Welcome to VanEck

Select Investor Type

13 November 2020

If biblical metaphors are your thing, you could compare the Covid-19 crisis to Egypt’s seven years of famine in the book of Genesis. Although a lesser crisis, just like then the pandemic follows years of plenty. The good years have been marked by exceptionally buoyant financial markets – a trend that came to a volatile end as the pandemic’s full force became clear.

For many people, the place they will feel the financial consequences of Covid-19 is their pension. Even now, the pandemic’s second wave is sinking Europe’s hopes of a V-shaped economic recovery, triggering a renewed slide in stock markets.

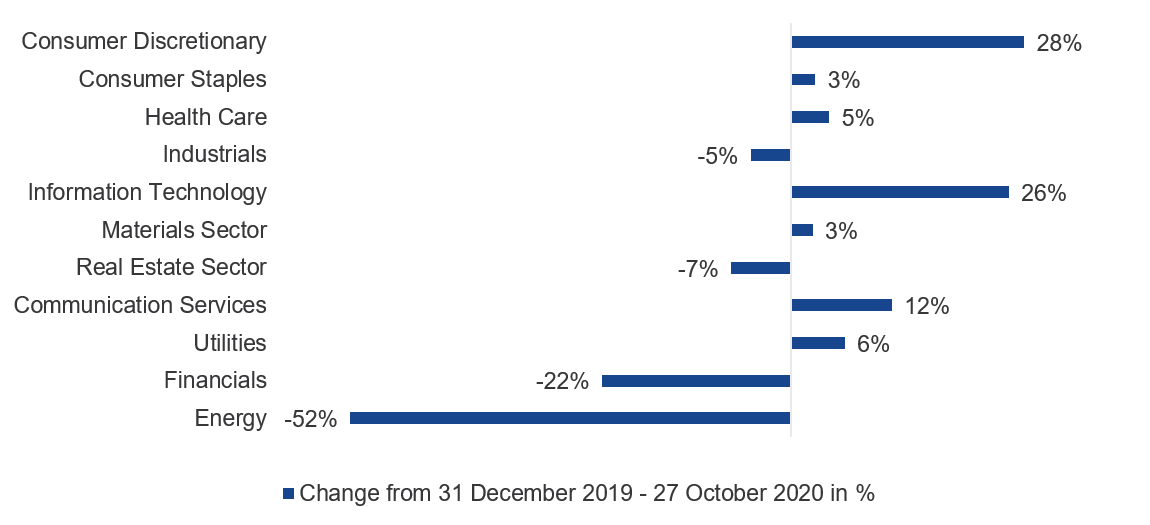

So, how safe are your retirement savings? One lesson of the pandemic is that you need to rely more on yourself and spread your risks. As social distancing has pushed people to work from home, so many have become more detached from their employers. And the performance of stocks has polarized. While technology and healthcare stocks have rocketed higher, some supposedly ‘safe’ stocks in sectors like oil, banks or airlines have fallen.

The lesson is clear. In times like these, your retirement savings are not as secure. You are better off taking control of your financial destiny and falling back on the golden rules of investing. Most importantly, these rules are: diversify your risk through portfolios invested across sectors and watch the cost of investing as high fees can add up to a lot over time.

Source: McKinsey. Past performance is not a reliable indicator of future performance.

When Covid-19 initially spread in March, the hit to stock markets and savings was immediate and brutal. The massive rally that followed, however, alleviated this to a degree.

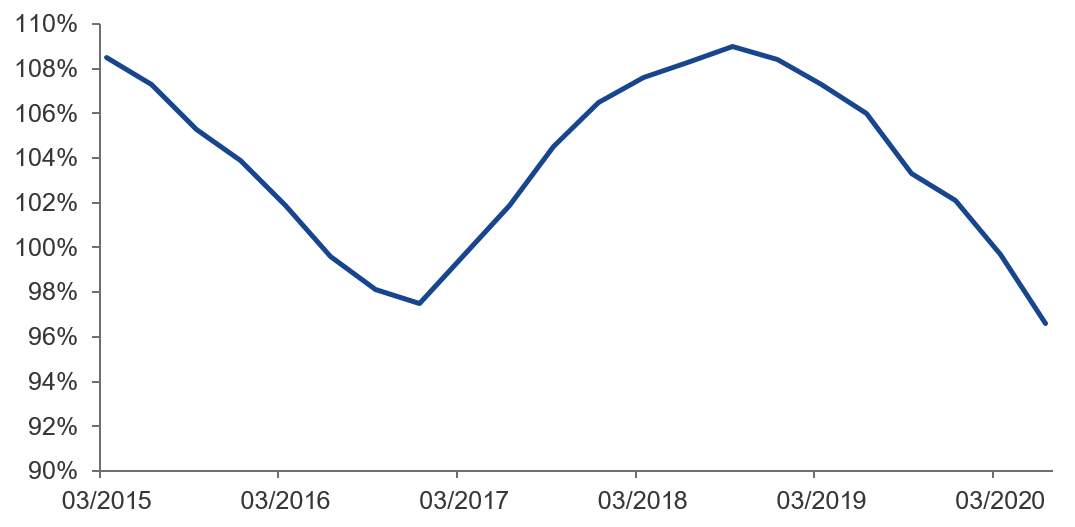

But to make things worse, savers around the world have raided pension schemes ahead of retirement to alleviate their immediate money worries. Furthermore, as interest rates fell still further, so the liabilities of corporate so-called defined benefit schemes rose. The result? Their funding ratios – which show to what extent investments cover future liabilities – dropped significantly. In the Netherlands, for instance, the ratio fell from 104% at the end of 2019 to 90% at 31 March 2020.

Funding ratio of Dutch pension funds

Source: Dutch Central Bank. Data for the period June 2015 – June 2020.

Turning to the state pension, in countries such as Italy and Germany, where the state pays a substantial proportion of pensions, problems are also mounting. As former French president François Hollande said recently in Le Figaro: “Today’s borrowings are tomorrow’s taxes.1”. In other words, your state pension may not be as generous as you think, once there is a reckoning for the huge borrowings currently being amassed by governments.

What all of this underlines is the importance of taking control of your financial destiny. The ability of your employer or the state to pay you a handsome pension on retirement has been weakening for some time, especially as defined contribution pensions have progressively taken over from old-fashioned defined benefit.

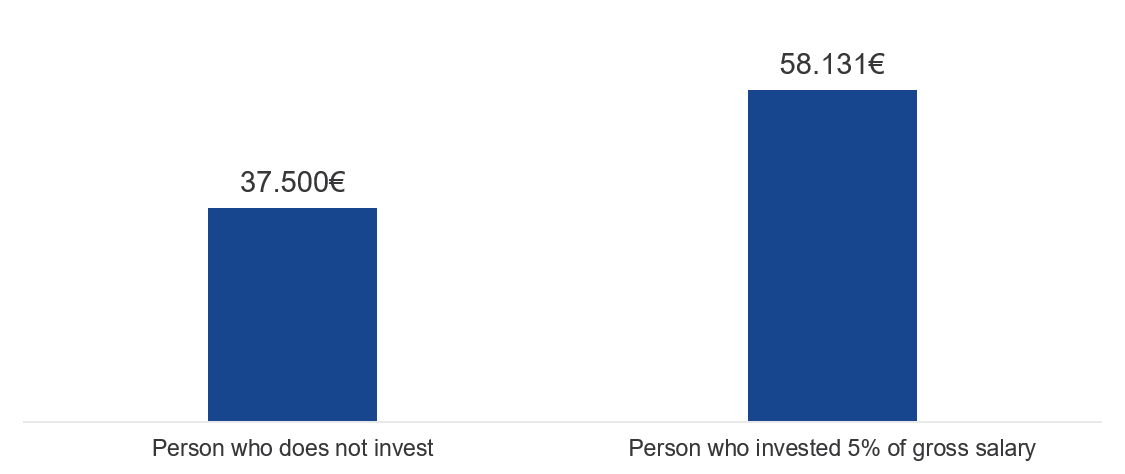

Take the trouble to understand you pension options and likely income on retirement. You will see that it pays off to build up an additional pension pot. An extra 5% of your monthly gross salary squirreled away could almost double your total pension (see graph below). Of course, ETFs are made for pensions. They are the perfect vehicles for accessing stock and bond markets in a diversified way with low costs – typically annual costs total below 0.5% of assets invested.

ETFs are accessible nowadays through pensions platform, such as the UK’s self-invested personal pension (known as a SIPP), online life insurance companies and sometimes even online brokers.

Expected annual pension at retirement

Source: VanEck. Assuming a person who gains 50,000€ annually throughout his life and receives a pension of 75% of final earnings. Annual return on pension investments are supposed to be 6% which can be converted into an annuity of 5% of the final savings amount.

Many countries provide valuable tax incentives for voluntary pension savings. Typically, your contributions are exempt from income tax, as are the gains on your capital over time. The impact can be material. If your marginal tax bracket is 50%, for any euro, pound or franc paid in your life insurance policy, you would pay 50 cents, pence or pfennig less taxes. And, assuming a 1% annual capital tax, the impact over a, say, 40-year period is sizeable! During retirement, typically, you pay taxes on the payments received from your pension. However, by then your marginal tax bracket may well be lower, as pensions typically are lower than salaries.

In many ways, it seems that Covid-19’s shock will leave a lasting impression, although perhaps not a truly biblical one. People seem more likely to spend time working from home in future, and all of us are are getting to grips with technology. Could it also be that people will seize control of their retirement savings?

1Source: Le Figaro.

This is a marketing communication. Please refer to the prospectus of the UCITS and to the KID before making any final investment decisions.

This information originates from VanEck (Europe) GmbH, which has been appointed as distributor of VanEck products in Europe by the Management Company VanEck Asset Management B.V., incorporated under Dutch law and registered with the Dutch Authority for the Financial Markets (AFM). VanEck (Europe) GmbH with registered address at Kreuznacher Str. 30, 60486 Frankfurt, Germany, is a financial services provider regulated by the Federal Financial Supervisory Authority in Germany (BaFin).

The information is intended only to provide general and preliminary information to investors and shall not be construed as investment, legal or tax advice VanEck (Europe) GmbH, VanEck Switzerland AG, VanEck Securities UK Limited and their associated and affiliated companies (together “VanEck”) assume no liability with regards to any investment, divestment or retention decision taken by the investor on the basis of this information. The views and opinions expressed are those of the author(s) but not necessarily those of VanEck. Opinions are current as of the publication date and are subject to change with market conditions. Certain statements contained herein may constitute projections, forecasts and other forward-looking statements, which do not reflect actual results. Information provided by third party sources is believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Brokerage or transaction fees may apply.

All performance information is based on historical data and does not predict future returns. Investing is subject to risk, including the possible loss of principal.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of VanEck.

© VanEck (Europe) GmbH / VanEck Asset Management B.V.

18 May 2026

18 May 2026