Welcome to VanEck

Select Investor Type

14 August 2023

Crypto evolution, from Bitcoin to crypto-linked debit cards, struggles with adoption due to technological complexities and infrastructures - Gnosis Pay (GNO) aims to solve key issues.

Please note that VanEck may have a position(s) in the digital asset(s) described below.

“The defense against the substitution of sovereign currencies is the maintenance of robust, trusted, and credible domestic institutions.” – IMF Blog, July 2023

After 6 months of dramatic BTC & ETH outperformance, many so-called “altcoins” rallied in July, especially those that had been designated securities in recent SEC lawsuits like SOL (+24%), MATIC (+5%), and ADA (+9%), following Ripple’s victory vs. the SEC on the matter of whether XRP the token (+51%) is a security when traded on centralized crypto exchanges.

For the month, Bitcoin & Ethereum fell (both down 3%), while nearly every other crypto sector we track posted gains, except for the long-suffering Metaverse coins.

In our view, one major challenge for digital asset investors is balancing the winner-take-all characteristics historically evident among digital platforms with the extreme price performance disparity already evident year-to-date. Historically, Bitcoin dominance rises in the early part of a bull market and then fades as investors borrow against those gains to speculate on riskier assets. This time, however, leverage is less available, and the regulatory environment in the US is much more severe. Meanwhile, the Bitcoin halving is still ahead of us, as we explained in a .

|

|

July |

YTD |

|

Coinbase |

32% |

168% |

|

MarketVectorTM Infrastructure Application Leaders Index |

9% |

37% |

|

MarketVectorTM Smart Contract Leaders Index |

4% |

32% |

|

Nasdaq 100 Index |

4% |

37% |

|

MarketVectorTM Decentralized Finance Leaders Index |

3% |

32% |

|

S&P 500 Index |

3% |

19% |

|

MarketVectorTM Centralized Exchanges Index |

1% |

1% |

|

MarketVectorTM Media & Entertainment Leaders Index |

-3% |

-14% |

|

Ethereum |

-3% |

55% |

|

Bitcoin |

-3% |

77% |

Source: Bloomberg, VanEck research as of 7/31/2023. Past performance is not indicative of future results. Not a recommendation to buy or sell any of the names mentioned herein.

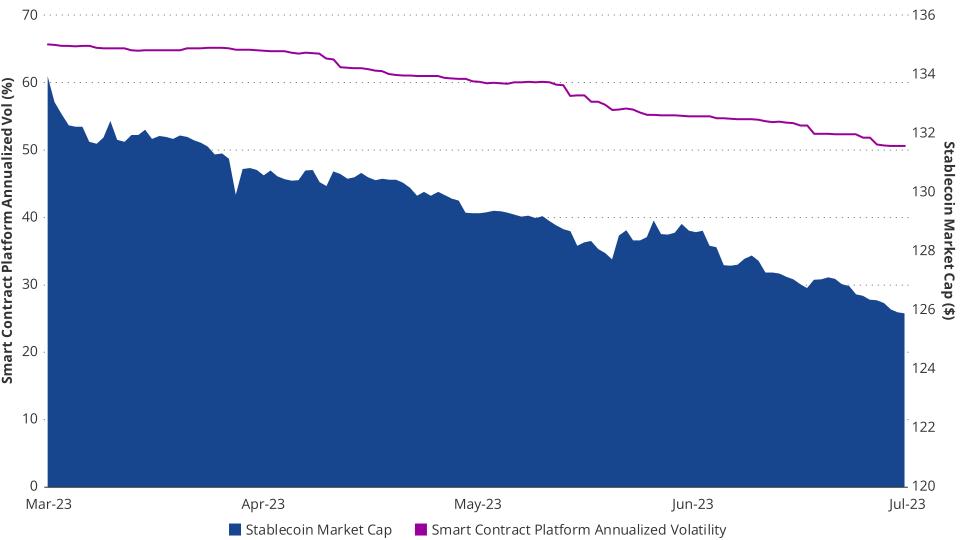

Layer 1 smart contract platforms (SCPs) rose 4% in July, while the sector (MVSCLE) 30-day annualized volatility fell to 34%, the lowest of the 4 major categories we track. Falling volatility has been a trend for much of the past year despite extreme events, including the collapse of FTX, Luna, and 3AC. At the same time, the market cap of stablecoins has moved in lockstep with the falling volatility. This makes sense to us because as opportunities for trading decline due to decreased vol, stablecoin yields should also fall, reducing demand for stablecoins. We think a new leverage cycle is a precondition for the type of absolute returns and volatility that have characterized past cycles. But so far, there is little evidence of rising demand or supply for leverage. Anyway, among the SCPs we track, the best performers of the month were Solana (SOL), up 24%, and Optimism (OP), +23%. This month's laggards included Stacks (STX), down 14%, Fantom (FTM), down 23%, and Ethereum -4%.

Source: Artemis.xyz, as of 7/26/2023. Past performance is no guarantee of future results. Not intended as a recommendation to buy or sell any securities named herein. Index performance is not representative of fund performance. It is not possible to invest directly in an index.

In July, Solana yet again proved its resilience by rebounding from major ecosystem FUD. In early June, the SEC labeled Solana a security in its lawsuit vs. Coinbase, and this catalyzed a 25% decline in the price of SOL. Since then, Solana has seen its fundamental metrics improve as ecosystem participants grew amid the rebirth of Solana DeFI. Though daily active users on Solana only saw a slight increase, around 3.5%, Solana applications like MarginFi, Hxro, and Drift catalyzed on-chain activity and caused a 31% bump in DEX volume and a 12.5% increase in TVL. As a result of the increase in usership on Solana, fees increased by 30% compared to the month of June. One interesting announcement in the Solana ecosystem was the concurrent announcements from both Neon, a Solana infrastructure project, and the Solana Foundation. Both entities launched compilers that would enable Solana to run Solidity smart contracts. As a result, Solana now has two credible offerings that will make it simpler for Ethereum developers to move over to Solana without making major changes to their coding language. Such offerings may bolster Solana’s ability to vie for the pie of blockchain developers. Another positive development for the Solana ecosystem was the listing of Helium (HNT) tokens on Coinbase after a successful move to the Solana blockchain. Helium is a decentralized cellphone and wireless communication network which originally ran a purpose-built layer 1 blockchain but migrated to Solana to save development costs and boost performance. Also helping Solana this month was the verdict in the Ripple case, which stipulated that tokens like SOL could be considered both securities and commodities – thus removing the probability that the SOL token would be proven through litigation to be a security under all circumstances.

Source: Artemis as of 7/31/2023. Past performance is no guarantee of future results. Not intended as a recommendation to buy or sell any securities named herein.

Despite increasing competition in the Layer-2 sub-sector of smart contract platform market, with Starknet announcing a major software improvement to enable more throughput, Mantle launching their mainnet Layer-2, and Polygon asserting a compelling multi-chain vision alongside a token revamp, Optimism’s OP token was a top performer in July. Regarding fundamental metrics, daily active addresses were up 23%, fees were up 29%, and daily transactions on Optimism surpassed Abitrum’s for the last few days of the month. Important catalysts came from increased interest in decentralized perpetual futures platforms like Kwenta and the launch of Sam Altman’s (OpenAi founder) Worldcoin, which runs on Optimism. (Colleague Pranav Kanade wrote about the Worldcoin project .)

For background, Worldcoin is a decentralized identity protocol with 2.1M accounts created. With each user onboarded, WorldCoin must create a wallet to hold that user’s identification credentials. Over the last week, WorldCoin employed Gnosis’ Safe product (see more on Gnosis below) to create a new wallet for each newly onboarded user. A significant percentage of these will likely begin using crypto assets on Optimism. The result is that Worldcoin may become a robust onboarding mechanism for cryptocurrency in general and the Optimism network in particular.

Optimism in July asserted its vision for its Optimism Superchain internet of blockchains governance structure and community norms while hinting at potential value accrual pathways. In a post that Optimism titled , the Optimism Collective (a band of companies, communities, and citizens working on the protocol) hinted that social norms should drive all blockchains and that those built using Optimism code should opt into Optimism’s future sequencer set which will be staked with OP tokens. While this declaration is non-binding, it sets the table for increasing community and builder cohesion around driving value back to the OP token to pay the OP team developing Optimism’s open-source software.

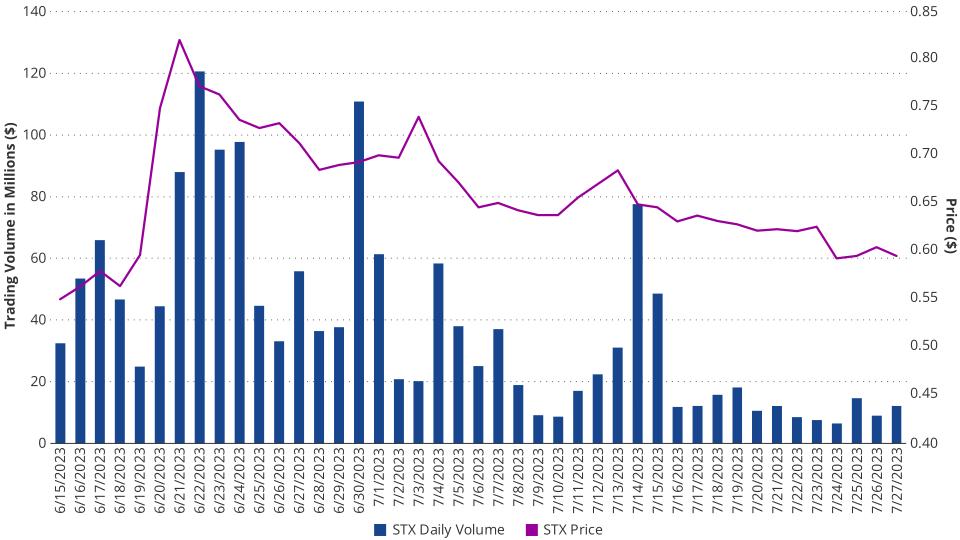

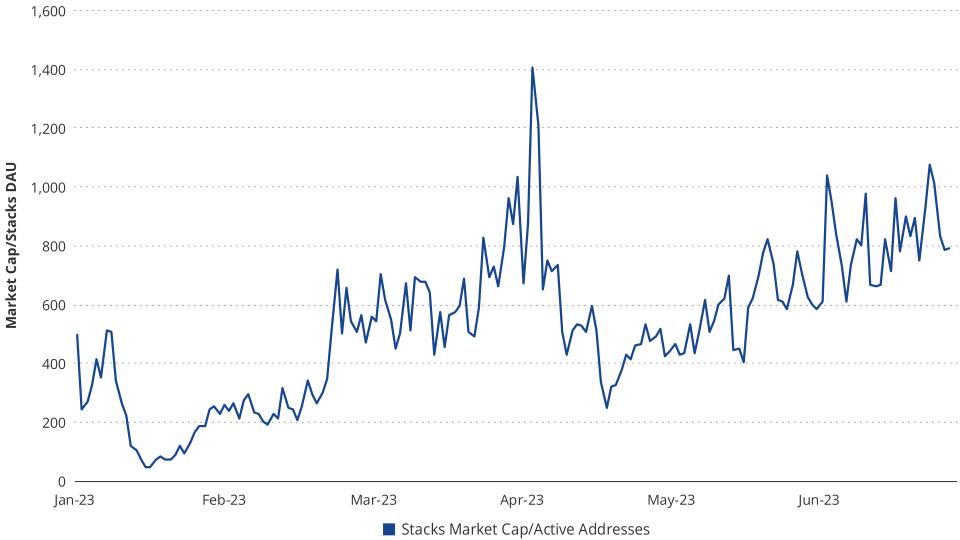

Stacks (STX) fell 14% in July, underperforming most L1s and L2s. The most telling metric of Stacks’ decline is the significant drop in the token’s daily trading volumes. During the month of June, the STX token averaged $55 million in daily trading volumes, with a monthly high of $120 million traded on June 22nd, coinciding with a local maximum for the token price at $0.82. Conversely, this past month, the average daily trading volume plunged to around $23 million. On the surface level, it appears the underperformance this month is a simple mean reversion back to similar price levels before the few isolated days in June, with the token sitting just under $0.60. In the months of June and May, Stacks had emerged as among the most credible of the Bitcoin L2s, on which Ordinals might be traded. As the narrative dried up, trading volumes and general interest in Stacks also evaporated.

Diving deeper into Stacks’ on-chain data, we notice the number of daily active addresses has continuously declined since the start of the year. In fact, daily active addresses hovered around 1,000 since the beginning of July, which marks the longest consecutive period this year in that range. Whether we are measuring market cap-to-TVL or price-to-active addresses. STX appears to be discounting a high probability of exponential growth in users and deposits. Stacks’ market cap to active address ratio is among the highest since late spring, ahead of the protocol’s “Nakamoto” consensus upgrade scheduled for November, which may increase the usability of the chain.

Source: Coingecko as of 7/27/2023. Past performance is no guarantee of future results. Not intended as a recommendation to buy or sell any securities named herein.

Source: Artemis as of 7/26/2023. Past performance is no guarantee of future results. Not intended as a recommendation to buy or sell any securities named herein.

Source: Artemis as of 7/26/2023. Past performance is no guarantee of future results. Not intended as a recommendation to buy or sell any securities named herein.

Fantom (FTM) suffered immensely this month with the hacking of the Multichain bridge, Fantom’s most important bridge to Ethereum, taking centerstage. TVL of Fantom dropped from $200 million to $67 million following the exploit, during which $126 million was drained from its Ethereum liquidity pools, rendering the wrapped representation of these assets on Fantom worthless. This is because Multichain holds assets on one end of the bridge and mints a backed representation of each asset on the other end. When Multichain was attacked, the hacker took the locked assets on the Ethereum side, which caused the minted representations on Fantom to become worthless. Since Fantom has no native stablecoins, all the value in popular stablecoins on its chain, including USDC, USDT, and TUSD, were bridged representations, with Multichain dominating 80% of this market.

While the actual Fantom token itself was not exposed to the Multichain hack, the hack represents a loss of trust in the chain. As a result of the hack, Fantom saw its most popular lending protocol, Geist, halted and then abandoned as the value of its tokens became zero. While transactions, users, and fees increased for the month, this can be attributed to uncertainty-induced volatility and the rush to exit the Fantom ecosystem.

Source: Artemis as of 7/26/2023. Past performance is no guarantee of future results. Not intended as a recommendation to buy or sell any securities named herein.

The founding vision of cryptocurrency was to create a medium of exchange whose value was unalterable by central authorities who could depreciate the currency, censor what it could be used for, and restrict who could use it. While the first successful cryptocurrency, Bitcoin, fulfills much of the original vision, it fails to be practical for most people. This is because the Bitcoin network lacks the responsiveness, scalability, and simplicity necessary for mass consumer audiences. Also, its volatile value and lack of deep liquidity made it costly to hold and difficult to exchange.

To solve these problems, the next solution was stablecoins which are tokens whose value was pegged to a fiat currency by an algorithm or by being backed by off-chain assets. Stablecoins solve the issue of the risks of holding BTC and the challenges of hedging price exposure. Furthermore, more advanced blockchain designs solved time constraints that enabled payments to be settled in seconds rather than minutes. However, adopting cryptocurrencies for payments has remained elusive because most people simply do not want to deal with the blockchain. Users and merchants did not want to go through the added hassle of learning how to use wallets or the time commitment of exchanging crypto and fiat. Instead, merchants and consumers remained wedded to existing digital payments infrastructure using things like point-of-sale card station devices and credit cards.

The next attempt to solve the payments problem was to tie cryptocurrencies to debit cards. Thus emerged centralized exchanges like Binance, Coinbase, and Crypto.com, each offering debit cards that were linked to user exchange accounts. While users could deposit stablecoins, other digital assets, and fiat into their exchange accounts to be used by these debit cards, users were still shackled to centralized service providers who held custody over the users’ digital assets. At the same time, there was no direct link to a user’s on-chain account.

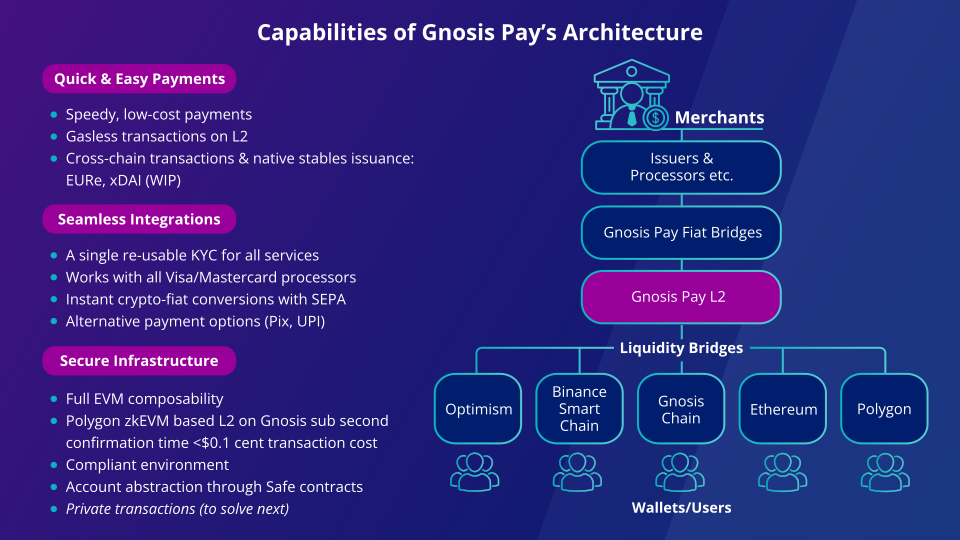

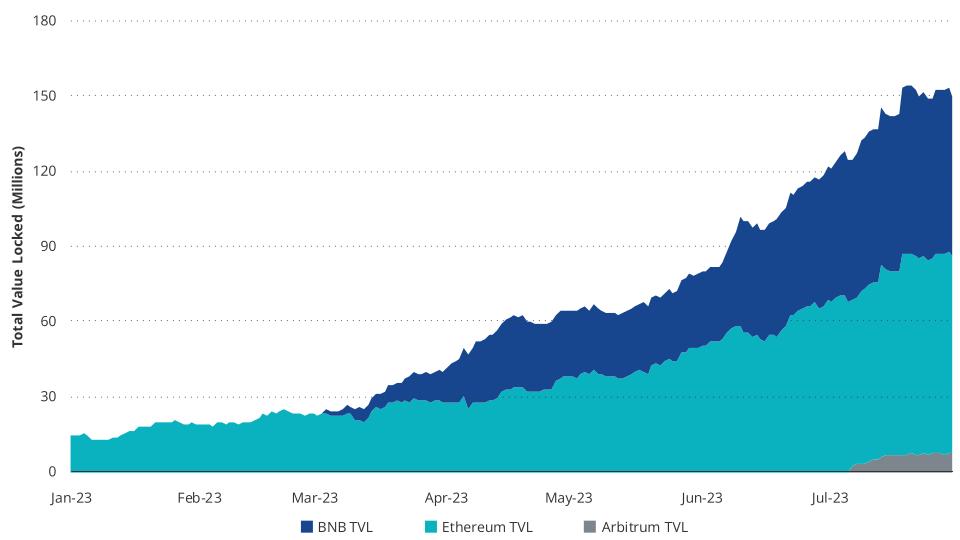

Now, Gnosis Pay (GNO) has established an innovative product to solve some of these issues. Gnosis Pay is a decentralized payment network that allows someone to pay at any merchant who accepts Visa with the cryptocurrency in their on-chain account. Gnosis Pay can accomplish this feat through its partnership with Monerium and their “EURe: which is a 1:1 Euro-backed stablecoin. On the backend, Monerium creates IBANs (international bank account numbers) for each card which links to each Gnosis Pay user’s on-chain account. Because Monerium is connected to the Euro area’s SEPA (Single Euro Payments Area) payment system, it can accept EURe tokens from Gnosis Pay users’ blockchain accounts, convert them into fiat and transmit them across SEPA to merchants at the point of sale. As a result, any user with EURe stablecoins in their on-chain wallet can use the Gnosis Pay debit card to pay at any merchant that accepts Visa. On the flip side, because each Gnosis Pay account has an associated IBAN, payments remitted in Euros are converted by Monerium into EURe stablecoins and sent to each account holder's blockchain wallet. All a user has to do is to have a balance of EURe stablecoins in their blockchain account linked to their Gnosis Pay debit card.

Source: Defillama.com as of 7/28.2023. Past performance is no guarantee of future results. Not intended as a recommendation to buy or sell any securities named herein.

To use Gnosis Pay, each user will have to have an account on Gnosis Pay’s Layer-2 blockchain of the Gnosis network. In practice, Gnosis Pay users must port token value from other blockchains, such as Ethereum, BSC, Gnosis, and Polygon, using the to Gnosis Pay before the Gnosis debit card can use it. Or, they can send fiat payments to their Gnosis Pay IBAN, which will be converted into EURe stablecoins and deposited into their accounts.

When a user sends funds to the Gnosis Pay Layer-2, they are screened for AML behavior and given KYC/KYB check by an identity verification company called . Once authorized and an account is created, a user authorizes the card to automatically draw from her or her blockchain account by linking it with the Gnosis Pay Application. The gas required for the transactions on the blockchain is taken care of by Gnosis Pay. In the future, MakerDAO’s Spark Protocol could enable users to borrow EURe stablecoins against their wallet’s non-stablecoin assets to make off-chain payments. Over time, Gnosis Pay will be available to other geographic regions like North America and Asia. Additionally, other stablecoins will be integrated into Gnosis Pay beginning in 4Q2023. Currently, the sign-up cost is €30, and another €10 for minting the card. There is a physical card, and eventually, a mobile card will be offered.

Source: Gnosis ETHCC Presentation.

We believe Gnosis Pay has made a substantial step forward that unlocks payments for everyday crypto users and Decentralized Autonomous Organizations (DAOs). DAOs, which are blockchain-based entities that often govern the business operations of on-chain applications, can now seamlessly pay for off-chain services in fiat, including vendor fees, employee wages, advertising, etc. Gnosis Pay has a high potential for adoption because many DAOs use Gnosis’s Safe multi-signature wallet to secure their on-chain treasuries. Collectively, Gnosis SAFE products secure more than in value on blockchains for DAOs, and converting a significant fraction of those entities to Gnosis Pay appears probable.

At this stage, the biggest impediments to mass adoption are Gnosis’s Pay’s limited geographic scope, the necessity of using the Gnosis Pay L2, the low float of EURe, and the lack of support for USD-based stablecoins like USDT and USDC. From the standpoint of usability, the ability to tap into the US financial system will be the biggest ongoing hurdle for Gnosis Pay growing widespread usage. From a regulatory perspective, it will be difficult for them to get partners, but it is almost certainly a top priority for the project’s team.

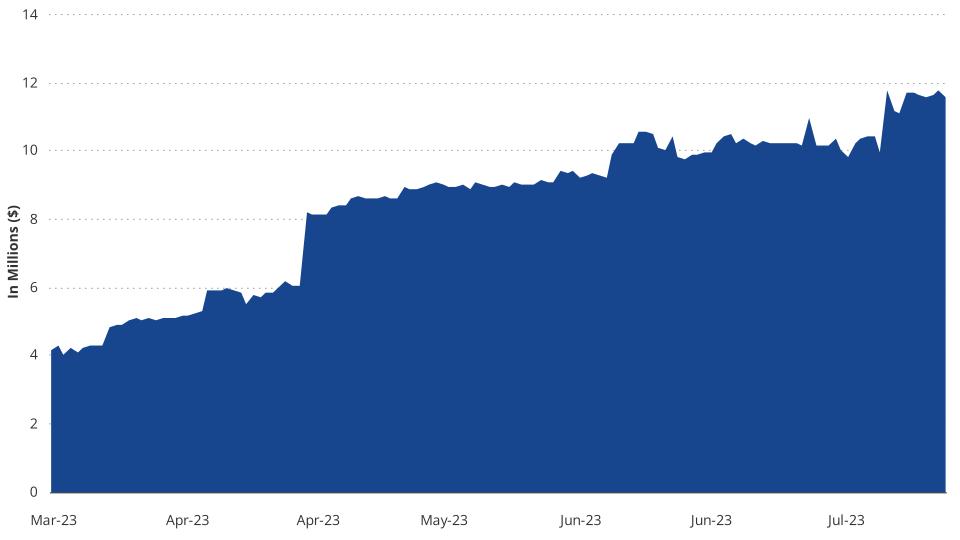

Another impediment to the greater success of Gnosis Pay is that it requires funds to be on the Gnosis Pay L2. The experience of bridging to Gnosis Pay is risky and time-consuming, and it exposes users to the risks of Gnosis Pay’s L2. Furthermore, because the supply of EURe is small at only $12M, there is not enough liquidity to feed a rapidly growing user base. This relatively small asset base makes it challenging for users to swap other assets for EURe without significantly moving the EURe price away from its peg.

Gnosis Pay is not alone in its non-custodial crypto debit cards, as the competitive marketplace is growing quickly. Some top constituents include Holyheld, BasedApp, , and Suberra. While each of these competitors has shown potential, each is currently limited to its geographical areas due to banking system challenges and regulatory constraints. Holyheld is limited to EU residents, BasedApp is relegated to Singaporeans, and Stables is accessible only to Australians. On the other hand, Suberra, which has yet to launch its card, will be available to users in the US. The biggest drawback of the competing offerings is user experience. In the case of BasedApp, Stables, and Holyhold, users must manually convert stablecoins to fiat currencies to “top-up” their fiat bank accounts to have funds to spend on the card. Gnosis Pay, by contrast, automatically pulls EURe balances when using a debit card. Additionally, the debit card holder must manually convert the fiat from their bank account into crypto to have the value back on the blockchain.

Currently, the fee structure for Gnosis Pay is unknown, as is Suberra’s, but the other competitive products have public fee structures that vary widely. BasedApp charges no fees on transfers but a card create fee and foreign transaction fees. It seems their monetization model relies upon the interest generated by holding the SGD that backs SGD stablecoins. Holyheld, on the other hand, has a deep menu of different types of charges for its product. It tells users to create new cards and charges them for crypto to fiat conversions at 0.75% for topping up the card or exchanging fiat for crypto. Additionally, Holyheld charges for a litany of other account actions, including outgoing fiat payments, fair usage charges, and account pin number change fees. By contrast, Stables does not charge for transfers or card usage but instead charges users a 1.5% fee when they swap between fiat and crypto to “top up” or withdraw from their fiat account.

Going forward, Gnosis has many different pathways it can choose to take that could lead to mass adoption. The chief obstacle it faces today is the strong user experience of the credit card ecosystem. While users love the simplicity of paying for things using credit cards and the rewards generated, merchants dislike the process of obfuscating credit card fees in higher consumer prices and/or paying for credit card charges themselves. Point of Sale devices like Stripe create even more costly overhead for consumer businesses. For example, Strip takes 2.7% on each transaction and a $0.05 fee. Gnosis Pay’s success could be found by unrooting this merchant-imposed, odious high fee structure that credit cards impose on the exchange of goods and services.

Gnosis could cut into this financial services racket by pushing merchants to charge lower fees for users of its cards through discounts to consumers (whether by lower prices for debit card purchases or higher prices for credit card purchases). This is not only because Gnosis would circumvent the credit card fees but also because Gnosis could send merchants rewards for charge activities using Gnosis Pay. This program could be paid for by Gnosis making an agreement with Monerium to remit some of the interest received from the Euros that back the EURe stablecoins to the merchants. While this would decrease Monerium's margin on the EURe business, it could be a catalyst that massively expands the market potential for EURe due to ardent merchant zest for Gnosis’s economical solution. However, this pathway would be the first step towards getting both the merchant and consumer off existing expensive, card-based point-of-sale infrastructure. In the long term, Gnosis will likely push both the consumer and the merchant to accept blockchain payments using wallet-based services, most likely embedded in cell phones. Regardless of the outcome, this initial entry point by Gnosis Pay is genuinely exciting and, if it lives up to its promise, could ultimately spur legislation in the United States on stablecoins. Additionally, the Gnosis architecture could help a “super-app,” such as X.com (formerly Twitter), launch a self-custody-based digital asset payment platform. In July, Twitter received its first three state money service business (MSB) licenses.

The MarketVector Decentralized Finance Leaders Index (MVDFLE) ended July +3%, outperforming Ether’s 3% price decline. The performance was mainly supported by Uniswap (UNI), which rallied 20% this month and represented ~33% of the index. DYDX and AAVE both notched gains this month, rising 6% and 1%, respectively, while LDO and CRV held the index back, falling 11% and 21%, respectively. MakerDAO stood out this month as its token, MKR, rallied an impressive 48% after the founder purchased more MKR, and the DAO’s estimated annual profit rose from real-world asset acquisition. Defi TVL dropped from $45.2b to $40.9b in July, driven by the falling price of Ether and the Curve exploit, resulting in many users withdrawing their assets from the protocol. Additionally, overall lending protocol TVL has now surpassed that of decentralized exchanges. This can be attributed to the growing adoption of Ether LSD products and the ease with which users can create negative-interest loans. Such creation is facilitated by the yield-bearing properties of LSD tokens, making them an attractive option for users seeking efficient debt management solutions.

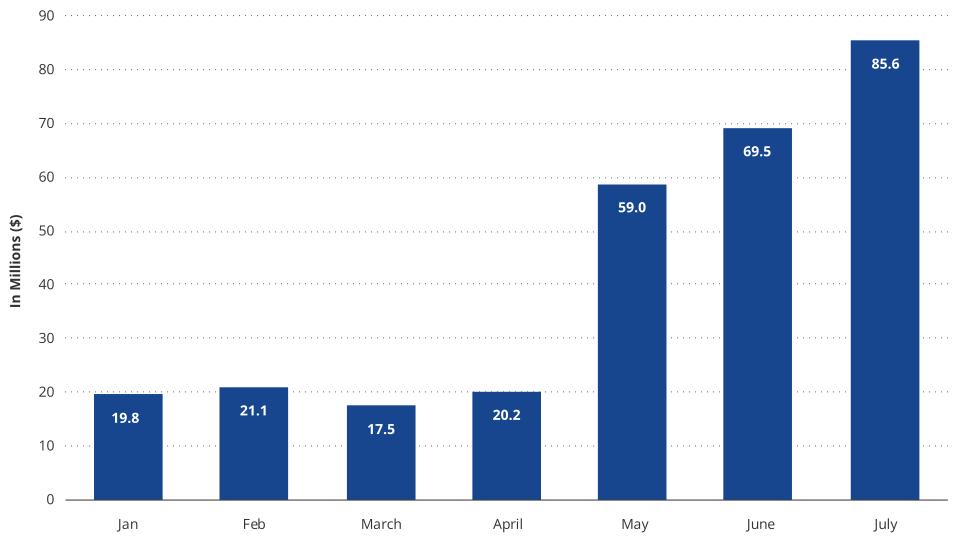

Over the last three months, MakerDAO has undertaken a significant transition in its asset composition. The platform has gradually reduced its reliance on USDC as the main asset backing DAI, decreasing it from 50% to approximately 9%. Instead, MakerDAO has adopted yield-bearing real-world assets (RWA), which now constitute over 50% of its assets, amounting to approximately $2.4 billion, according to data from a Dune dashboard by @SebVentures. This strategic shift has resulted in a remarkable surge in MakerDAO's estimated annual profit. Since the beginning of May, the estimated profit has nearly quadrupled, rising from $23 million to an impressive $86 million, as reported on makerburn.com.

Source: VanEck Research, makerburn.com as of 7/31/23.

Furthermore, MakerDAO successfully passed the Enhanced DAI Savings Rate proposal. This new development allows DAI holders to earn up to 8% interest by depositing their DAI into the DAI Savings Rate (DSR). The elevated rate will remain in effect until 20% of DAI is deposited into the DSR, providing a very attractive earning opportunity for DeFi users. Currently, just over $300 million of DAI has been deposited into the DSR, about 6.5% of the circulating supply. MakerDao also introduced the Smart Burn Engine, designed to utilize DAI from the Surplus Buffer. This initiative aims to purchase MKR tokens and pair them with DAI, depositing them into the Uniswap V2 DAI-MKR liquidity pool, providing alternative methods for managing MKR tokens. Despite MakerDAO's remarkable growth, DAI's market capitalization still experienced a decline, falling by approximately $90 million in July to $4.56 billion, as stablecoin liquidity dried up, given the lack of volatility and leverage available to borrowers.

On top of the positive fundamental developments at MakerDAO, Rune Christensen, the co-founder of MakerDAO, sold about 13 million LDO tokens and subsequently purchased 32,637 MKR tokens at an average price of $734. This move has already proven advantageous, with Rune's trade up over 50% based on the current price of MKR. Conversely, observations by anonymous Twitter user @0xSisyphus pointed out that A16Z and Paradigm, two prominent venture capital firms, are potentially selling MKR tokens. This speculation arose as both firms withdrew MKR from the governance contract and transferred it to Coinbase. It's worth noting that A16Z acquired 6% of the Maker supply in 2018 at a fully diluted value (FDV) of $250 million, and Paradigm acquired 5.5% of the Maker supply in 2019 at a $500 million FDV, meaning both investments have underperformed Ethereum significantly over the same period.

The crvUSD market cap briefly rose over $100m in July but retreated below $90m following a ~$5 million exploit of Conic Finance. Then, on the 30th of the month, some liquidity pools using ETH were exploited due to a compiler reentrancy vulnerability in the version of Vyper used to code the smart contracts. The pools impacted included alETH/ETH, msETH/ETH, pETH/ETH, and CRV/ETH. Teams attempted to whitehack as many pools as they could before they were exploited, and at the time of writing, it would appear that ~$50 million was lost. For context, these pools combined held a fraction of Curve’s TVL, but many users and protocols removed liquidity out of fear, and Curve’s TVL fell ~50%. Hopefully, this liquidity will return as things normalize.

The LSDFi narrative is witnessing a significant surge as the staking of ETH to the beacon chain continues. Users are actively depositing their liquid-staked ETH into protocols that allow them to capture higher yields or unlock new utility. The growing amount of staked Ether – 22M ETH staked across 700k validators, representing 19% of total supply and growing - is expected to yield benefits for these protocols, as they allow users to earn more ETH or create negative interest rate loans with their LSDs. Notably, Pendle, Lybra, and Origin protocols saw significant TVL growth last month. Moreover, the introduction of Yearn into the LSD scene has generated anticipation for the full launch of their st-yETH vault. We count $600M+ in TVL across these LSDFi protocols, up from $200M in May. We share details on three strong competitors below.

In July, Pendle introduced Pendle Earn, a streamlined version of their yield trading platform. This new offering allows users to earn an upfront fixed yield on their yield-bearing assets. While retaining the option for speculative and directional trading on variable yield, the protocol now enables users to toggle between Trade and Earn mode on their browser to access either the more comprehensive platform or, the newer simplified version. The rebranding of Pendle Earn has proven highly successful, evident in the significant increase in total value locked, which surged by approximately $30 million to reach $154M million this month, marking an impressive 24% growth.

Furthermore, Pendle has been granted support from ETH L2 Mantle Network, a strong signal of recognition and endorsement for Pendle as a new DeFi primitive. This grant incentivizes Pendle to expand its presence to the newly launched chain, showcasing the platform's growing reputation and appeal within the DeFi space. Pendle's achievements underscore the importance of simplifying user experiences in DeFi, as it often plays a pivotal role in driving user adoption of new innovative financial products in DeFi.

Source: VanEck Research, DefiLlama as of 7/31/23.

Lybra Finance, who launched their yield-bearing stablecoin, eUSD, continued to grow in July from $276 million TVL to over $380 million. The lion’s share of this growth came from the continued adoption of eUSD, which saw a $56 million increase in market cap from $136 million to $192 million at the time of writing. Additionally, Lybra released their v2 documentation, which will allow for new LSD products to be used as collateral and see LBR and peUSD deployed as LayerZero Omnichain Fungible Tokens (OFT) to be used on Arbitrum, among other protocol enhancements. This should only continue to bolster the protocol’s growth as more LSD liquidity is bridged to layer 2 blockchains to avoid the high transaction costs of Ethereum.

Origin Protocol saw significant growth in their liquid staked ether product, Origin Ether, which nearly doubled its TVL in July from $44m to $84m. This was mainly a result of the $110k incentive given to vlCVX holders to vote for CRV emissions to be distributed to the ETH+oETH pool on Curve. Additionally, 20% of protocol fees will go to lock CVX so the protocol can continue to incentivize the liquidity of their LSD product. Origin’s success this month highlights how protocols can leverage the existing DeFi ecosystem to incentivize protocol growth. By making it economically worthwhile for vlCVX holders to direct CRV emissions to the ETH-oETH pool, Origin can begin to create a flywheel effect. Users provide liquidity to earn CRV rewards, which grows the oETH TVL and allows Origin to lock more CVX, resulting in more incentives directed toward the ETH-oETH pool.

Yearn has commenced bootstrapping its yETH product this month in preparation for its full-scale launch. Following the closure of deposits last weekend, the product is set to launch with a Total Value Locked (TVL) of $3.9 million, having attracted ~$9,500 in monthly incentives from various LSD protocols and centralized exchanges offering LSD products. These entities are vying for significant allocations of the yETH LSD basket. Notably, Swell Network's largest incentive of ~$3,600 has been allocated to bolster swETH's initial weight in the vault, bolstering the product's appeal and potential yield generation. Based on the current proportion of incentives to deposits, it is estimated that the yETH product will provide an approximate annual percentage yield (APY) of ~3% on top of the yield derived from the underlying LSDs. Furthermore, with the inclusion of swap yields, the yETH vault is poised to be highly competitive compared to traditional LSDs.

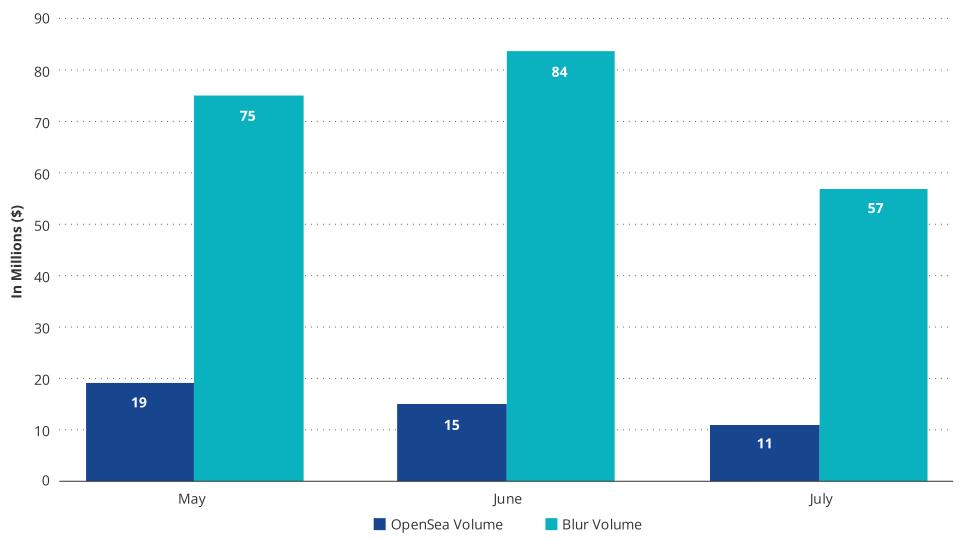

In the month of July, the NFT market experienced its fifth consecutive monthly decline in volume. Blur maintained its position as the leading NFT exchange by volume, accounting for over 70% of the total NFT volume. However, it's essential to recognize that despite its dominance in volume, OpenSea still outpaced Blur significantly in terms of users and trades, indicating that Blur's primary user base still consists mainly of NFT power users. Blur's peer-to-peer NFT lending platform, Blend, also remained a driving force in NFT loan markets, enabling nearly 94% of loan volume in July. However, there was a noticeable decline in NFT loans throughout the month, with the weekly average loan volume dropping from approximately $180 million in June to around $102 million.

Source: VanEck Research, @Hildobby as of 07/31/23.

Past performance is no guarantee of future results. Not intended as a recommendation to buy or sell any securities named herein.

The Market Vector Media and Entertainment Leaders Index returned -2% for the month of July, nearly matching ETH’s price decline. APE continued to sell off throughout the month, falling 16%, while its peers, SAND and MANA, recorded losses of only 2.5% and 4%, respectively. APE’s underperformance is magnified by its staking program, which rewards APE holders an unsustainable 49% APY for staking their tokens. Meanwhile, on the Web3 gaming front, active users across the top Web3 games we track fell by 2%, a symptom of the lackluster IP produced and the failure to address the needs of Web2 gamers.

In the Web3 gaming industry, a significant problem has become clear: an overestimation of additional features that truly resonate with gamers. The status quo indicates a strong preference among gamers for marketplaces that facilitate the buying and selling of in-game items, as exemplified by the thriving gray markets for trading Counter-Strike skins. We believe contemporary Web3 games must adopt a more focused approach, deploying smart contracts solely for elements that add tangible value to the gamer’s experience. Key aspects include representing valuable in-game items as NFTs on the backend and providing a web2-like interface for seamless item trading on the front end.

At the forefront of utilizing blockchain to deliver value to gamers, ImmutableX has been lauded for its emphasis on aggregating NFT liquidity, creating an intuitive wallet management experience through the Immutable Passport, and leveraging established online gaming marketplaces such as the Epic Game Store and Gamestop NFT marketplace. Mythical Games has also emerged as a prominent competitor by challenging the notion of needing the blockchain for anything other than NFTs representing in-game items. They have adopted a different strategy than many other games, launching their apps on major app stores despite Apple and Google's egregious 30% tax levied on in-app purchases while simultaneously establishing their marketplace, DMarket. This approach allows them to reach a broader audience and naturally incentivizes users to engage with DMarket due to more favorable pricing. Notably, DMarket has executed an impressive $162 million in NFT sales since its inception, as reported by Cryptoslam! Despite this success, the MYTH token has underperformed the broader crypto market.

Another noteworthy trend observed in the Web3 gaming space is the significance of valuable Intellectual Property (IP) tied to existing user interests. Successful games tend to center around popular sports themes, exemplified by Sorare, NBA TopShot, and NFL All Day. Mythical Games follows this trend with their NFL Rivals game, boasting over 1 million players and earning the prestigious position of being ranked as the #1 Sports game on the Apple app store, currently maintaining a strong position at #4.

As the Web3 gaming industry continues to evolve, staying attuned to gamer preferences and industry trends remains crucial for sustained success. Currently, we think the teams that address the most direct concerns from gamers and create games that appeal to things people already have a passion for (such as sports, fashion, and social experiences) will be the most successful. Given the lack of widespread adoption and the less robust monetization models of current gaming tokens, we have limited our investments in the space.

Links to third party websites are provided as a convenience and the inclusion of such links does not imply any endorsement, approval, investigation, verification or monitoring by us of any content or information contained within or accessible from the linked sites. By clicking on the link to a non-VanEck webpage, you acknowledge that you are entering a third-party website subject to its own terms and conditions. VanEck disclaims responsibility for content, legality of access or suitability of the third-party websites.

To receive more Digital Assets insights, subscribe for our Crypto Newsletter

Important Information

This is not financial research but the opinion of the author of the article. We publish this information to inform and educate about recent market developments and technological updates, not to give any recommendation for certain products or projects. The selection of articles should therefore not be understood as financial advice or recommendation for any specific product and/or digital asset. We may occasionally include analysis of past market, network performance expectations and/or on-chain performance. Historical performance is not indicative for future returns.

For informational and advertising purposes only.

For informational and advertising purposes only.

This information originates from VanEck (Europe) GmbH, Kreuznacher Straße 30, 60486 Frankfurt am Main. It is intended only to provide general and preliminary information to investors and shall not be construed as investment, legal or tax advice. VanEck (Europe) GmbH and its associated and affiliated companies (together “VanEck”) assume no liability with regards to any investment, divestment or retention decision taken by the investor on the basis of this information. Views and opinions expressed are current as of the date of this information and are subject to change with market conditions. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results. VanEck makes no representation or warranty, express or implied regarding the advisability of investing in securities or digital assets generally or in the product mentioned in this information (the “Product”) or the ability of the underlying Index to track the performance of the relevant digital assets market.

The underlying Index is the exclusive property of MarketVector Indexes GmbH, which has contracted with CryptoCompare Data Limited to maintain and calculate the Index. CryptoCompare Data Limited uses its best efforts to ensure that the Index is calculated correctly. Irrespective of its obligations towards the MarketVector Indexes GmbH, CryptoCompare Data Limited has no obligation to point out errors in the Index to third parties.

Investing is subject to risk, including the possible loss of principal up to the entire invested amount and the extreme volatility that ETNs experience. You must read the prospectus and KID before investing, in order to fully understand the potential risks and rewards associated with the decision to invest in the Product. The approved Prospectus is available at www.vaneck.com . Please note that the approval of the prospectus should not be understood as an endorsement of the Products offered or admitted to trading on a regulated market.

Performance quoted represents past performance, which is no guarantee of future results and which may be lower or higher than current performance.

Current performance may be lower or higher than average annual returns shown. Performance shows 12 month performance to the most recent Quarter end for each of the last 5yrs where available. E.g. '1st year' shows the most recent of these 12-month periods and '2nd year' shows the previous 12 month period and so on. Performance data is displayed in Base Currency terms, with net income reinvested, net of fees. Brokerage or transaction fees will apply. Investment return and the principal value of an investment will fluctuate. Notes may be worth more or less than their original cost when redeemed.

Index returns are not ETN returns and do not reflect any management fees or brokerage expenses. An index’s performance is not illustrative of the ETN’s performance. Investors cannot invest directly in the Index. Indices are not securities in which investments can be made.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of VanEck.

© VanEck (Europe) GmbH

This is a marketing communication. Please refer to the prospectus of the UCITS and to the KID before making any final investment decisions.

This information originates from VanEck (Europe) GmbH, which has been appointed as distributor of VanEck products in Europe by the Management Company VanEck Asset Management B.V., incorporated under Dutch law and registered with the Dutch Authority for the Financial Markets (AFM). VanEck (Europe) GmbH with registered address at Kreuznacher Str. 30, 60486 Frankfurt, Germany, is a financial services provider regulated by the Federal Financial Supervisory Authority in Germany (BaFin).

The information is intended only to provide general and preliminary information to investors and shall not be construed as investment, legal or tax advice VanEck (Europe) GmbH, VanEck Switzerland AG, VanEck Securities UK Limited and their associated and affiliated companies (together “VanEck”) assume no liability with regards to any investment, divestment or retention decision taken by the investor on the basis of this information. The views and opinions expressed are those of the author(s) but not necessarily those of VanEck. Opinions are current as of the publication date and are subject to change with market conditions. Certain statements contained herein may constitute projections, forecasts and other forward-looking statements, which do not reflect actual results. Information provided by third party sources is believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Brokerage or transaction fees may apply.

All performance information is based on historical data and does not predict future returns. Investing is subject to risk, including the possible loss of principal.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of VanEck.

© VanEck (Europe) GmbH / VanEck Asset Management B.V.

09 March 2026

09 March 2026