EM Asia - Signals on Growth, Inflation

21 October 2022

Read Time 2 MIN

Global Growth Headwinds

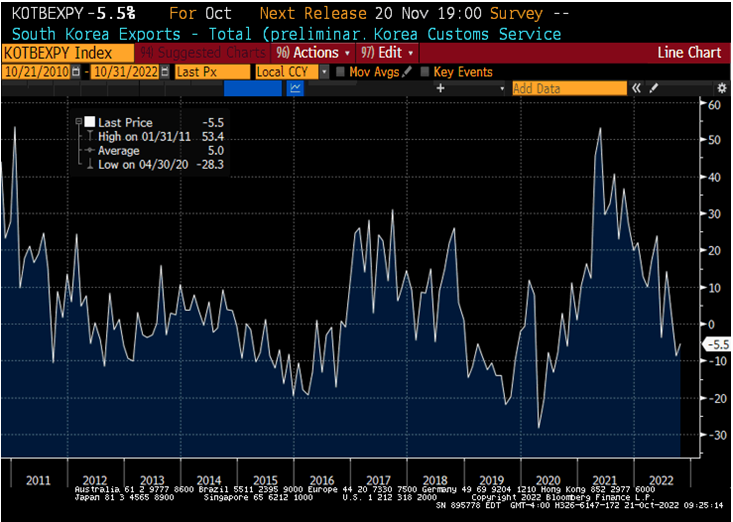

South Korea’s sluggish early-October exports added to concerns about the global growth outlook. South Korean trade numbers are often used as a gauge for global activity, so a 5.5% annual decline in 20-day exports (see chart below) did not go unnoticed. The fact that exports to China fell by 16.3% raised further questions about the policy response in the aftermath of the communist party congress. Today’s 40bps cut in the margin refinancing rates by the China Securities Finance Corporation suggests that the “targeted” approach is still the preferred one, but the new lineup of the Politburo Standing Committee (to be announced tomorrow) should signal whether this will still be the case going forward.

Asia Policy Tightening

Another reason we keep an eye on emerging markets (EM) Asia is that the region might actually be able to avoid the high inflation “curse” that plagued Emerging Europe and LATAM (as well as developed markets (DM)) for most of the year. Malaysia’s below-consensus headline inflation print comes on the heels of a downside inflation surprise in Indonesia – and it is also quite low in a global context (“mere” 4.5% year-on-year). Still, communications from the Indonesian central bank show that sticky core inflation is a risk – similar to Malaysia – and it warrants additional policy tightening (especially against the backdrop of solid domestic activity and the U.S. Dollar strength).

Inflation Pressures In LATAM

Weaker than expected retail sales in Mexico suggest that some domestic inflation pressures might be easing in that part of the world, but we’ll get a more definitive answer on Monday, after the release of bi-weekly inflation. The consensus sees tentative moderation in headline inflation, but not yet in core prices – and this means that another 75bps rate hike (to 10%) might still be on the table in early November. The latest market expectations see double-digit terminal rates in most LATAM economies – and there are still questions whether some countries (Chile) can stop tightening safely, and whether others (Colombia) would be under increasing pressure to accelerate hikes (Colombia). Stay tuned!

Chart at a Glance: Global Activity Gauge – Still Heading South

Source: Bloomberg LP.

Insights relacionados

Related Insights

10 fevereiro 2026

06 março 2025

20 fevereiro 2025

10 fevereiro 2026

A desvalorização está novamente em foco. Veja a seguir o que está impulsionando essa situação, o que poderia revertê-la e como estamos posicionando as carteiras para os dois cenários.

07 abril 2025

As tarifas de Trump provocam temores de guerra comercial, alimentando a volatilidade do mercado, o risco de inflação e as ameaças de recessão. Com prováveis retaliações globais, o crescimento de curto prazo está claramente em risco.

06 março 2025

As tarifas de Trump, a próxima fase da IA e uma possível reavaliação do ouro dos EUA podem abalar os mercados - os investidores que estiverem à frente dessas transições estarão mais bem posicionados.

20 fevereiro 2025

O avanço da IA na China, a inflação persistente, o desempenho superior do ouro e o aumento da demanda de energia destacam um cenário de investimentos em transformação.

16 janeiro 2025

Em 2025, lidar com as turbulências envolve equilibrar a inovação tecnológica, as estratégias para combater a inflação, as transformações no setor energético e os desafios derivados dos cortes de gastos e da inflação.