Boeing and Constellation: Moat Stocks Rebound After Drawdown

03 June 2020

Read Time 3 MIN

Morningstar strategist Andrew Lane recently published a research paper examining the performance of the Morningstar® Wide Moat Focus IndexSM in periods following market drawdowns. I’ve often written of the long-term nature of Morningstar’s moat investing philosophy, and this piece hammers home the potential benefits of the strategy’s systematic focus on valuations. The strategy’s March 2020 index review coincided with one such period, and we’re tracking the dynamics of many of the companies selected for inclusion at that time, including Boeing (BA), Bank of America (BAC) and Constellation Brands Inc (CTZ).

Focus on Valuations Has Driven Outperformance versus Broad Market

Investing in companies with sustainable competitive advantages, or wide economic moats, is a popular investing strategy. So popular, particularly in times of uncertainty, that demand for these companies can drive share prices higher relative to those companies that lack a discernible economic moat. That is what makes valuation research so important. Identifying when these well-positioned companies’ share prices are trading below fair value and then allocating at attractive entry points can make the difference between outperformance and underperformance.

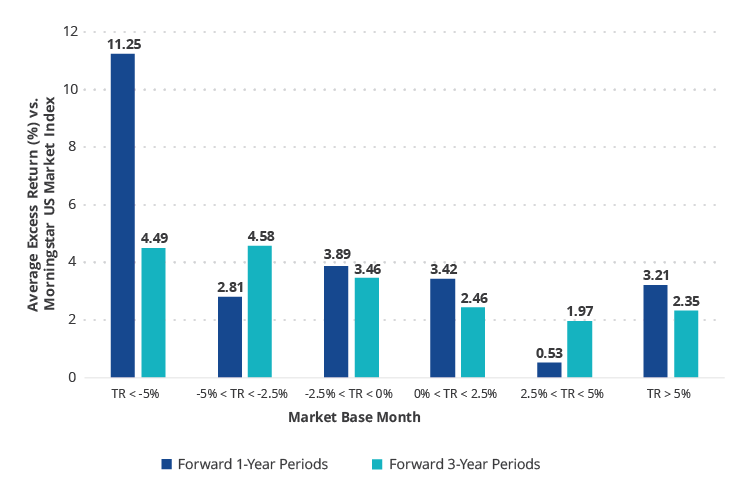

Investing in wide moat companies alone hasn’t always generated excess returns relative to the broad market as measured by the Morningstar US Market Index and has even underperformed the market in some instances. This is where valuations may make a difference. As evidenced by the paper, Wide Moat Focus Index: Strong Performance After Market Declines, Morningstar’s regular assessment of valuation dislocations has contributed to the Morningstar Wide Moat Focus Index’s impressive average excess returns relative to the broad market in periods following a month of any market return profile. Even more impressive is that average excess returns relative to the broad market in periods following months in which the market is down more than 5% were even more pronounced. While not every period in the study features outperformance, on average the index has a track record of success.

Sizeable Market Declines Have, on Average, Preceded Excess Returns

2/28/2007 - 3/31/2020

| Number of Occurrences | ||||||

| 1 Year Periods | 15 | 11 | 21 | 51 | 30 | 17 |

| 3 Year Periods | 13 | 9 | 21 | 37 | 26 | 15 |

Source: Morningstar. Data as of 3/31/2020. Morningstar Wide Moat Focus Index vs. Morningstar US Market Index. Performance data quoted represents past performance. Past performance is not a guarantee of future results. Index performance is not illustrative of fund performance. Prior to 4/24/2012, VanEck Vectors Morningstar Wide Moat ETF had no operating history. For fund performance current to the most recent month-end, visit vaneck.com.

Talk about Timing

Though we didn’t know it at the time, the Morningstar Wide Moat Focus Index rebalanced on the market’s recent bottom, March 20 - 23. Big name companies trading at big time discounts to Morningstar’s fair value estimate were added.

Boeing (BA) was added to the index for the first time when it was trading at a 70% discount to Morningstar’s fair value. At the end of April, Morningstar reduced Boeing’s fair value estimate approximately 15%, citing its debt burden associated with the continued 737 MAX grounding. Despite this reduction in fair value estimate, Boeing ended the month of May trading at nearly a 50% discount to fair value and has returned 53.51% since being added to the index.

Constellation Brands (STZ) has also posted an impressive 44.94% return in the short time it has been in the index. The beverage company—which derives its moat from its intangible assets, one of Morningstar’s five sources of moat—finished May at a 20% discount to fair value.

Other new entrants have lagged the broad market in that period, such as American Express (AXP, 29.98%), Bank of America (BAC, 22.62%), Corteva (CTVA, 21.89%), Blackbaud (BLKB, 13.63%), and US Bancorp (USB, 10.46%). As mentioned earlier, this strategy is built for the long-term and time will tell how the March 2020 rebalance will impact index performance.

VanEck Vectors Morningstar Wide ETF (MOAT) seeks to replicate as closely as possible, before fees and expenses the price and yield performance of the Morningstar Wide Moat Focus Index.

Related Insights

Related Insights

09 July 2026

As mega-cap tech pulled back in June, the Moat Index gained on semiconductor and cybersecurity strength and the SMID Moat Index rose on AI chips and a notable health care deal.

09 June 2026

Software and cybersecurity earnings showed that AI is broadening demand for enterprise tech, not eroding it, as Moat Indexes rebounded late in the month.

08 May 2026

Tech and semiconductor stocks led April’s rebound. Moat stocks participated in the rally though narrow leadership favoring mega-cap growth weighed on relative performance.

10 April 2026

U.S. equities fell in March as oil surged on geopolitical tensions. The Moat Index lagged on no energy exposure, while the SMID Moat Index held up with help from energy and materials.

30 March 2026

The Moat Index added NVIDIA, Broadcom and new names following its quarterly review, as tech dislocations created opportunity, while maintaining a value tilt and notable discount to fair value.