China’s Dismal Q2 GDP – Nothing to See Here?

15 July 2022

Read Time 2 MIN

China Growth Slowdown

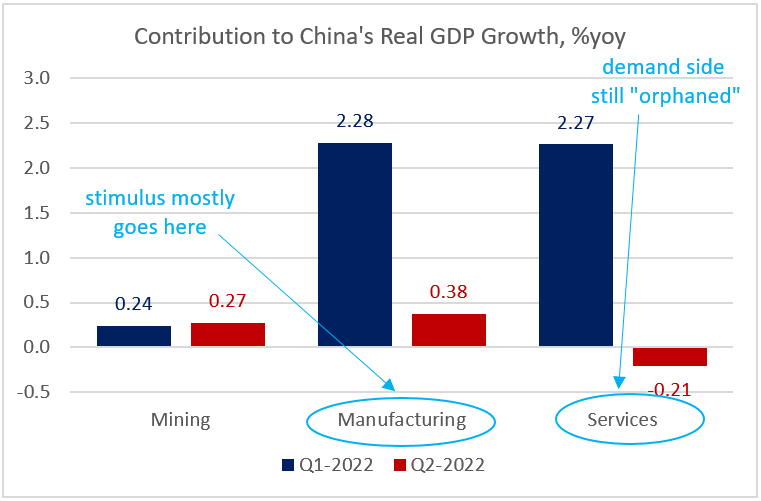

Chinese stocks reacted negatively to China’s dismal Q2 GDP print, even though June’s activity data showed signs of a rebound. The Q2 real GDP growth dropped by 2.6% in sequential terms and was barely positive on a year-on-year basis (0.4%). The services sector was hit the hardest – posting a negative year-on-year growth for the first time since the pandemic (Q3 2020). But manufacturing also showed a comparable drop in the contribution to quarterly growth (see chart below). China’s zero-COVID policy was the main culprit, and the removal of some restrictions was already visible in June’s industrial production, retail sales and investments. (Much) stronger than expected credit aggregates for June suggest that domestic activity should show even better results in July and August – naturally, provided there are no new lockdowns.

China Policy Stimulus

The question is whether the prospective Q3 rebound (fingers crossed) would significantly narrow (or close) the widening gap between the 2022 growth forecast and the official growth target. As we said, easier movement restrictions are a huge plus – but given that China’s zero-COVID policy will not go anywhere any time soon, there is an ever-present risk that lockdowns will be back. We also keep an eye on the new growth headwind, which some commentators call the “mortgage payment crisis”. And this brings us back to the additional stimulus. Today’s reports that the central bank decided to keep the 1-year medium-term lending facility rate unchanged at 2.85% tells us that this is pretty much business as usual as regards the fiscal-monetary breakdown (emphasis on fiscal support). Finally, authorities continue to target supply side (especially infrastructure) to prop up growth, while demand side remains an afterthought. The next stop on the growth front is the release of July’s activity gauges at the end of the month.

China Growth – Global Implications

China’s growth trials and tribulations can have a significant impact on some global commodity prices – with major implications for some emerging markets (EM) currencies, like the Chilean peso. Granted, concerns about the policy direction after the presidential elections helped to drive the peso down this year, but this happened against the backdrop of falling copper prices. The central bank tried to stay away from the FX market, but finally gave up yesterday, announcing a USD25B FX intervention program, making the Chilean peso the happiest EMFX on the block (up by 438bps against the U.S. dollar, according to Bloomberg LP, as of 9:40am ET). Every little bit helps, when dealing with persistent inflation pressures – including a stronger/stable currency. Stay tuned!

Chart at a Glance: China – Universal Slowdown, Lopsided Stimulus

Source: VanEck Research; Bloomberg LP

Related Insights

IMPORTANT DEFINITIONS & DISCLOSURES

This material may only be used outside of the United States.

This is not an offer to buy or sell, or a recommendation of any offer to buy or sell any of the securities mentioned herein. Fund holdings will vary. For a complete list of holdings in VanEck Mutual Funds and VanEck ETFs, please visit our website at www.vaneck.com.

The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results. Information provided by third-party sources are believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as of the date of this communication and are subject to change without notice. The information herein represents the opinion of the author(s), but not necessarily those of VanEck.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction, nor is it a commitment from Van Eck Associates Corporation or its subsidiaries to participate in any transactions in any companies mentioned herein. This content is published in the United States. Investors are subject to securities and tax regulations within their applicable jurisdictions that are not addressed herein.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.