP

* Hungary’s official policy rate is on hold, but there is massive shadow tightening

** Romania hiked, but indicated that this is likely to be the last hike

Related Insights

Related Insights

10 febrero 2026

06 marzo 2025

20 febrero 2025

10 febrero 2026

La erosión del valor de la moneda vuelve a estar en el centro de atención. A continuación, analizamos qué lo está impulsando, qué podría revertirlo y cómo estamos posicionando las carteras en ambos escenarios.

07 abril 2025

Los aranceles de Trump avivan los temores de una guerra comercial, impulsando la volatilidad del mercado, el riesgo inflacionario y la amenaza de una recesión. Ante posibles represalias globales, el crecimiento a corto plazo corre un riesgo evidente.

06 marzo 2025

Los aranceles de Trump, la próxima fase de la IA y una posible revalorización del oro estadounidense podrían sacudir los mercados; los inversores que se adelanten a estas transiciones estarán mejor posicionados.

20 febrero 2025

El avance de la IA en China, la persistente inflación, el rendimiento superior del oro y el aumento de la demanda energética ponen de relieve un panorama de inversión cambiante.

16 enero 2025

En 2025, superar los problemas significa equilibrar la innovación tecnológica, las coberturas contra la inflación, los cambios energéticos y los riesgos derivados de los recortes del gasto y la inflación.