Welcome to VanEck

Select Investor Type

11 May 2023

Investors in the wild west of cryptocurrencies must evaluate a project's long-term viability but fear not. There are ways to do it! Examining a token's supply distribution and supply distribution schedule can help determine if a project is fairly launched and if its founders and developers are incentivized enough to see it through to completion.

Supply distribution refers to how a token's total supply is distributed among different entities. This distribution must be fair, or it can lead to centralization, manipulation, and market volatility. From time to time, a new project or layer-1 comes by (this time it was SUI that triggered me to write this story), which becomes a textbook example of how not to distribute tokens.

Imagine you’re in line for pizza, and you see that the people in front of you are getting a slice for just $1. Now you come up to the counter and they charge you $10 for the same slice! I know most people would be quite upset about this, but unfortunately, this is the reality that both traditional finance, and crypto live in. I have always been a strong supporter of crypto. Not just for the sake of decentralization or self-custody, but also for the ability to offer the same financial opportunities regardless of who you are. I always like to say that everyone buys Bitcoin for the price they deserve. Relative to future generations acquiring you may be better off taking the chance to be an early adopter. I think this is especially relevant for layer 1 cryptocurrencies, which aim to be a universal currency on and beyond their open-source platform.

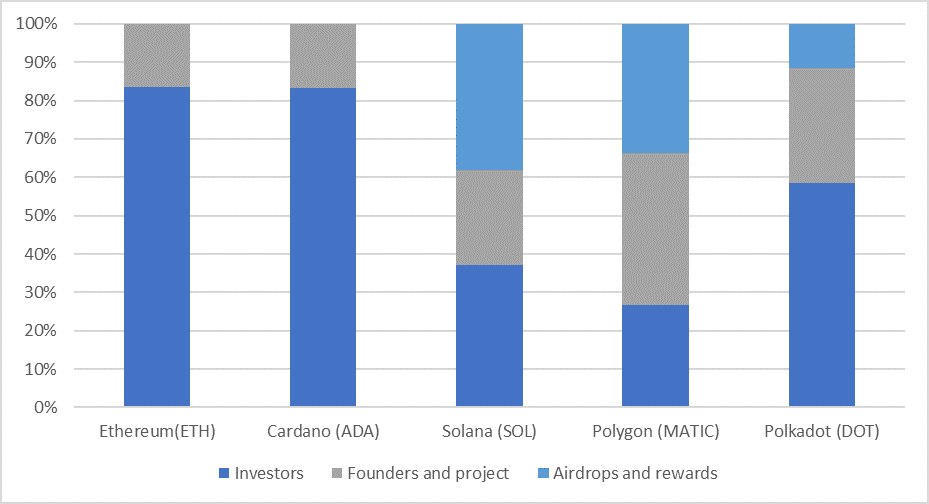

For many new tokens this analogy doesn’t work anymore, because token distributions and supply schedules have gotten a lot more complicated. Let’s use Sui (SUI) and Aptos (APT) as examples, both layer-1’s well known for being spin-offs of the failed Meta project “Diem”. A significant portion of tokens are reserved for the team, venture capital investors, early contributors and test net participants (largely comprising of VCs). It is only afterwards that the token is introduced to public sales, This can be done in a variety of ways, such as through investment tiers or lock drops. What does the initial token distribution look like for some well-known cryptocurrencies?

Source: Messari, data as of 30/04/2023.

Clearly, there is not just one recipe for success as all the top blockchain networks and their tokens are relatively successful compared to their competitors further down the line. Ethereum has a strong and community-driven development team which makes up for the lack of incentives. Solana has high incentives to build and use the technology but it lacks in terms of community relative to Ethereum.

For SUI, half the supply of the tokens is allocated to the Community Reserve—a fund managed by the Sui Foundation. This is significantly more than what we have seen in previous projects. Most of the remaining tokens will be allocated to those who contributed to the project, and 14% will be allocated to investors according to the Sui Foundation. SUI is meant to be a currency on the Sui network, but potentially outside of the network as well. Imagine if the ECB would do the same when developing a Digital Euro, it would create some social unrest. I know that this isn’t an entirely fair comparison because tokens are also used as a funding method and for their utility on the network. Perhaps projects should find other ways to reward team members, early contributors and the community as opposed to diluting the supply of the network’s currency.

Next, we should look at the supply distribution schedule. This is how the token supply is released over time, which can be done in various ways, including pre-mining, airdrops and lock drops. Pre-mining can give early investors and the project team an unfair advantage. Airdrops can artificially inflate the perceived value of a token, leading to market manipulation. Seed investments from venture capitalists can be a good sign, but they can also raise funds without selling tokens to the public. In most recent token drops, not all tokens are released at the time of sale. A significant portion of tokens are vested (essentially meaning that they are locked), and a portion of tokens become available periodically in a pre-programmed manner.

Investors should look for projects with a fair supply distribution that is diverse among different entities. This can help prevent centralization, market manipulation and create a sustainable ecosystem. Investors should also look for projects with a transparent supply distribution schedule that outlines how and when the token supply will be released over time. This transparency helps investors understand a project's long-term viability and gain confidence in its potential for success.

In conclusion, examining a token's supply distribution and supply distribution schedule is a useful way to evaluate a project's long-term viability. It ensures that a project is fairly launched and that its founders and developers are incentivized to see it through to completion. So, let's hope for a pizza party where everyone gets a fair share of the pizza. As always, investors should do their research before investing in any project.

Important Information

We publish this newsletter to inform and educate about recent market developments and technological updates, not to give any recommendation for certain products or projects. The selection of articles should therefore not be understood as financial advice or recommendation for any specific product and/or digital asset. We may occasionally include analysis of past market, network performance expectations and/or on-chain performance. Historical performance is not indicative for future returns.

ETN Disclaimer

Important information

For informational and advertising purposes only.

This information originates from VanEck (Europe) GmbH, Kreuznacher Straße 30, 60486 Frankfurt am Main. It is intended only to provide general and preliminary information to investors and shall not be construed as investment, legal or tax advice. VanEck (Europe) GmbH and its associated and affiliated companies (together “VanEck”) assume no liability with regards to any investment, divestment or retention decision taken by the investor on the basis of this information. Views and opinions expressed are current as of the date of this information and are subject to change with market conditions. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results. VanEck makes no representation or warranty, express or implied regarding the advisability of investing in securities or digital assets generally or in the product mentioned in this information (the “Product”) or the ability of the underlying Index to track the performance of the relevant digital assets market.

The underlying Index is the exclusive property of MarketVector Indexes GmbH, which has contracted with CryptoCompare Data Limited to maintain and calculate the Index. CryptoCompare Data Limited uses its best efforts to ensure that the Index is calculated correctly. Irrespective of its obligations towards the MarketVector Indexes GmbH, CryptoCompare Data Limited has no obligation to point out errors in the Index to third parties.

Investing is subject to risk, including the possible loss of principal up to the entire invested amount and the extreme volatility that ETNs experience. You must read the prospectus and KID before investing, in order to fully understand the potential risks and rewards associated with the decision to invest in the Product. The approved Prospectus is available at www.vaneck.com. Please note that the approval of the prospectus should not be understood as an endorsement of the Products offered or admitted to trading on a regulated market.

Performance quoted represents past performance, which is no guarantee of future results and which may be lower or higher than current performance.

Current performance may be lower or higher than average annual returns shown. Performance shows 12 month performance to the most recent Quarter end for each of the last 5yrs where available. E.g. '1st year' shows the most recent of these 12-month periods and '2nd year' shows the previous 12 month period and so on. Performance data is displayed in Base Currency terms, with net income reinvested, net of fees. Brokerage or transaction fees will apply. Investment return and the principal value of an investment will fluctuate. Notes may be worth more or less than their original cost when redeemed.

Index returns are not ETN returns and do not reflect any management fees or brokerage expenses. An index’s performance is not illustrative of the ETN’s performance. Investors cannot invest directly in the Index. Indices are not securities in which investments can be made.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of VanEck.

© VanEck (Europe) GmbH

This is a marketing communication. Please refer to the prospectus of the UCITS and to the KID before making any final investment decisions.

This information originates from VanEck (Europe) GmbH, which has been appointed as distributor of VanEck products in Europe by the Management Company VanEck Asset Management B.V., incorporated under Dutch law and registered with the Dutch Authority for the Financial Markets (AFM). VanEck (Europe) GmbH with registered address at Kreuznacher Str. 30, 60486 Frankfurt, Germany, is a financial services provider regulated by the Federal Financial Supervisory Authority in Germany (BaFin).

The information is intended only to provide general and preliminary information to investors and shall not be construed as investment, legal or tax advice VanEck (Europe) GmbH, VanEck Switzerland AG, VanEck Securities UK Limited and their associated and affiliated companies (together “VanEck”) assume no liability with regards to any investment, divestment or retention decision taken by the investor on the basis of this information. The views and opinions expressed are those of the author(s) but not necessarily those of VanEck. Opinions are current as of the publication date and are subject to change with market conditions. Certain statements contained herein may constitute projections, forecasts and other forward-looking statements, which do not reflect actual results. Information provided by third party sources is believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Brokerage or transaction fees may apply.

All performance information is based on historical data and does not predict future returns. Investing is subject to risk, including the possible loss of principal.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of VanEck.

© VanEck (Europe) GmbH / VanEck Asset Management B.V.

09 March 2026

09 March 2026