Political Games vs. Macro – Who Wins?

30 March 2023

Read Time 2 MIN

China Geopolitical Goals

Headlines about the rising tensions between the U.S. and China continue to flood our Bloomberg screens – fanning debates about China’s long-term geopolitical aspirations and the renminbi’s possible (or is it likely?) ascendance as one of the world’s reserve currencies at the expense of the good old greenback. Many emerging markets (EM) are watching these developments with great interest – a possibility of playing China against the U.S. might look attractive going forward – but for now many seem content with the fact that their economies are arguably more correlated with China’s post-pandemic rebound than with the U.S. Federal Reserve’s rate cycle or developed markets (DM) banking mayhem. This explains why the next batch of China’s activity gauges will be closely watched this evening. The consensus is cautious – both the services and the manufacturing PMIs are expected to stay in expansion zone, but with no further improvement.

EM Inflation Risks

The pace of China’s rebound is an important driver for China’s inflation outlook (very benign right now) and China’s “exported” inflation – including a wider impact on global commodity prices, which can affect the disinflation momentum in EM. The latest communications from various EM central banks sounded hawkish (surprisingly so in some instances), with upside inflation risks being a top concern. And EM hawks continued to dominate the newsflow this morning. Brazil’s quarterly inflation report talked about the need to maintain restrictive policy stance for now, while the South African central bank surprised with a larger than expected +50bps rate hike, raising this year’s inflation forecast. The rate-setting meetings in Mexico and Colombia this afternoon now look even more interesting.

EM Market Performance

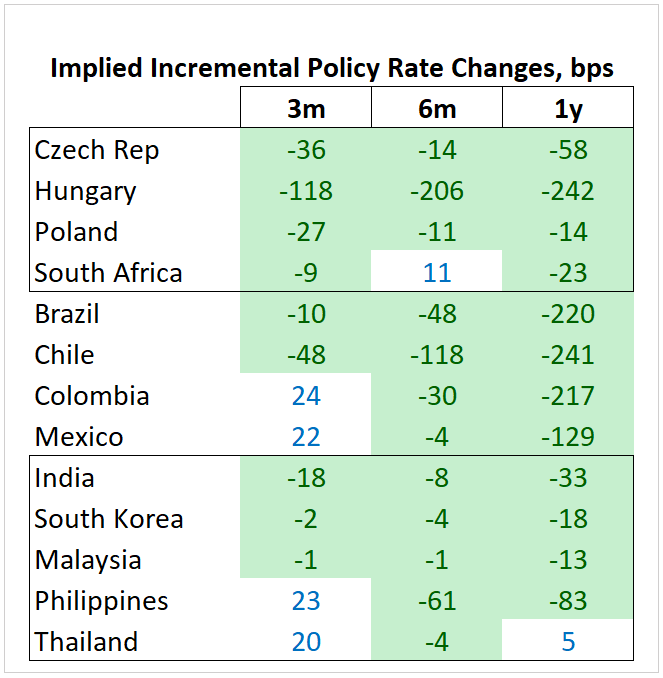

While this is happening, the market continues to price in EM rate cuts in the next six months. These expectations are on the optimistic side, but EMs’ “cautious for longer” policy bias can easily create more room for rate cuts in the fall and beyond. In the meantime, high real interest rates in EM can improve local bonds’ valuations and shelter EM currencies from market turmoil in DM. Stay tuned!

Chart at a Glance: Market Still Sees Rate Cuts in EM

Source: Bloomberg LP.

Insights relacionados

Related Insights

10 fevereiro 2026

06 março 2025

20 fevereiro 2025

10 fevereiro 2026

A desvalorização está novamente em foco. Veja a seguir o que está impulsionando essa situação, o que poderia revertê-la e como estamos posicionando as carteiras para os dois cenários.

07 abril 2025

As tarifas de Trump provocam temores de guerra comercial, alimentando a volatilidade do mercado, o risco de inflação e as ameaças de recessão. Com prováveis retaliações globais, o crescimento de curto prazo está claramente em risco.

06 março 2025

As tarifas de Trump, a próxima fase da IA e uma possível reavaliação do ouro dos EUA podem abalar os mercados - os investidores que estiverem à frente dessas transições estarão mais bem posicionados.

20 fevereiro 2025

O avanço da IA na China, a inflação persistente, o desempenho superior do ouro e o aumento da demanda de energia destacam um cenário de investimentos em transformação.

16 janeiro 2025

Em 2025, lidar com as turbulências envolve equilibrar a inovação tecnológica, as estratégias para combater a inflação, as transformações no setor energético e os desafios derivados dos cortes de gastos e da inflação.