Is “Everything Rally” In Trouble?

22 February 2023

Read Time 2 MIN

Fed Message and the Market

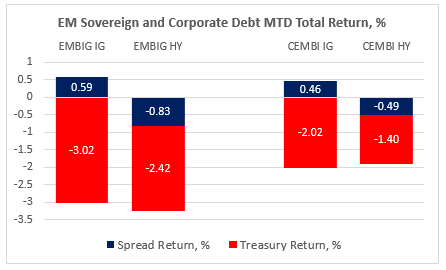

January’s rally in the 10-year U.S. Treasury yield is now completely undone, causing collateral damage in emerging markets (EM) debt. As you can see on the chart below, EM debt’s losses in February are largely the result of higher “risk-free” rates – this applies both to sovereign and corporate bonds. Lower-rated bonds were also affected by higher U.S. rates volatility, which has a fairly strong correlation with High Yield EM spreads (this shows as the negative spread return on the chart). The “higher for longer U.S. rates” narrative is partly driven by a slower pace of disinflation and more robust domestic activity in the U.S. And the market was slow to catch up with the U.S. Federal Reserve’s (Fed’s) hawkish message. The Fed’s minutes this afternoon might well provide an extra push in the hawkish direction.

Fed, Geopolitics, Macro

Can U.S. rates start “decompressing” once the new Fed narrative gets internalized by the market? Quite possibly. It is not unusual for UST yields to anticipate the Fed’s path (the peak rate and eventual easing in this case) well in advance. However, higher geopolitical tensions might complicate things. Will the next leg of Russia’s offensive in Ukraine affect Europe’s growth prospects (the consensus priced out the 2023 recession) and reaffirm the “least bad” status of the U.S. dollar and U.S. rates? Or will another debt ceiling debacle (ummm… debate) in the U.S. – together with the persistent drumbeat about the end of the petrodollar – make the greenback’s life more difficult this time around?

China’s Recovery

China is, of course, an integral part of the global geopolitical “knot”, but we suspect that the market might be paying more attention to the economic data flow in the next few days. China’s high frequency data signals that the recovery might be “uneven” and perhaps even “delayed” until H2/early-2024. There is a sense that perhaps the market’s pause is justified after the huge “reopening” rally, and it’s time to wait until the recovery’s timeline becomes clearer. The next set of China’s activity gauges (out next week) will therefore be closely watched. Stay tuned!

Chart at a Glance: EM Debt Returns Hit by Higher Risk-Free Rates

Source: Bloomberg LP.

CEMBI – J.P. Morgan Corporate Emerging Markets Bond Index is a global, liquid corporate emerging markets benchmark that tracks U.S.-denominated corporate bonds issued by emerging markets entities.

Related Insights

IMPORTANT DEFINITIONS & DISCLOSURES

This material may only be used outside of the United States.

This is not an offer to buy or sell, or a recommendation of any offer to buy or sell any of the securities mentioned herein. Fund holdings will vary. For a complete list of holdings in VanEck Mutual Funds and VanEck ETFs, please visit our website at www.vaneck.com.

The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results. Information provided by third-party sources are believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as of the date of this communication and are subject to change without notice. The information herein represents the opinion of the author(s), but not necessarily those of VanEck.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction, nor is it a commitment from Van Eck Associates Corporation or its subsidiaries to participate in any transactions in any companies mentioned herein. This content is published in the United States. Investors are subject to securities and tax regulations within their applicable jurisdictions that are not addressed herein.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.