EM Hikes - Outlasting the Fed?

27 June 2022

Read Time 2 MIN

Fed Rate Hikes Expectations, Recession Concerns

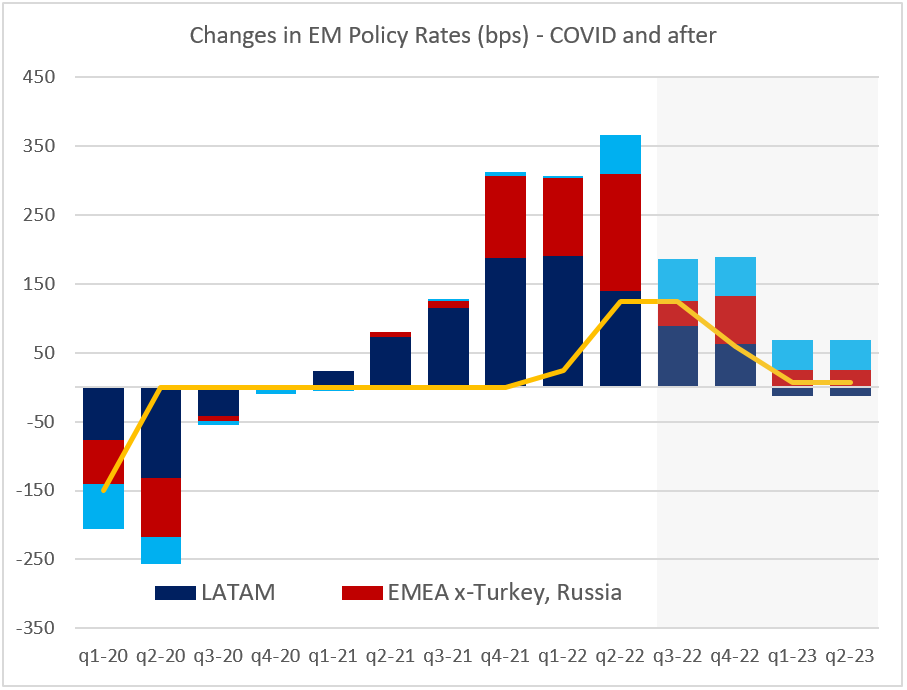

The current hiking cycle in the U.S. is expected to be short-lived – in part due to persistent recession concerns (the nearly-zero Federal Reserve Bank of Atlanta’s GDP nowcast and below-consensus activity surveys for June did little to improve sentiment last week). Where does this leave emerging markets (EM) central banks, many of which started to tighten aggressively well before the U.S Federal Reserve (Fed)? The current market expectations (“embedded” in local swap curves) suggest that the tightening cycle in EM might have peaked in Q2, but it can, nevertheless, outlast the Fed (see chart below). There are several reasons for that.

Uphill Inflation Battle in EM

EMs are facing multiple growth headwinds this year (stimulus withdrawal, capital outflows and higher commodity prices). However, many economies are growing above potential, and it is still an uphill battle on the inflation front for most countries – especially in Central Europe, where annual inflation is now in double digits (the consensus sees Poland’s inflation accelerating to 15.5% year-on-year in June). Aggressive frontloading leaves room for a slower pace of hikes going forward (Brazil is a good example), but it is too early to switch to neutral policy stance – an attempt to do so is likely to be treated by the market as a mistake (keep an eye on the Czech National Bank after the dovish makeover of its board). There is also a “changing of the guard” aspect in EM – Asian central banks were latecomers to the policy normalization game, but are now in the liftoff stage (India, Malaysia, the Philippines) or getting close to it (Thailand, Indonesia).

Turkey’s Unorthodox FX Policy

No discussion about EM rates will be complete without mentioning the block’s “enfant terrible” – Turkey. Turkey is flatly refusing to hike (despite 70%+ annual inflation), expanding the network of “out-of-the-box” FX rules instead. The latest “innovation” limits access to the lira-denominated loans for companies with FX deposits above a certain threshold. The lira did strengthen against the U.S. dollar after Friday’s announcement, but not nearly as much as after the first “out-of-the box” solution in December 2021 (Law of Diminishing Returns?) – suggesting that measures like this are poor substitutes for orthodox policies. Stay tuned!Chart at a Glance: EMs to Continue Hiking in 2022/23

Source: VanEck Research; Bloomberg LP

Related Insights

IMPORTANT DEFINITIONS & DISCLOSURES

This material may only be used outside of the United States.

This is not an offer to buy or sell, or a recommendation of any offer to buy or sell any of the securities mentioned herein. Fund holdings will vary. For a complete list of holdings in VanEck Mutual Funds and VanEck ETFs, please visit our website at www.vaneck.com.

The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results. Information provided by third-party sources are believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Any opinions, projections, forecasts, and forward-looking statements presented herein are valid as of the date of this communication and are subject to change without notice. The information herein represents the opinion of the author(s), but not necessarily those of VanEck.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction, nor is it a commitment from Van Eck Associates Corporation or its subsidiaries to participate in any transactions in any companies mentioned herein. This content is published in the United States. Investors are subject to securities and tax regulations within their applicable jurisdictions that are not addressed herein.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.