Welcome to VanEck

Select Investor Type

23 November 2020

As emerging markets (EM) countries waver between lifting and tightening COVID-19 related restrictions, we see a reacceleration of stay-at-home behavior. This trend is implicit in digitization, including online food delivery, payments, telemedicine, video entertainment, etc. In particular, online food delivery has grown substantially. We discussed trend acceleration1 in our recent blogs on Africa, Brazil and India, and food delivery is the top player in the digital acceleration club. Its structural growth trend is persistent across emerging markets and can be found in Asia, EMEA, LatAm and Africa – home to Meituan Dianping, Delivery Hero and Prosus N.V., some of the most resilient, innovative and disruptive portfolio companies in the Consumer Discretionary space.

“The COVID crisis has moved food delivery from a luxury to utility.”

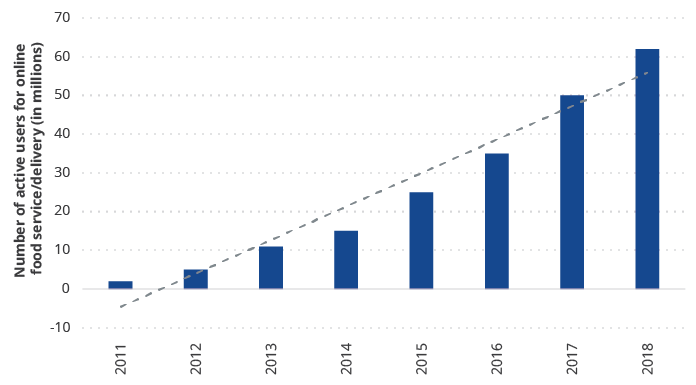

~ Dara Khosrowshahi (CEO, Uber), 2Q20 Earnings CallThe global food service delivery market is estimated to grow to $1 trillion USD in the long term.2 Urbanization, digital penetration and an increased demand for convenience (i.e., out-of-home delivery service) have been driving demand globally. In comparison to developed markets (DM), online food delivery in EM is at early stages of development, creating ample opportunity for structural growth investing and potential for alpha generation. We believe this is a long-term, sustainable, structural growth theme that will continue to trend upwards in the future.

Source: HSBC Global Research. Data as of October 2019.

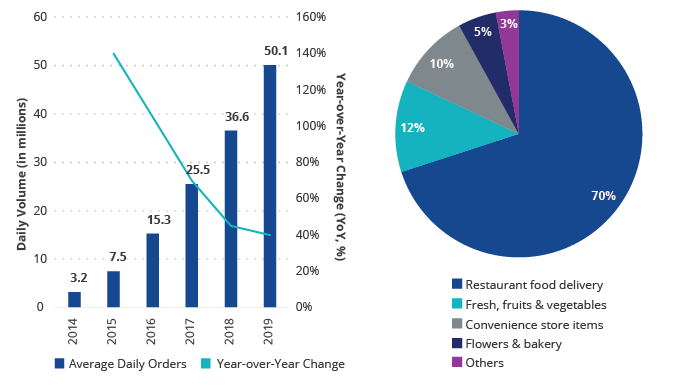

In many ways, China is at the leading edge of the online food delivery space globally. In its early years, the food delivery business model was a polarizing topic among investors. Many believed it was a model that was too difficult to build a sustainable moat around. A lack of differentiation among platforms and low user switching costs promoted aggressive price wars that bears being viewed as a race to the bottom with no path to profitability. Despite these challenges, Meituan has emerged as China’s food delivery leader. Their market leadership is built on superior execution led by their CEO Wang Xing, who is held in very high esteem in China’s tech community. As presented in charts below, the country’s total on-demand delivery orders reached over 50 million in 2019, with food delivery representing 70% of those orders.

Source: CFLP, Company Data, Goldman Sachs Global Investment Research. Data as of 11 June 2020.

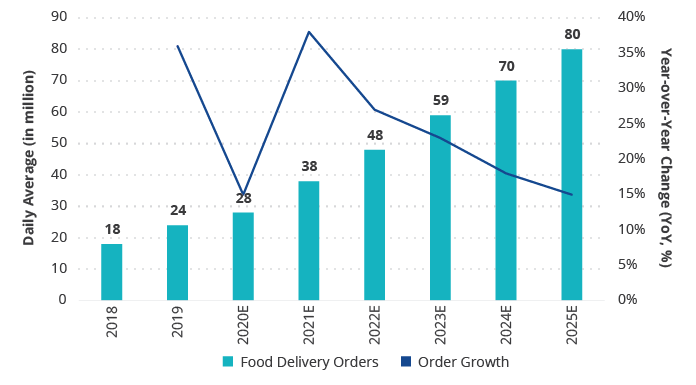

Meituan Dianping (2.19% of Strategy assets) is China’s leading e-commerce services platform company. Its apps connect consumers, including local businesses for food delivery, in-store dining, hotel bookings, among other services. Through strong execution on cross-selling an expanding array of lifestyle services to users and its merchant oriented focus, Meituan has become the largest food delivery network in the world, completing 25 million orders per day in 2Q 2020.3 We estimate Meituan’s online food delivery orders to grow to 80 million per day by 2025E.

Source: Company Data, Goldman Sachs Global Investment Research. Data as of 24 August 2020.

E = Estimates.

Our structural growth thesis is based on the following:

Meituan’s recent performance further consolidates our conviction in this portfolio company. It was primarily driven by a strong recovery in revenue, accompanied by greater than expected profitability. Sentiment was further boosted by market share gains in food delivery as well as new initiatives (e.g., groceries), which should serve to meaningfully expand the company’s target addressable market in the future.

Our EME team has been monitoring Meituan since its IPO in September 2018. However, it wasn’t until March 2020 that COVID created what we viewed as a compelling buying opportunity—when the stock sold off approximately 30% from peak to trough. Since then our initial thesis has played out nicely with Meituan emerging as a winner from COVID related lockdowns in China.

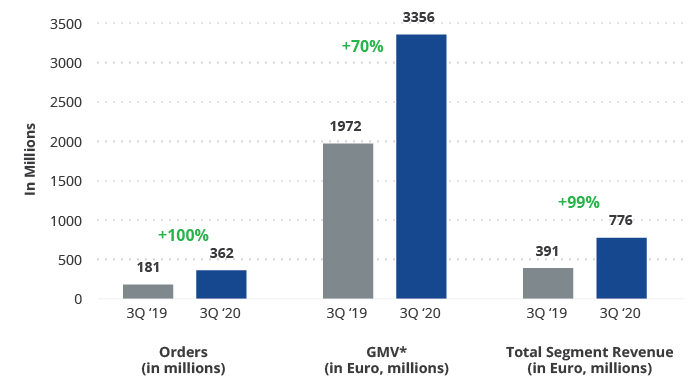

Delivery Hero (1.94% of Strategy assets)5 is an ambitious and truly inspiring food delivery service listed in Germany. While the company remains headquartered in Germany, most of its actual operations are based in emerging markets – spanning across EMEA, LatAm and Asia – operating in close to 50 countries globally and leading online food delivery in 90% of them.

Source: Company Data, 3Q20 Results Presentation. Data as of 30 September 2020.

*GMV = Gross Merchandise Value.

We believe that Delivery Hero’s scale and platform offer a unique play for EM structural growth. Our investment thesis is based on the following analysis:

Delivery Hero’s recent performance further reinforces our thesis – the company did, indeed, produce what we believe as “heroic” performance. There is now better appreciation that the company’s current level of investment will bear fruit. M&A activity in the sector has also shone a light on just how undervalued this sector has been. We have held a position in Delivery Hero since the IPO of the company in 2017 and continue to believe in the long-term prospects of the business.

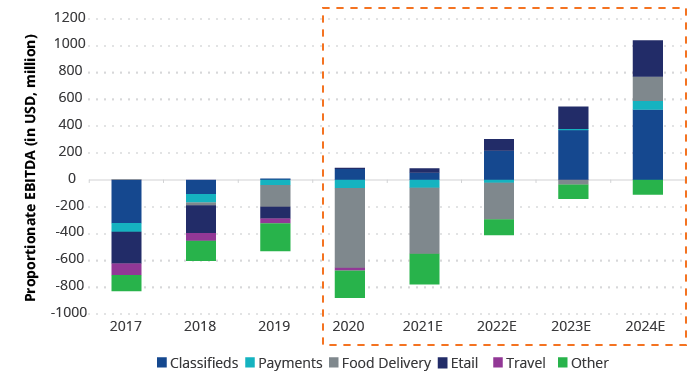

Prosus N.V. (2.86% of Strategy assets), a subsidiary and recent spinoff from our long-time holding in South Africa’s Naspers7, comprises a portfolio of leading digital assets outside of South Africa across Asia, Emerging Europe, MENA and LATAM. In addition to its 31% stake in Tencent Holdings and 21% stake in Delivery Hero (both portfolio companies in the Strategy), Prosus is heavily invested in three key e-commerce verticals – direct beneficiaries of the global digitization trend – online food delivery, online classifieds and payments & fintech.

Our structural growth thesis is based on the following:

While we expect further investments in this vertical in assets like Swiggy, we believe 2020 may mark peak losses in food delivery, with focus increasingly shifting from “land-grab” to profits.

Source: Company Data, Goldman Sachs Global Investment Research. Data as of 3 November 2020.

E = Estimates.

Prosus’ recent and expected performance has been solid across most verticals, and the stock has done well YTD. However, we have actually seen the share price’s discount to NAV (which remains dominated by Tencent) widening to historical highs, although we expect the earnings growth of the company’s ex-Tencent assets to outpace the earnings growth of Tencent over the coming three years. This should help narrow the discount going forward. Additionally, we have seen management engage in multiple large scale M&A attempts but remaining disciplined in not overpaying for assets in this environment, while recently announcing a $5 billion share buyback program split between Naspers and Prosus shares. We take this as a vote of confidence in the company’s future outlook and a reflection of management’s eagerness to unlock shareholder value, particularly given the current attractive valuation levels.

We have only held Prosus in the strategy since its spin-off from Naspers last year and its listing in the Netherlands to facilitate access to a wider base of global investors that may not prefer to invest in a Johannesburg Stock Exchange listed company. That said, Naspers itself is an old friend that we have held in the portfolio for many years and that has done well for us. We are encouraged by management’s increased disclosure levels and commitment to further unlock shareholder value, and we remain positive on the future prospects of the company.

Trend acceleration has been quite positive for the VanEck Emerging Markets Equity Strategy. Our focus on many of these structural growth areas enabled us to invest in Meituan Dianping, Delivery Hero and Prosus N.V. These companies are showing strong growth potential and recent earnings results further solidify our conviction in these names. As a result, our outlook is optimistic for the remainder of 2020 and beyond, despite the current challenges. A key driver of our outlook for the end of 2020 and beyond is an expectation of global growth recovery, boosted by a timely introduction of a COVID-19 vaccine and its distribution schedule.

1The global pandemic has accelerated growth in certain sectors and industries such as digital payments, e-commerce, data centers, telemedicine and video gaming, with disruption timelines shortening. This acceleration trend is quite positive for our active VanEck Emerging Markets Equity Strategy, as we have always been forward looking, focused on many of these structural growth areas and, as a result, we currently see that positive prospects for many of our portfolio companies actually accelerated.

2Source: HSBC Global Research. Data as of October 2019.

3Source: Company Data, Goldman Sachs Global Investment Research. Data as of 24 August 2020.

41P marketplace model means that the company sells its own inventory; whereas 3P model implies that the company operates platforms for other businesses to sell its inventory.

5Naspers owns a 21% stake in the company.

6The term “dark convenience store,” “dark supermarket” or “dotcom centre” refers to a retail outlet or distribution centre that caters exclusively for online shopping. A dark convenience store is generally a large warehouse that can either be used to facilitate a "click-and-collect" service, where a customer collects an item they have ordered online or as an order fulfilment platform for online sales.

7Naspers owns a majority stake (72.5%) in Prosus N.V.

This is a marketing communication. Please refer to the prospectus of the UCITS and to the KID before making any final investment decisions.

This information originates from VanEck (Europe) GmbH, which has been appointed as distributor of VanEck products in Europe by the Management Company VanEck Asset Management B.V., incorporated under Dutch law and registered with the Dutch Authority for the Financial Markets (AFM). VanEck (Europe) GmbH with registered address at Kreuznacher Str. 30, 60486 Frankfurt, Germany, is a financial services provider regulated by the Federal Financial Supervisory Authority in Germany (BaFin).

The information is intended only to provide general and preliminary information to investors and shall not be construed as investment, legal or tax advice VanEck (Europe) GmbH, VanEck Switzerland AG, VanEck Securities UK Limited and their associated and affiliated companies (together “VanEck”) assume no liability with regards to any investment, divestment or retention decision taken by the investor on the basis of this information. The views and opinions expressed are those of the author(s) but not necessarily those of VanEck. Opinions are current as of the publication date and are subject to change with market conditions. Certain statements contained herein may constitute projections, forecasts and other forward-looking statements, which do not reflect actual results. Information provided by third party sources is believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Brokerage or transaction fees may apply.

All performance information is based on historical data and does not predict future returns. Investing is subject to risk, including the possible loss of principal.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of VanEck.

© VanEck (Europe) GmbH / VanEck Asset Management B.V.

11 December 2025

11 December 2025