Welcome to VanEck

Select Investor Type

01 September 2020

The level of stimulus the Federal Reserve (Fed) has thrown at the economy this year is almost unprecedented and has investment consequences.

First, gold. Our outlook for gold has been bullish since the summer of 2019, and the case for gold investing has become more solid in recent weeks as gold rallied through its $1,800 per ounce technical resistance level and past its previous high of $1,921.

To help gauge how high gold could go, we looked at prior gold bull markets—which could be categorized as either inflationary or deflationary—as well as the persistence of negative real interest rates. Our base case now is that we are in a deflationary environment and, based on historical trends, gold’s price typically moves up two to three times in a deflationary cycle. This helped inform the $3,400 price target we have set for gold. (See prior gold bull markets here.)

Financial markets have also benefited from the Fed stimulus. And perhaps the surprise from this summer’s data is that the global economy is doing quite well, supporting the markets, despite the social distancing that we all feel in our personal lives. Important commodities like copper have regained pre-COVID highs. In addition, China’s industrial recovery is pointing to all-time highs in activity, even while the consumer activity is still below prior-year levels.

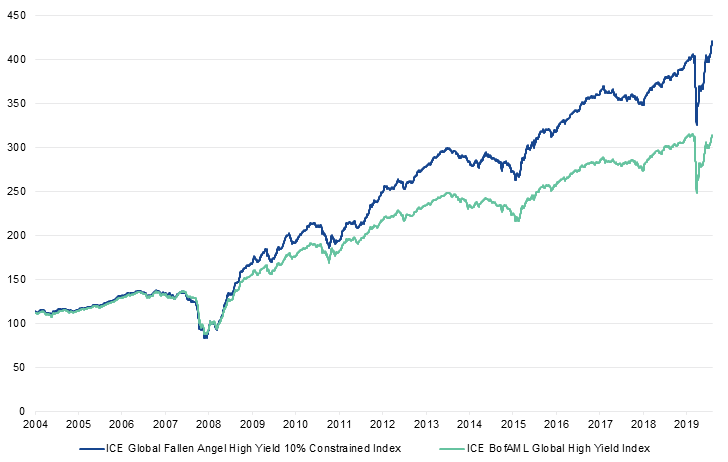

In a recessionary environment, some bonds are going to default or be downgraded. Fixed income markets this year generally started recovering after the Fed announced plans to intervene. We have already seen a record amount of new fallen angel bond volume over $140B as of 31 July 20201—and expect more through the remainder of the year.

Similar to 2016, we have seen a lot of energy companies downgraded to become fallen angels, and the fallen angel strategy is buying those downgraded bonds. These new energy fallen angels are among the top contributors to performance of the fallen angel strategy so far this year. As long as the Fed remains supportive, we believe this strategy should continue to do well.

Source: ICE Data Indices as of 31/7/2020. This chart is for illustrative purposes only. Broad High Yield Bond Market is represented by the ICE BofAML Global High Yield Index. Fallen Angel Global High Yield is represented by the ICE Global Fallen Angel High Yield 10% Constrained Index (HWCF). Index performance is not illustrative of fund performance. Indexes are unmanaged and are not securities in which an investment can be made. Current data may differ from data quoted. Past performance is no guarantee of future results. An investor cannot invest directly in an index. The results assume that no cash was added to or assets withdrawn from the index.

One risk to gold and bonds is if there were to be an unforeseen rise in interest rates in the U.S. This could come from a burst of inflation driven by supply chain issues or money supply growth, for example. This is not our “base case”, but it is possible. As we can see from the chart below, higher real interest rates are not good for gold.

Source: VanEck, FactSet, Bloomberg. Data as of May 2020. Past performance is no guarantee of future results.

Another concern for the market is that the return to full employment may be bumpy. An incredible number of people have been laid off in the U.S. and, regardless of GDP numbers, people are unlikely to return to work at the same levels as the start of the year. Concern may be high enough for policy makers to take additional steps that may impact the financial recovery.

In our view, it is hard to invest according to politics, but it is important to look at the underlying policies and see if they are going to change. Regardless of who is elected in November, we don’t anticipate a big shift in Fed policy. As far as tax policy, we think there would have to be quite a degree of confidence in the economic recovery before any possible fiscal shock in terms of a big tax increase. In our view, investors should ignore all the political noise and make sure there is going to be a policy change before shifting their assets.

1Source: FactSet, ICE Data Indices, LLC and Morningstar.

This is a marketing communication. Please refer to the prospectus of the UCITS and to the KID before making any final investment decisions.

This information originates from VanEck (Europe) GmbH, which has been appointed as distributor of VanEck products in Europe by the Management Company VanEck Asset Management B.V., incorporated under Dutch law and registered with the Dutch Authority for the Financial Markets (AFM). VanEck (Europe) GmbH with registered address at Kreuznacher Str. 30, 60486 Frankfurt, Germany, is a financial services provider regulated by the Federal Financial Supervisory Authority in Germany (BaFin).

The information is intended only to provide general and preliminary information to investors and shall not be construed as investment, legal or tax advice VanEck (Europe) GmbH, VanEck Switzerland AG, VanEck Securities UK Limited and their associated and affiliated companies (together “VanEck”) assume no liability with regards to any investment, divestment or retention decision taken by the investor on the basis of this information. The views and opinions expressed are those of the author(s) but not necessarily those of VanEck. Opinions are current as of the publication date and are subject to change with market conditions. Certain statements contained herein may constitute projections, forecasts and other forward-looking statements, which do not reflect actual results. Information provided by third party sources is believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Brokerage or transaction fees may apply.

All performance information is based on historical data and does not predict future returns. Investing is subject to risk, including the possible loss of principal.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of VanEck.

© VanEck (Europe) GmbH / VanEck Asset Management B.V.

21 July 2025

21 July 2025