Welcome to VanEck

Select Investor Type

06 November 2023

In October, Bitcoin experienced its most significant surge since January, witnessing increased flows into its ETNs and ETFs, partly driven by investor anticipation of upcoming Bitcoin ETF launches in the U.S.

Please note that VanEck may have a position(s) in the digital asset(s) described below.

Bitcoin surged by the most since January, +28% in October, as digital assets outpaced the Nasdaq (-2%) for the second month in a row. Large-caps (+21%) again beat small-caps (+4%), even as the ETH-to-BTC ratio fell below the levels set during the 3AC liquidation in June 2022. Demand for on-chain leverage remained somewhat muted, with DeFi TVL growth merely keeping pace with the incremental rise in ETH prices, hardly an impressive feat. Rather, the activity came from the regulated space: flows into Bitcoin ETNs and ETFs globally reached $412M in the month compared to $630M total YTD, while the Chicago Mercantile Exchange (CME’s) share of Bitcoin futures activity reached record levels (23%). We attribute this surge to astute investors positioning themselves ahead of the impending wave of roughly a dozen or so spot Bitcoin ETFs gearing to launch on U.S. securities exchanges by mid-January 2024.

| October | YTD | 365 days | |

| Bitcoin | 28% | 109% | 73% |

| MarketVectorTM Infrastructure Application Leaders Index | 28% | 56% | 15% |

| MarketVectorTM Smart Contract Leaders Index | 20% | -9% | -9% |

| MarketVectorTM Media & Entertainment Leaders Index | 16% | -29% | -58% |

| Ethereum | 9% | 51% | 19% |

| MarketVectorTM Decentralized Finance Leaders Index | 6% | 25% | -11% |

| Coinbase | 0% | 119% | 17% |

| MarketVectorTM Centralized Exchanges Index | 0% | -4% | -30% |

| S&P 500 Index | -1% | 10% | 10% |

| Nasdaq 100 Index | -3% | 23% | 18% |

Source: Bloomberg, as of 10/31/2023. Past performance is no guarantee of future results. Not intended as a recommendation to buy or sell any securities named herein.

Amidst the sharp sell-off in U.S. government debt, Bitcoin’s performance is gaining newfound attention from potential clients who shunned digital assets a year ago. Significantly, the TLT (iShares 20+ Year Treasuries, mkt cap $40B) ETF has fallen further, peak-to-now, than Bitcoin. Even the AGG (iShares Core U.S. Bond, mkt cap $90B) ETF now has a negative return over 5 years! Foreign central banks have been selling U.S. Treasuries and buying gold. Clients are increasingly asking if Bitcoin will be next.

US taxpayers are navigating a complex web of potentially indirectly funding via deficit spending, both sides of the Israeli war through direct aid to Israel, tax incentives for prestigious universities fostering radical leftist ideologies, and recent sanctions relief to Iran coupled with aid to Gaza. Amidst this hypocrisy, a compelling narrative touting “Bitcoin as a safe haven” is taking shape, championed by figures such as BlackRock’s Larry Fink, PIMCO advisor Mohamed El-Erian, and legendary hedge fund investor Stanley Druckenmiller. As the implications of G7 over-indebtedness become increasingly apparent to the average citizen and to America’s growing number of adversaries, we anticipate Bitcoin will thrive. Our observations in October revealed that crypto again demonstrated its strongest price performance during Asian trading hours.

As a personal aside, it is a sad irony that part of Bitcoin’s initial allure to this Jewish portfolio manager was the idea that it might be easier to memorize a 12-word seed phrase rather than try to insert diamonds in my derriere in the case of an extermination attempt or another Jewish diaspora. And while it is true that after viewing Hamas’ barbaric butchery on October 7th, I wonder if my passphrase would probably be extricated by some novel form of torture, my hope remains: that by introducing a harder standard of energy-backed money to the world, Bitcoin might absorb some of the entropy that alienates so many amidst so many polarizing issues. Indeed, even as I debated one particularly irksome pro-Hamas opponent on X, I found myself hours later liking one of her tweets, which read: “Separating money and state. Forget all else, this is the mission of Bitcoin.” Whatever facts we disagree on, and there appears to be a greater number of them now, we both trust the next Bitcoin block in ten minutes. I find that agreement profoundly valuable right now.

Regrettably, many G7 administrations’ approach to tech innovation diverges significantly from certain fundamental principles core to free speech. President Biden's executive order on AI, reportedly influenced by his viewing of the Tom Cruise film 'Mission Impossible – Dead Reckoning Part I,' which features a sentient and rogue AI causing submarine havoc, seeks to regulate the act of solving mathematical problems in public, necessitating government registration beyond a certain threshold. In a parallel effort, Senator Elizabeth Warren is striving to introduce provisions into the essential National Defense Authorization Act that would subject crypto miners, validators, and wallet providers to the Bank Secrecy Act and KYC requirements, a proposition that many entities deem an impractical endeavor. Recent regulations in the EU, Canada, and the UK have placed considerable strain on the open internet, compelling platforms like Meta and others to curtail free news content and implement subscription models. Some of these regulations impose considerable fines for 'misinformation,” an infraction determined by diktat. Opposing such trends, many crypto investors look forward to a potential victory by pro-Bitcoin candidate Javier Milei in Argentina’s Presidential run-off on November 19th as a potential catalyst to remind the world that self-sovereign currencies can play a role at the sovereign level, too.

Regrettably, many G7 administrations’ approach to tech innovation diverges significantly from certain fundamental principles core to free speech. President Biden's executive order on AI, reportedly influenced by his viewing of the Tom Cruise film 'Mission Impossible – Dead Reckoning Part I,' which features a sentient and rogue AI causing submarine havoc, seeks to regulate the act of solving mathematical problems in public, necessitating government registration beyond a certain threshold. In a parallel effort, Senator Elizabeth Warren is striving to introduce provisions into the essential National Defense Authorization Act that would subject crypto miners, validators, and wallet providers to the Bank Secrecy Act and KYC requirements, a proposition that many entities deem an impractical endeavor. Recent regulations in the EU, Canada, and the UK have placed considerable strain on the open internet, compelling platforms like Meta and others to curtail free news content and implement subscription models. Some of these regulations impose considerable fines for 'misinformation,” an infraction determined by diktat. Opposing such trends, many crypto investors look forward to a potential victory by pro-Bitcoin candidate Javier Milei in Argentina’s Presidential run-off on November 19th as a potential catalyst to remind the world that self-sovereign currencies can play a role at the sovereign level, too.

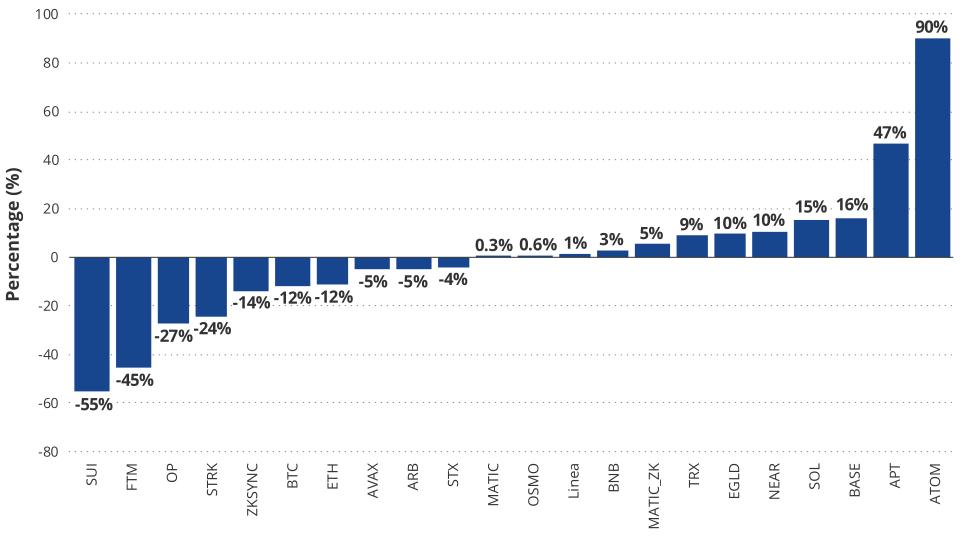

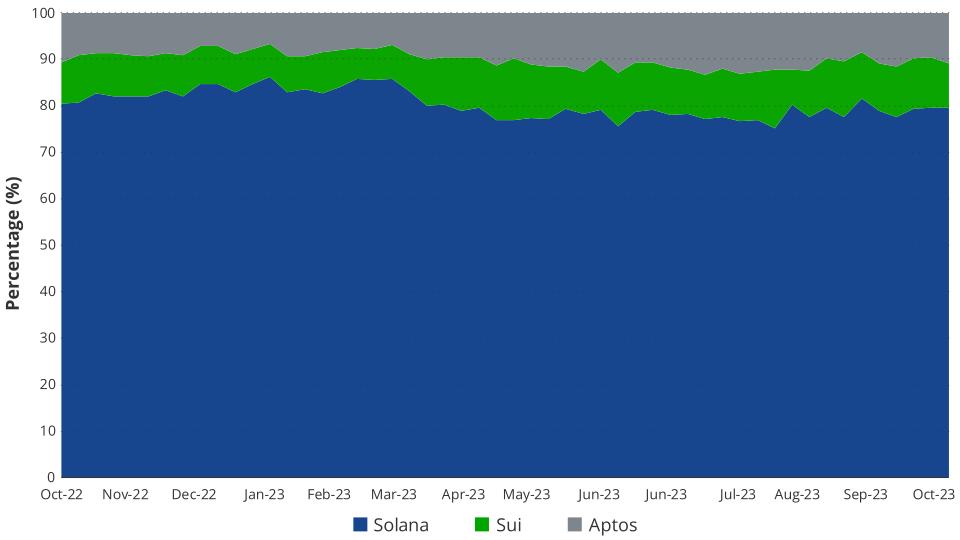

Smart contract platform tokens rallied 11.1% in October, and the total market cap (ex Bitcoin) grew from $268B to $298B. The top performers were Solana (+79%) and Stacks (+30%), while the laggards for the month were Sui (-6%) and ATOM (+9%).

Source: Artemis XYZ as of 10/31/2023 . Past performance is no guarantee of future results. Not intended as a recommendation to buy or sell any securities named herein.

Source: Artemis XYZ as of 10/31/2023. Past performance is no guarantee of future results. Not intended as a recommendation to buy or sell any securities named herein.

The Ethereum ecosystem, including its L2 smart contract platforms, was again front and center in the October news cycle. On October 11, Ethereum saw its validator queue empty, indicating that there was no waiting line for new entities to stake ETH and become a validator for Ethereum. Although more than 14k validators joined the network in October, demand was insufficient to create a queue, and this is the first time since the Merge in September 2022 that this has occurred. Consequently, the Ethereum annualized staking rate reached its lowest level since the Merge on October 15th at 3.5% before rallying to end the month at 4.12% as prices rebounded.

Meanwhile, the focus on L2 technology is heating up as zero-knowledge (ZK) L2 Zk Scroll launched on October 17th and has amassed $10.5M in TVL at the time of writing. Scroll joins existing zero knowledge L2 players Polygon zkEVM, Starkware, and ZkSync Era. To many in the crypto space, zk Layer-2s are a massive improvement over existing optimistic L2s like Arbitrum, Optimism, and Base. Layer-2s that use zk technology post proofs of the transactions that occur on their L2 directly to Ethereum. By contrast, optimistic L2s post a batch of transactions to an L2 without proof of authenticity. As a result, another party can challenge the authenticity of optimistic L2 batches and force the L2 to reverse them if they are incorrect. The advantage of zk L2s is that they enable faster bridging back to Ethereum which can be accomplished in as little as 15 minutes. By contrast, optimistic L2s force a withdrawer to wait 7 days, the challenge period where someone can prove fraud, before they can move their assets off an L2. The tradeoff is that zk Layer-2s cost slightly more to users to transact upon due to the cost of posting large proofs to Ethereum. Long term, zk L2s believe transactions costs will be cheaper as the per-transaction cost will scale down with an increase in the volume of transactions.

Source: Artemis XYZ as of 10/31/2023. Past performance is no guarantee of future results. Not intended as a recommendation to buy or sell any securities named herein.

Another interesting development for zk Layer-2s was the news that popular blockchains Canto and Astar will launch new networks through Polygon’s network of zk chains. Polygon also saw the stand-up of its new token to replace the MATIC token called POL. The token is part of Polygon’s shift to a zk-centric network, and the POL token, unlike the garishly named MATIC, will have inflation, which will be 2% per year. According to the Polygon team, half of the inflation will be used to invest in projects building on Polygon, while the other half will be allocated towards securing the network through validator payments. At its core. Polygon’s new zk approach is a fascinating new direction that could prove sagacious depending upon adoption of its new approach. Like Ethereum, Polygon is moving away from simply being a transaction execution environment and becoming a settlement layer. Additionally, though Starkware does not have a live token, the Israeli team announced in October that they would delay token unlocks for the future token from 11/29/2023 until 4/15/2024. Clearly, Starkware will be releasing its token in the near future.

Not to be left behind, L2 Arbitrum came out with several announcements, including the anticipated launch of their Orbit project. This would allow Arbitrum to scale to more users by enabling developers to create L3 chains that settle their activity to Arbitrum. This would make Arbitrum into a settlement and execution layer similar to Ethereum. Arbitrum also announced its L3s would use Celestia as a data availability layer. Finally, Arbitrum concluded voting on its Short-Term Incentive Program (STIP) that allocates $50M worth of ARB tokens to various projects on Arbitrum’s chain. Big winners included Camelot, GMX, Dopex, Jones, and Galxe.

Other Interesting News Items:

Uniswap charging 0.15% on its frontend for trades.

dYdX launching an app chain in the Cosmos.

Shrapnel, a game on Arbitrum, raising $20M.

BNB launches a data storage competitor to Filecoin called Greenfield.

Polkadot V2 which increases the number of parachains (Polkadot L2s), improved tokenomics, and a lower cost of security for projects building on Polkadot.

Circle partnering with Family Mart in Taiwan to allow Family Mart customers to trade in their frequent shopper points for USDC on the BitoPro crypto exchange.

Frax stablecoin issuer expanding to offer access to T-Bills on chain through its v3 upgrade.

Source: Artemis XYZ as of 10/31/2023.Past performance is not indicative of future results. Not intended as a recommendation to buy or sell any of the names mentioned herein.

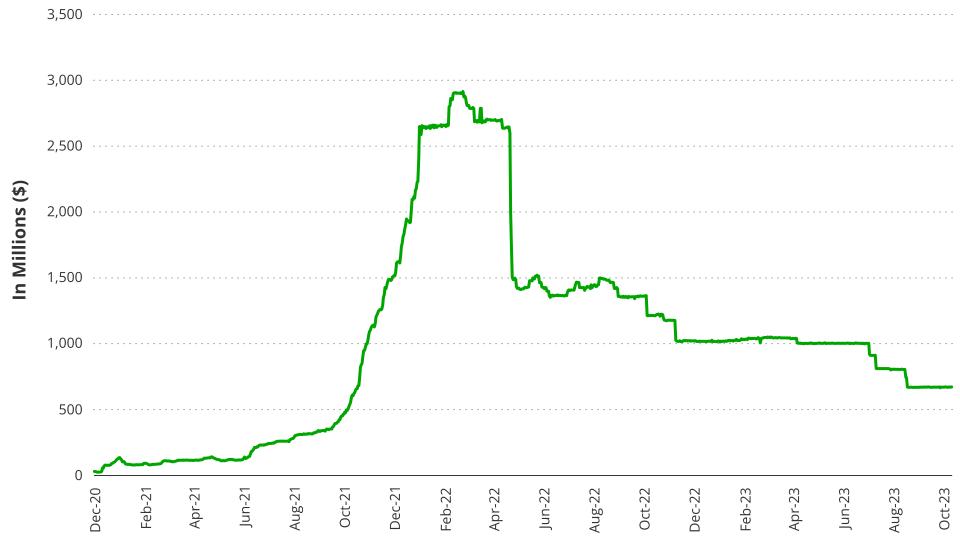

Solana’s SOL (79.3+%) token washed away almost a year of bearish vibes with a much-welcome rally in October. In the aftermath of FTX immolation in November 2022, SOL’s price nosedived from the mid-$30 range in early November 2022 to trade as low as $8 on December 29, 2022. After FTX collapsed, the chief backer of Solana was consigned to the glue factory, and with Solana facing a flood of token unlocks, it was assumed that Solana would be joining FTX in the afterlife. Solana was seemingly left with an ecosystem in shambles as many projects lost funding while others saw their on-chain activity dwindle below economic sustainability. As a result of the death of these ventures, individuals, and entities who used Solana pulled their stablecoins that were on Solana, and the total market cap of stablecoins fell from $1.85B on Jan 1, 2023, to a low of $1.44B on October 17, 2023.

Despite the flurry of bad news and languishing SOL price, Solana continued to innovate, as did projects in the Solana ecosystem. Interesting projects we like, including consumer-relevant applications such as Hivemapper, Render, and Helium, continue to attract users. Additionally, the Solana Foundation launched a programming interface for developers to create mobile phone applications for Solana called the Solana Mobile Stack, and Solana even launched its own phone. Coming into October, many investors were lukewarm on Solana due to the overhang of the FTX estate liquidating large chunks of tokens, investor token unlocks, and the popularity of Ethereum L2s that had TVLs surpass that of Solana’s.

In mid-October, however, it was noticed that the FTX estate had staked 5.5M (out of the 58.9M they hold or will receive) Solana tokens worth $122M that many feared would be sold to pay be creditors. The positive news for Solana continued from there with the core Solana project called Squads, a multi-sig, inking a $5.7M VC raise, ensuring it ample runway to continue to provide its pivotal services on Solana. Activity for Solana also significantly picked up as usership increased, surging Solana fees by more than 18%. This uptick in activity helped drive Solana DeFi TVL to advance by 6%. At the same time, the narrative for yield generation from on-chain activity, including MEV using Solana liquid staking tokens (LSTs), also accelerated. Popular liquid staking and MEV facilitator Jito was the chief beneficiary of SOL LSTs, attracting a 70% increase in SOL. Another positive development for Solana in October included the introduction of an encrypted token standard that allows anyone to obscure balances of these tokens from other users. Given that Solana’s ecosystem is still recovering, it was also encouraging to see Solana Labs introduce a new incubator program for nascent Solana projects.

For more on the potential of Solana, please see , including a financial model that anticipates up to $8B in revenues to SOL token-holders by 2030.

Source: Dune as of 10/31/2023. Past performance is not indicative of future results. Not intended as a recommendation to buy or sell any of the names mentioned herein.

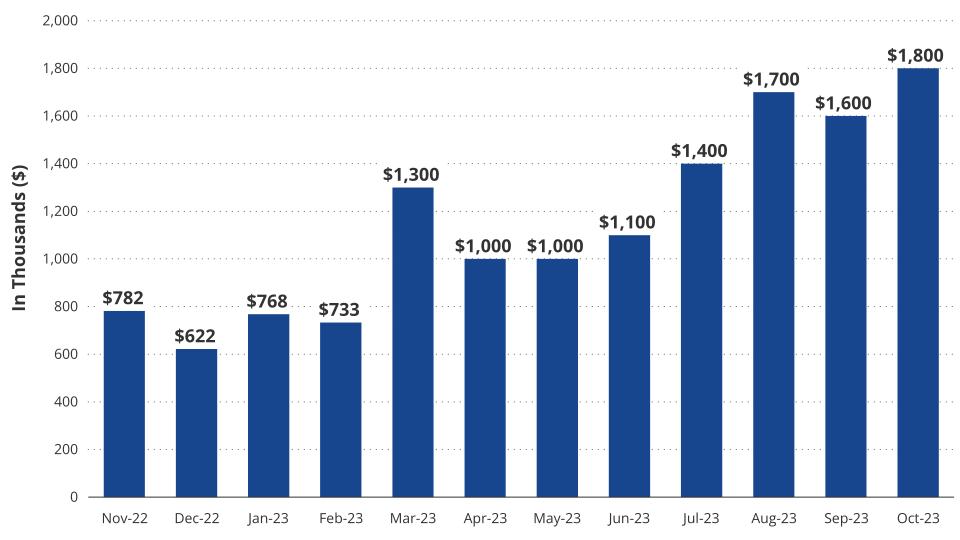

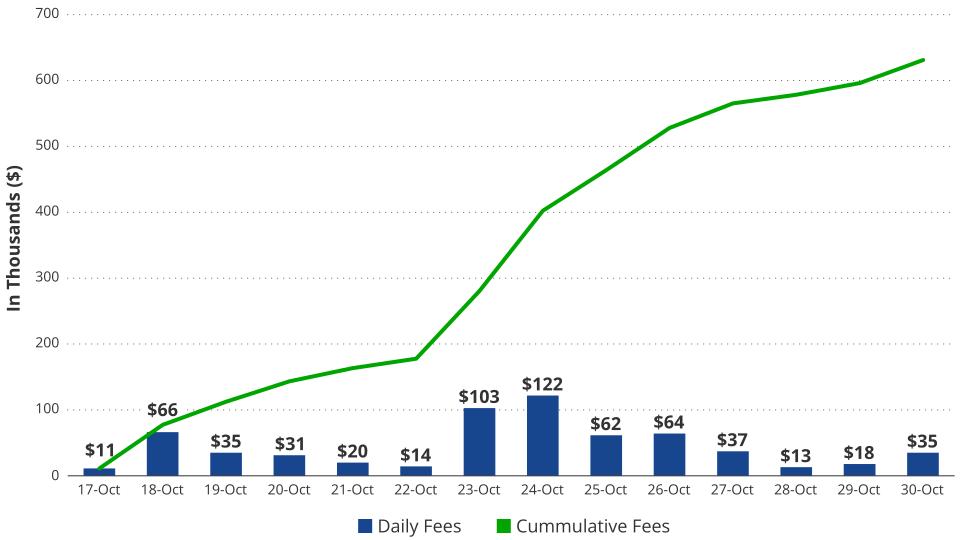

Stacks, a smart contract platform that rests upon the Bitcoin network and utilizes BTC, was the other largest winner in October, gaining (+34%). Part of this is undoubtedly because it is a leveraged play to the price of BTC, which had a blockbuster month (+24%), outperforming Ethereum. Curiously, activity on Stacks did not change much from September, measured by DEX volumes, daily transactions, or daily active addresses. However, while daily fees did increase by 60%, the average daily fee for October was only $200. TVL did grow meaningfully on Stacks as it rose from $13.8M at the beginning of the month to $25M as of October 27. Positive news included Digital asset custody firm Copper stating that it would integrate support for Stacks for Copper customers.

Part of STX’s price fortune stems from the misfortunes of Stack’s competitors. In mid-October, a security researcher for the Lightning Network announced he had uncovered an attack vector for the Lightning Network that could cause the network to be halted. As a result, the researcher named Antoine Riard declared he would stop his work on the Lightning Network. However, others contend that the Lighting Network is safe, and as of October 27, BTC locked on the Lightning Network was at 5,920, which was up from 4,420 at the start of October.

Source: Artemis XYZ as of 10/31/2023. Past performance is not indicative of future results. Not intended as a recommendation to buy or sell any of the names mentioned herein.

Sui (-6%), despite initial early potential, has continued to languish as it fails to attract developers and users to its ecosystem. Compared to the month of September, the daily active users on Sui have fallen by (-55%). Though DEX volumes have increased by 240% and TVL has jumped by 87%, the increase in activity is overshadowed by high rewards inflation and investor token unlocks. The increase in floating tokens was 7.3% just for the month of October, as more than 67M tokens were added to the supply. This brings the total number of tokens to 906M. However, the token dilution becomes worse as time progresses due to an aggressive unlock schedule for early investors and team members. By this time next year, there will be 2.7B Sui tokens in circulation. Of that, around 1.05B will be in the hands of early investors of Sui. Facing a 3x supply overhang over the next year is a substantial burden that anyone token holder must reconcile no matter how vibrant Sui’s ecosystem becomes. In October, the token dilution issue came to a head as South Korean regulators accused the Sui Foundation of manipulating the supply of tokens. Though Sui denies the rumors of doing anything illegal, the South Korean Financial Supervisory Service announced that it would be launching an investigation into the distribution of the Sui token.

Amid the negative news, Sui awarded over $1M in grants to programs building in its ecosystem. Additionally, they announced a new $51.3M ecosystem fund to support DeFi projects building on Sui. This development is particularly important given the lack of adoption by developers. Sui’s is programmed using Move, which is the same language as Aptos and very similar, because Move is based on Rust, to the language that Solana employs. The result is that Sui is directly competing with those other two ecosystems for developers. Solana, as an incumbent with a strong community identity, continues to maintain its developer share, but Sui could potentially catch up if its ecosystem stirs development interest.

Source: Artemis XYZ as of 10/31/2023. Past performance is not indicative of future results. Not intended as a recommendation to buy or sell any of the names mentioned herein.

Despite a mid-month rally alongside the rest of the SCP market, ATOM ended the month up only (+9%) amid continued concerns with its business model and how it will capture revenue from its ecosystem’s success. The key issue going forward is going to be the willingness of projects to come into the ATOM Economic Zone (AEZ) to lease security from ATOM’s Cosmos Hub blockchain. Though some important projects will be using ATOM for security, including Neutron, Stride, and Noble (eventually), many of the most vibrant projects in the Cosmos contend they will not use the Cosmos Hub. Though lack of Hub business success is not something new in October, it is a serious condition that is limiting Cosmos and could prove terminal to ATOM if things do not improve. Though the Cosmos ecosystem attracts the third most developers in crypto behind Polkadot and Ethereum, those figures are irrelevant to the Cosmos ATOM token until the Cosmos Hub is able to get other projects aligned with its needs. Another longstanding issue weighing on the ATOM’s price is concern over inflation. The ATOM token inflation rate is very high at 16.5% per year, and this is one of the highest among SCPs. Until these issues are resolved, ATOM will have great difficulty matching the performance of the Cosmos ecosystem or competitor blockchains.

Despite the negative news for ATOM, there are some positive trends. Surprisingly, Cosmos had one of the best gains of users in October compared to September, with (+90%) in daily active users. Additionally, the Blockworks team and others are working on proposals to change ATOM’s tokenomics. These plans include focusing the Cosmos Hub’s business approach to other blockchains and reducing inflation of the Cosmos Hub. At the same time, two important projects launched in the Cosmos in October, and they could attract more interest in the Cosmos Hub. Celestia, the first of the new Data Availability blockchains, and dYdX, the dominant derivative DEX, both launched their mainets in October. Finally, earlier in the month, the Cosmos chain Noble launched native USDC in the Cosmos which will allow anyone to mint native USDC through the Noble chain and transport across the 64 active Cosmos chains.

Source: DeFi Llama as of 10/31/2023. Past performance is not indicative of future results. Not intended as a recommendation to buy or sell any of the names mentioned herein.

The MarketVector Decentralized Finance Leaders index (MVDFLE) recorded a 5.8% increase during the month, underperforming the rally in Bitcoin and Ethereum. Among the index components, UNI, MKR, and CRV underperformed significantly, returning -9%, -12%, and -9%, respectively. In contrast, AAVE, RUNE, and LDO rallied 19%, 47%, and 5%.

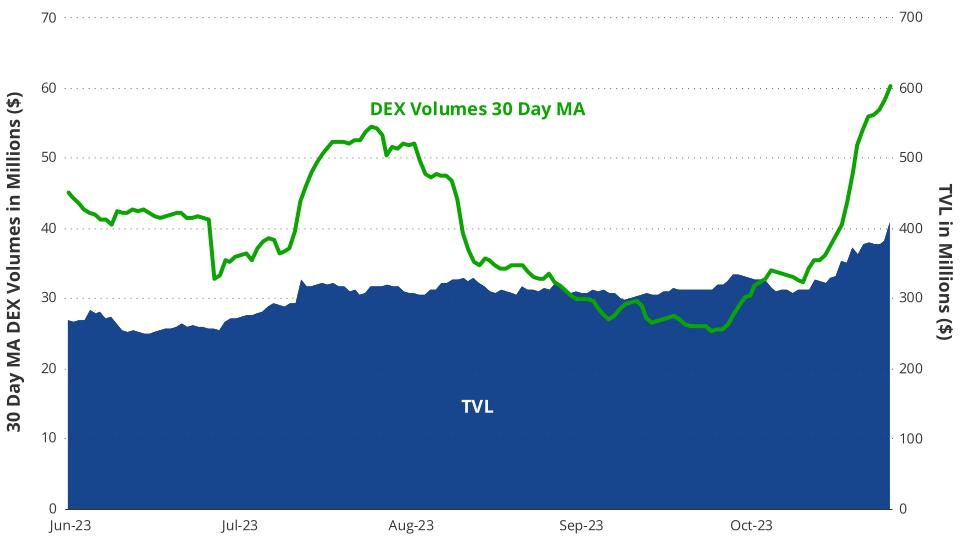

The underperformance of DeFi as a whole is not surprising, considering the rally in digital assets was led by Bitcoin, and DeFi tokens typically trade better when ETH leads the market. Notably, the top-performing tokens in the index have established substantial dominance in their respective areas of the crypto market, with Aave being the largest lending market, Lido a clear winner in ETH liquid staking, and Thorchain (RUNE) as the dominant decentralized exchange for native BTC and ETH swaps. Decentralized exchange (DEX) volume and the total value locked (TVL) in DeFi experienced significant reversals this month, with DeFi trading volume jumping 26% to $55.7 billion and the TVL across DeFi rising 8% to $41.7 billion. Arbitrum, Thorchain, and Solana experienced the largest surges in DEX volume, rising 53%, 146%, and 115%, respectively. The relative outperformance in DEX volumes across these chains suggests that they are becoming the preferred chains for trading digital assets outside of Ethereum.

Thorchain (RUNE) performed exceptionally well this month due to its dominant position as the most decentralized protocol for swapping native BTC and ETH. The decentralized exchange saw its volume more than double from September to $2.46 billion as investors flocked to acquire Bitcoin, anticipating the tailwinds from a potential U.S. spot Bitcoin ETF and the upcoming Bitcoin halving. While Thorchain’s decentralization comes with a few regulatory concerns, such as the FTX exploiter using the protocol to exchange stolen funds, investors seemed ultimately unconcerned as they rushed to buy RUNE this month.

Source: Token Terminal as of 10/31/2023. Past performance is not indicative of future results. Not intended as a recommendation to buy or sell any of the names mentioned herein.

Aave outperformance this month was driven by a short squeeze on centralized exchanges that led to the liquidation of over $2 million in short positions within a span of three days, alongside positive fundamental growth. Moreover, investors may be strategically positioning themselves in AAVE due to several fundamental factors favoring the protocol. With the recent upsurge in crypto market volatility, Aave is poised to bolster its daily revenue through the liquidation of overleveraged users and the heightened demand for stablecoins, often signaling the onset of a cryptocurrency bull market.

As the predominant lending protocol in DeFi, the borrow rate for USDC on Aave serves as a valuable indicator of the market's appetite for leverage. Users typically deposit their favorite digital assets as collateral and borrow USDC to increase their exposure. During the bear market, the borrow rate for USDC on Aave remained at approximately 4%. However, it has surged to 12% on the V3 market and 19% on V2, signifying that on-chain investors are leveraging their exposure to volatile digital assets in anticipation of a bull market. Aave's daily revenue has surged in tandem with higher borrow rates. According to Token Terminal, Aave's monthly revenue has more than doubled since the start of the year, rising to $1.8 million this month.

Source: The Block as of 10/30/2023. Past performance is not indicative of future results. Not intended as a recommendation to buy or sell any of the names mentioned herein.

In the middle of the month, Uniswap Labs made the decision to impose a 0.15% swap fee on transactions conducted via their Uniswap front end and within the Uniswap Wallet. This fee applies to swaps involving ETH, USDC, WETH, USDT, DAI, WBTC, agEUR, GUSD, LUSD, EUROC, and XSGD as both the input and output tokens, excluding swaps between stablecoins. Since its introduction, the frontend has collected $631k in fees, indicating a potential annual revenue of over $15 million for Uniswap Labs. This move has generated discontent within the community, as some perceive it as a signal that Uniswap Labs prioritizes enhancing the value of their equity over promoting value accrual to the Uniswap token. The reason why Uniswap Labs could want to do this despite owning a large amount of UNI is that driving value to the token could be accompanied with regulatory scrutiny if it leads to the UNI token being deemed an unregistered security. The community's dissatisfaction is rooted in a prolonged debate spanning several years regarding the activation of the "fee switch" to generate revenue from liquidity provider earnings on the Uniswap protocol. Back in June, the Uniswap DAO nearly voted to activate the fee switch, but the vote ultimately failed due to regulatory apprehensions from venture capital teams holding significant UNI tokens and Uniswap Labs equity. The contentious nature of this debate contributed to the underperformance of the UNI token during crypto’s rally in October.

Source: Coingecko as of 10/31/2023. Past performance is not indicative of future results. Not intended as a recommendation to buy or sell any of the names mentioned herein.

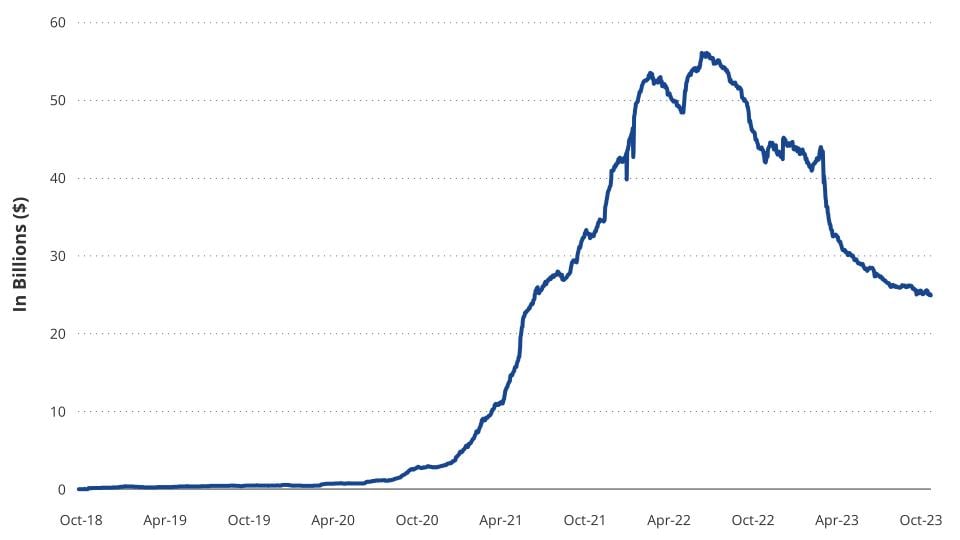

Frax Finance is following in the footsteps of MakerDAO by introducing a staking product for their FRAX stablecoin, known as sFRAX. Utilizing the non-profit entity established by the DAO, FinResPBC, the Frax DAO can now custody Real World Assets (RWAs) off-chain and offer users a yield on sFRAX just below the Interest Rate on Reserve Balances (IORB). Currently, sFRAX has seen a decent amount of adoption, with the amount of FRAX deposited surpassing 44 million. While the strong early growth is a good sign for sFRAX, it is still only a fraction of the amount that Maker has seen deposited into sDAI, which boosted DAI’s market capitalization by 20% and stands today at around $1.5 billion in deposits.

While sFRAX shares similarities with sDAI, there are key distinctions. Notably, MakerDAO's governance dictates the yield earned by sDAI holders via the Enhanced DAI Savings Rate (DSR), which decreases the effective yield for depositors as the DSR utilization increases. Currently, Maker's DSR has a utilization rate of around 30%, meaning nearly one-third of all DAI is deposited in the DSR and receiving yield payouts from MakerDAO. However, once the utilization rate reaches 35%, the yield for depositors will decline to 4.32% and remain at that level even if utilization decreases back to below 35%. In contrast, the yield for sFRAX depositors is solely based on the IORB rate, adjusted slightly lower (0.05%-0.1%) to account for fees related to capital movement between RWAs and on-chain assets. Notably, this ensures that the yield for sFRAX depositors remains unaffected by the actions of other investors but only by fluctuations in short-term interest rates. Consequently, it's likely that sFRAX will become a more capital-efficient means of capturing yield over the long term compared to sDAI. If Maker's rates decrease and the benefits of switching from sDAI to sFRAX become more apparent, we may witness a transition of investors towards holding sFRAX.

Source: Cryptoslam as of 10/31/2023. Past performance is not indicative of future results. Not intended as a recommendation to buy or sell any of the names mentioned herein.

NFT volume saw a small but insignificant increase this month, rising only $7 million to $306 million. Despite the poor volume of the overall NFT market, Blur made strides in market share, with volume this month growing to $132 million, excluding wash sales and its share of the Ethereum NFT exchange marketplace rising to over 60% from 55%. The rise in volume on Blur was influenced by the upcoming end of season 2 farming rewards on November 20th, which will see over 300 million Blur airdropped to users of the protocol. The airdrop gained significant value this month as the price of BLUR rallied 31% on the announcement of a governance proposal to enable a fee on the exchange’s volume. After some discussion by the community, it appears that the DAO will likely vote on whether or not to enable a 0.5% fee on volume. Additionally, the fee would likely be accompanied by a locking mechanism, which would help to sink many of the tokens that will be distributed in the season 2 airdrop and dissuade farmers from dumping them on the market. Those who have voiced their opinions against the proposal have indicated that it could lead to Blur losing its dominant market share, while community members in support have highlighted that there is no utility or value accrual to BLUR and progress on this front needs to be made to support the token valuation. After BLUR’s strong rally this month, it would appear that the market agrees with the latter. For context, if this fee had been applied to both Blur’s exchange and lending volume over the last month, it would have generated just under $2 million in cash flow for the DAO, which could then be used for token buybacks and distributed to owners who lock their tokens.

Source: DUNE: @Cryptokoryo as of 10/29/23. Past performance is not indicative of future results. Not intended as a recommendation to buy or sell any of the names mentioned herein.

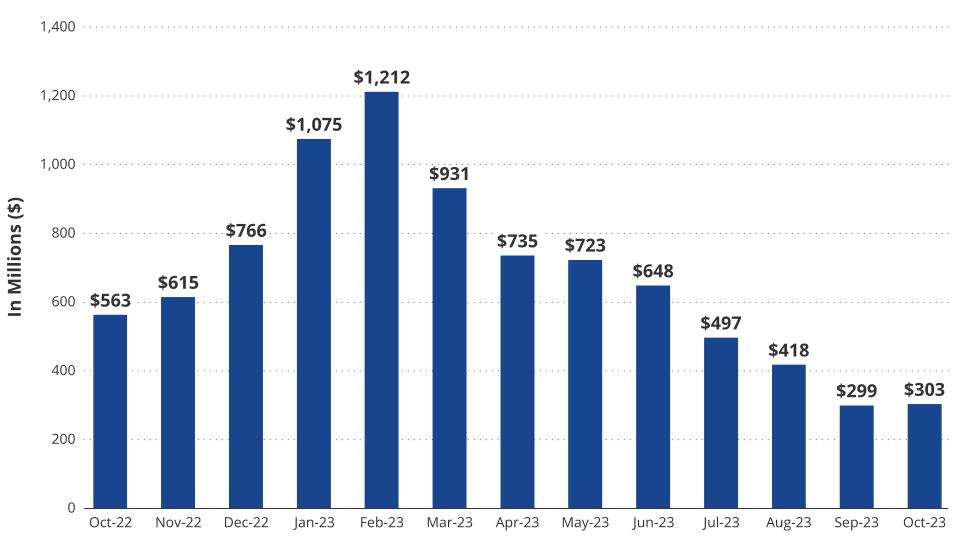

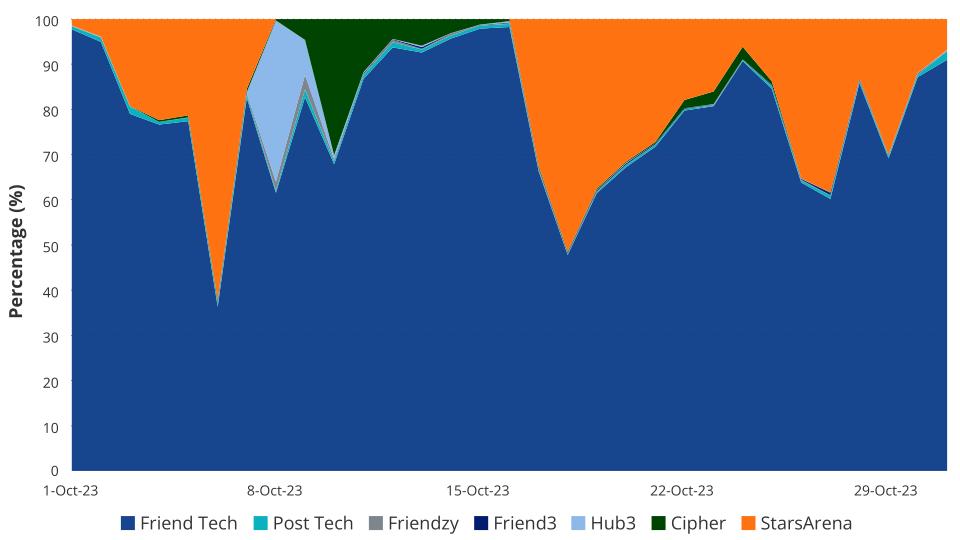

Friend.Tech continued to capture the majority of Social Finance (SoFi) volume this month while competitors suffered from exploits and lack of usership. At the start of the month, StarsArena was exploited for ~$3 million AVAX due to a re-entrancy bug. However, the team was able to recoup the funds from the exploiter (minus a 10% whitehat bounty) and relaunch the platform by mid-month. Upon relaunch, StarsArena was able to gain back some market share from Friend.Tech, but it has consistently receded since and never exceeded its all-time high market share of volume that it achieved on its initial launch.

In previous recaps, we have mentioned how the illiquidity of Friend.Tech keys will lead to substantial price movements as users exit the protocol. This was made evident this month when one of the top accounts on the platform, Vombatus.eth, dumped 176 of their own keys for 851 ETH, or about $1.5 million. This sent the price of Vombatus.eth keys from around 8.3 ETH each to 1.7 ETH, an 80% drawdown. We believe that there is a high possibility that the same heightened volatility that initially attracted users to Friend.Tech could also catalyze their exit as users look to capitalize on the massive appreciation many of the Friend.Tech keys have experienced. As it stands today, Friend.Tech has been able to onboard 832k unique buyers who have traded over $23 million of keys on the protocol. Friend.Tech’s continued dominance in the SoFi market suggests that its ability to capture a large number of users early and promises of a future airdrop have provided a strong enough moat to retain users at least until the airdrop has commenced.

The MarketVector Media and Entertainment Leaders index (MVMELE) finished the month up 14.8%, slightly underperforming Bitcoin but outperforming ETH by a considerable margin as investors speculated on the low market capitalization tokens, which can provide higher upside in a bull market rally. Of the index components, GALA, AXS, and MANA received the most attention, returning 32%, 17%, and 16%, respectively. APE and SAND underperformed the rest of the index, returning only 5.6% and 9% throughout the month. While GALA and MANA had no clear catalysts this month to explain their performance, the AXS rally was likely supported by Game Jam 2023, an event where independent game developers were invited to create and submit games to be included in the Axie Infinity universe. Axie Infinity currently attracts about 300k monthly active players, which is still only a fraction of the ~3 million monthly active users it boasted in the bull market before being hacked. While the outperformance of metaverse and gaming tokens was impressive, keep in mind that GALA, AXS, and MANA are still down from their peaks of 98%, 96%, and 93%, respectively.

Source: DappRadar as of 10/31/2023. Past performance is not indicative of future results. Not intended as a recommendation to buy or sell any of the names mentioned herein.

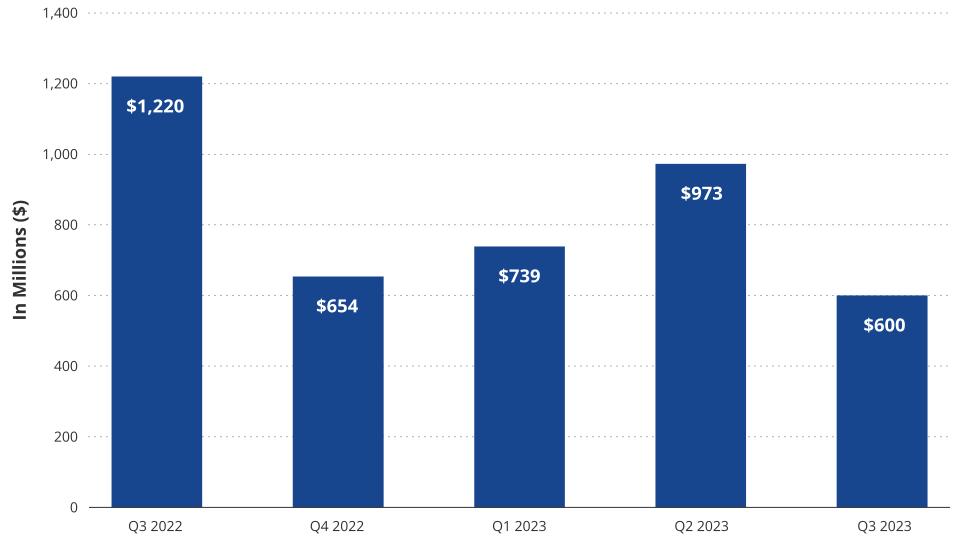

The outperformance of metaverse and gaming tokens indicates that investors still believe in the potential of a blockchain-based metaverse in the future, which is supported by a report from DappRadar indicating that $600m in investment flowed into Web3 gaming in Q3. However, the Web3 gaming space has continued to see lackluster adoption throughout the bear market as multiple AAA games were promised in 2023 but have not yet been released, such as Illuvium and Shrapnel. Additionally, the top metaverse platforms continue to see low monthly usership, with The Sandbox and Decentraland only attracting 12.5k and 3.2k unique users in October. With this in mind, it would appear that the outperformance was likely due to traders speculating ahead of a potential bull market run rather than any real fundamental change in value. Gaming and metaverse tokens have historically been highly speculative, and since the move was not supported by any large fundamental improvements in the tokenomics of these projects, we think it is likely they will underperform during consolidation periods with brief spikes in outperformance until greater adoption is seen and clear winners emerge.

Source: Coingecko as of 10/31/2023. Past performance is not indicative of future results. Not intended as a recommendation to buy or sell any of the names mentioned herein.

Near the end of the month, Circle (the company that issues USDC) announced a partnership with the second-largest convenience store chain in Taiwan, FamilyMart, and the leading cryptocurrency exchange in Taiwan BitoGroup, to provide FamilyMart customers with the ability to exchange loyalty points for USDC. According to the announcement, Taiwan has one of the highest densities of convenience stores, making loyalty points at these shops extremely significant for the daily consumer. By providing the ability to redeem loyalty points for USDC, consumers will be able to avoid the depreciation of loyalty points and use their rewards to purchase a much wider range of goods as they are no longer limited to accessing the value of their points purely through items sold by FamilyMart. Additionally, the partnership should help bolster the circulating supply of USDC, which has been hammered during the bear market and is down 55% from the all-time high. Circle previously announced a partnership with Grab App, a super-app in Southeast Asia with over 130 million users. The latest partnership with FamilyMart highlights Circle’s continued effort to get their stablecoin integrated with more retail-facing applications, as well as the growing adoption of Web3 technology in Asia.

Links to third party websites are provided as a convenience and the inclusion of such links does not imply any endorsement, approval, investigation, verification or monitoring by us of any content or information contained within or accessible from the linked sites. By clicking on the link to a non-VanEck webpage, you acknowledge that you are entering a third-party website subject to its own terms and conditions. VanEck disclaims responsibility for content, legality of access or suitability of the third-party websites.

To receive more Digital Assets insights, subscribe for our Crypto Newsletter

Important Information

This is not financial research but the opinion of the author of the article. We publish this information to inform and educate about recent market developments and technological updates, not to give any recommendation for certain products or projects. The selection of articles should therefore not be understood as financial advice or recommendation for any specific product and/or digital asset. We may occasionally include analysis of past market, network performance expectations and/or on-chain performance. Historical performance is not indicative for future returns.

For informational and advertising purposes only.

This information originates from VanEck (Europe) GmbH, Kreuznacher Straße 30, 60486 Frankfurt am Main. It is intended only to provide general and preliminary information to investors and shall not be construed as investment, legal or tax advice. VanEck (Europe) GmbH and its associated and affiliated companies (together “VanEck”) assume no liability with regards to any investment, divestment or retention decision taken by the investor on the basis of this information. Views and opinions expressed are current as of the date of this information and are subject to change with market conditions. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results. VanEck makes no representation or warranty, express or implied regarding the advisability of investing in securities or digital assets generally or in the product mentioned in this information (the “Product”) or the ability of the underlying Index to track the performance of the relevant digital assets market.

The underlying Index is the exclusive property of MarketVector Indexes GmbH, which has contracted with CryptoCompare Data Limited to maintain and calculate the Index. CryptoCompare Data Limited uses its best efforts to ensure that the Index is calculated correctly. Irrespective of its obligations towards the MarketVector Indexes GmbH, CryptoCompare Data Limited has no obligation to point out errors in the Index to third parties.

Investing is subject to risk, including the possible loss of principal up to the entire invested amount and the extreme volatility that ETNs experience. You must read the prospectus and KID before investing, in order to fully understand the potential risks and rewards associated with the decision to invest in the Product. The approved Prospectus is available at www.vaneck.com . Please note that the approval of the prospectus should not be understood as an endorsement of the Products offered or admitted to trading on a regulated market.

Performance quoted represents past performance, which is no guarantee of future results and which may be lower or higher than current performance.

Current performance may be lower or higher than average annual returns shown. Performance shows 12 month performance to the most recent Quarter end for each of the last 5yrs where available. E.g. '1st year' shows the most recent of these 12-month periods and '2nd year' shows the previous 12 month period and so on. Performance data is displayed in Base Currency terms, with net income reinvested, net of fees. Brokerage or transaction fees will apply. Investment return and the principal value of an investment will fluctuate. Notes may be worth more or less than their original cost when redeemed.

Index returns are not ETN returns and do not reflect any management fees or brokerage expenses. An index’s performance is not illustrative of the ETN’s performance. Investors cannot invest directly in the Index. Indices are not securities in which investments can be made.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of VanEck.

© VanEck (Europe) GmbH

This is a marketing communication. Please refer to the prospectus of the UCITS and to the KID before making any final investment decisions.

This information originates from VanEck (Europe) GmbH, which has been appointed as distributor of VanEck products in Europe by the Management Company VanEck Asset Management B.V., incorporated under Dutch law and registered with the Dutch Authority for the Financial Markets (AFM). VanEck (Europe) GmbH with registered address at Kreuznacher Str. 30, 60486 Frankfurt, Germany, is a financial services provider regulated by the Federal Financial Supervisory Authority in Germany (BaFin).

The information is intended only to provide general and preliminary information to investors and shall not be construed as investment, legal or tax advice VanEck (Europe) GmbH, VanEck Switzerland AG, VanEck Securities UK Limited and their associated and affiliated companies (together “VanEck”) assume no liability with regards to any investment, divestment or retention decision taken by the investor on the basis of this information. The views and opinions expressed are those of the author(s) but not necessarily those of VanEck. Opinions are current as of the publication date and are subject to change with market conditions. Certain statements contained herein may constitute projections, forecasts and other forward-looking statements, which do not reflect actual results. Information provided by third party sources is believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Brokerage or transaction fees may apply.

All performance information is based on historical data and does not predict future returns. Investing is subject to risk, including the possible loss of principal.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of VanEck.

© VanEck (Europe) GmbH / VanEck Asset Management B.V.

09 March 2026

09 March 2026