Welcome to VanEck

Select Investor Type

20 July 2023

In light of Ethereum’s recent hard fork, which allows users to withdraw staked ETH and, in our view, creates a major new competitor to US T-bills, we revisited our Ethereum estimates with a more rigorous valuation model.

We now see ETH network revenues may be rising from an annual rate of $2.6B to $51B in 2030. This analysis offers a potential valuation methodology for Ethereum, considering transaction fees, MEV, and "Security as a Service.” We assess market capture across key sectors and explore Ethereum's potential as a store-of-value asset in the evolving crypto landscape.

We may potentially value Ethereum by estimating cash flows for the year that ended on 4/30/2030. We project Ethereum revenues, deduct a global tax rate and a validator revenue cut and arrive at a cashflow figure. We then apply multiple estimates by applying a long-term estimated cash flow yield of 7% minus the long-term crypto growth rate of 4%. We then arrive at the fully diluted valuation (“FDV”) in 2030, divide the total by the expected number of tokens in circulation, and then discount the result by 12% to 4/20/2023. You can see our revenue estimates in the table below with more detailed assumptions in the Ethereum Valuation Scenarios table. Please note that these assumptions and estimations should not be understood as facts.

| Ethereum Revenue | ||||

| Today | Base 2030 | Bear 2030 | Bull 2030 | |

| Ethereum Total Revenue | $2,539 | $50,985 | $2,564 | $136,771 |

| Transactions | $1,991 | $29,337 | $1,271 | $83,839 |

| Finance, Banking, Payments | $929 | $10,370 | $444 | $26,666 |

| Metaverse, Social and Gaming | $834 | $13,068 | $700 | $42,004 |

| Infrastructure | $228 | $5,899 | $126 | $15,170 |

| MEV - Block Builder Revenue | $497 | $19,665 | $1,175 | $48,078 |

| Ethereum Security as a Service | $0 | $1,983 | $118 | $4,854 |

Source: VanEck Research as of 4/30/2023. Past performance is no guarantee of future results. The above is not intended as financial advice, a recommendation to buy or sell Ethereum, or any call to action. There may be risks or other factors not accounted for in the above scenarios that may impede the performance of Ethereum; the actual future performance of Ethereum is unknown, and may differ significantly. Any projections, forecasts or forward-looking statements included herein are the results of a simulation based on our research, are valid as of the date of this communication and subject to change without notice, and are for illustrative purposes only. Please conduct your own research and draw your own conclusions.

To properly unpack our valuation approach to Ethereum, it is important first to understand what Ethereum is, how it works, and why it is valuable. At the most basic level, one can think of Ethereum as a mall that lives on the internet and provides a secure place for internet commerce to take place. Users interact inside Ethereum’s mall by means of wallets, and Ethereum’s mall businesses are made up of batches of smart contract code. The Ethereum software determines the structure and rules of the mall, while validators ensure that the rules are followed, secure the mall, and maintain a ledger of all economic events that occur within the mall. Ethereum also apportions the limited space within the mall by charging users for conducting business and exchanging value.

Ethereum is free software that is hosted on computers distributed throughout the globe. It employs an array of logic, called a protocol, to create a unified understanding of ownership, commercial activity, and business logic. This allows users to engage in commerce without the need to trust any of its participants or counterparties. Ethereum code creates verifiable and unambiguous rules that assign clear, strong property rights to create a platform for unrestrained business formation and free exchange.

The computers that run Ethereum software, called validators, receive inflationary rewards and a portion of the fees remitted by users performing activity on Ethereum. Businesses are created on Ethereum by deploying a series of smart contracts. Smart contracts are computer code libraries that autonomously execute functions when called upon by users without any intermediary. Using smart contracts, developers can build logic that replicates the function of businesses like banks, auction houses, social media companies, video games platforms, cloud computing services, and commodities exchanges. Using Ethereum, a business can keep its treasury entirely on Ethereum and enable smart contract disbursements to employees, vendors, contractors, and suppliers who can also have wallets on Ethereum.

For users to perform on-chain actions to exchange value or interact with on-chain businesses, they incur fees paid to Ethereum. These fees are relative to the computational intensity and spot demand for computation on the Ethereum network. Curiously, unlike most enterprises where businesses pay the overhead of rent, electricity, and the rest, users directly pay the overhead costs of interacting with the on-chain business to that on-chain business’s host and chief vendor - Ethereum. Thus, users pay both the costs of hosting the business and the costs of Ethereum computation, on behalf of on-chain businesses, through their transactions.

The principal medium of exchange on the Ethereum network is the ETH token. For users to conduct activity on Ethereum, they must pay for the cost of performing their actions in ETH, just like at Dave & Busters, where one must buy “gaming points” to play video games. To do anything on Ethereum, a user of Ethereum must utilize ETH tokens. Additionally, validators must post value, in the form of ETH, as collateral against their honesty. If a validator cheats, the ETH is seized. Considering that ETH tokens are the currency used to pay validators (who are selling ETH to cover costs), this marries demand with supply – Ethereum users buy tokens to use Ethereum, and Ethereum validators sell tokens to “supply” Ethereum.

What does it mean to “supply” Ethereum? In essence, it means participating in the consensus mechanism of Ethereum that verifies value transfers, allows for the deployment of smart contract code, or enables calls to Ethereum’s software. All business logic and exchange of assets occur as ledger entries on blocks. Blocks are simply the “to-do list” for the Ethereum computer to complete, and every twelve seconds, the table of actions is executed. The list directs Ethereum to perform an action or a series of actions on behalf of the users. These directions could be as simple as sending value or as complex as buying and selling dozens of tokens simultaneously across dozens of different Ethereum-based token exchanges. Users gain inclusion on the block for their actions by paying a base fee and an inclusion fee. If there is a lot of demand for Ethereum’s “to-do list,” users can increase their inclusion fee, called a “tip,” to ensure their request is fulfilled. Additionally, Ethereum has created a marketplace to auction off the right to order (and add transactions to) the action list on each of Ethereum’s blocks. This is done because there is immense value in ordering the transactions. These two activities currently represent Ethereum’s core business – selling blockspace and selling the right of others to order it. Distilled, Ethereum is selling secure, immutable blockspace that facilitates internet commerce.

Because Ethereum is not really a business, we identify revenue as an activity where tokens are used in Ethereum’s core business – the provision of immutable, decentralized computing through the sale of blockspace. As a result, we count transaction fees, both the base fee and the tip fee, as a revenue line. Other analysts only count the base fee because it is burned, which impacts all ETH holders, while omitting the tip because it only is remitted to each leadership slot validator. In their construct, only staked ETH on validators receives the tip fee. However, we count both tip and base fees in addition to base fees as each reflects economic activity on Ethereum related to the sale of blockspace. Therefore, the economic value of those actions flows through to Ethereum as a business.

Additionally, we subtract ETH burned from the base fee from the ETH total supply and derive token value from the end-year, reduced supply total. Admittedly, unlike other components of our analysis, the yearly trajectory of ETH usage significantly influences today’s token valuation through total token supply reduction. Additionally, we do not count inflationary security issuance as a revenue item as it does not relate directly to an outside entity buying blockspace.

Not only do we recognize the transaction fees of the system, but we also recognize MEV as a revenue item to ETH. With entities like Flashbots auctioning off blockspace to builders, a portion of the MEV will accrue to ETH stakers, passed on by validators. Similar to tip fees given to validators, we also believe block-building fees should be included in Ethereum’s revenue calculations as they are economic activity related to the sale of blockspace.

Finally, we assert that ETH may be evolving beyond a transactional currency or a consumable commodity like oil or natural gas. We believe that ETH, while not a complete store of value like Bitcoin due to Ethereum’s demonstrated mutability of code and an evolving social consensus focused on utility, will may become a store-of-value asset for state actors looking to maximize human capital (vs. Bitcoin, which maximizes for stranded energy). Importantly, in this model update, due to smart contract programmability on Ethereum combined with maturing cross-chain messaging technology, we introduce a novel revenue item called “Security as a Service” (SaaS).

Conceptually, ETH’s value can be used both within Ethereum and outside of it to secure applications, protocols, and ecosystems. Using projects such as Eigenlayer, ETH can be used to back entities such as Oracles, Sequencers, Validators, bridges, contractual agreements, and perhaps novel entities yet to be discovered. The result is that ETH approximates a Layer 0 asset like Bitcoin or Polkadot’s DOT and Cosmos’s ATOM claim. These Layer 0 assets can be used to back and bootstrap new blockchains. Since ETH may be a bearer asset, ETH can be locked behind some business or protocol’s guarantees to act honestly. If that honesty is violated, that value can be seized to penalize malicious or irresponsible parties and/or compensate affected parties. This can be thought of as a performance bond or collateral that ensures a damaged party recovers losses while a lousy actor pays for its malice.

Stepping back, this business type relies upon the value of ETH as a token and the safety and persistence of Ethereum’s software. Thus, as Ethereum’s security can be exported, ETH holders who participate in SaaS should be rewarded at some multiple to the summed value of priority fees, tips, block-building fees, and ETH inflationary issuance – the ETH holder’s opportunity cost multiplied by risk. This multiple reflects the average security risks and investment risks involved in offboarding ETH as a security provision asset.

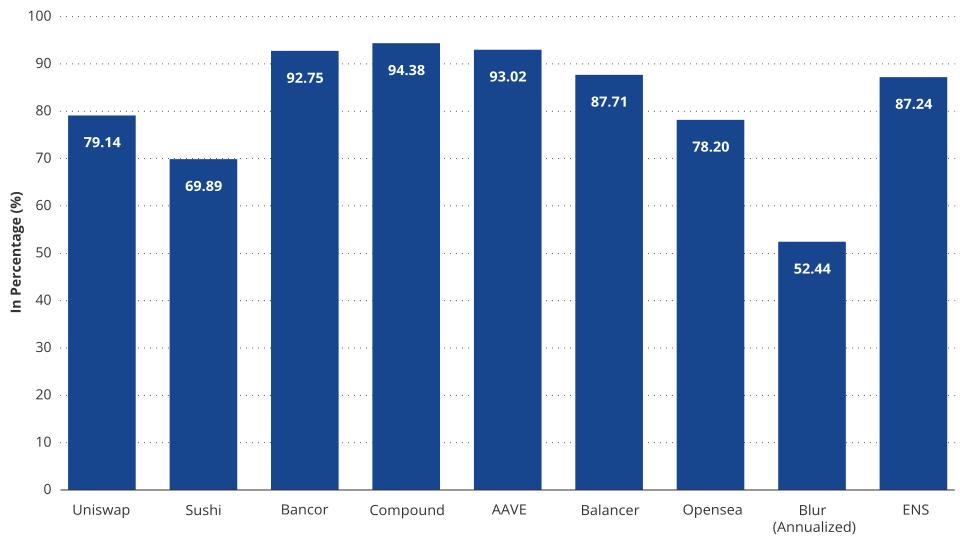

Source: VanEck, Token Terminal as of 4/30/2023. Past performance is no guarantee of future results. Not intended as a recommendation to buy or sell any securities named herein.

The base of our calculations comes from the smart contract platform “market capture.” This is the percentage of each business category’s economic activity that we believe will utilize, be derived from, or reside on public smart contract platforms like Ethereum. Our main categories are Finance, Banking, and Payments (FBP), Metaverse, Social and Gaming (MSG), and Infrastructure (I). FBP encompasses financial activity, including consumer and business payments, banking services, and exchanges of value. MSG includes software and internet businesses that revolve around online social media, gathering, gaming, and virtual/online world value creation. Infrastructure encompasses the provision of cloud computing, server space, and distributed storage, as well as telecommunication and the internet. We assume that 5%, 20%, and 10% of finance, metaverse/media, and tech infrastructure activity, respectively, move on-chain. (Our relatively high estimates for metaverse/media contemplate the recent acceleration in information censorship in countries like Brazil, India & Ireland and the high number of open-source social networks currently under development). Please note that these assumption may differ significantly from reality and should not be understood as facts.

Since the precise value accrual from a business deployed to a blockchain is uncertain, we assume a take rate on the business economic activity derived from blockchain deployment. This is not without precedent, as many blockchain-native businesses are currently deployed to smart contract platforms. The businesses themselves do not directly pay fees to Ethereum for the usage of their businesses. The users do. However, over the long run, to simplify the user experience, businesses deployed to blockchain will likely pay fees on behalf of their customers. For example, a coffee roaster whose website is hosted on AWS does not make a customer pay for both the coffee purchase and the roaster’s website costs at check out. Instead, the coffee store abstracts those costs and makes the customer only directly pay for the purchase items. In the future, blockchain-reliant and blockchain-based businesses will likely gravitate towards similar dynamics.

Looking at the cost breakdown to the user for using a blockchain business can inform our estimates of blockchain value capture over the long run. Right now, a user who wants to secure a loan using AAVE on Ethereum will pay both fees to AAVE and Ethereum for this business transaction. Of course, on the flip side, these fees to a user represent revenues to AAVE and Ethereum. If such a transaction occurred in real life, it would look like someone going to a Sharper Image at the mall and paying for his “laser pointer blowtorch back-scratcher” in addition to a portion of the Sharper Images’ monthly rent at checkout. We can see the breakdown of this ratio by examining the gas costs users pay to interact with an on-chain business’s smart contracts (Ethereum’s revenue) versus the costs the user pays directly to the business (AAVE’s revenues) from the same transaction. These ratios vary greatly depending on the type of on-chain business.

Source: VanEck, Token Terminal as of 4/30/2023. Past performance is no guarantee of future results. Not intended as a recommendation to buy or sell any securities named herein.

We can infer from the above chart that over the past year, the average cost split between platform and business for a user of AAVE is shared 6.98% to the platform (Ethereum) and 93.02% to AAVE (application and its lenders). Drawing back to focus on value accrual to smart contract platforms like Ethereum, we feel this relationship will shift over time as off-chain businesses deploy on-chain to reduce costs and seek new revenue. In our model, we assume application take rates will vary between 90% to 97% of revenue depending on the end market, with ETH share falling between 3% and 10% depending on the business category. Please note that these assumptions should not be understood as facts and reality may differ significantly from these assumptions.

We think approximating this take rate is essential because “transactions revenue” is not an ideal mechanism to describe future blockchain value capture. Going by our earlier assertion that the transactions are a “to-do list” of items for Ethereum to compute, many uses of the blockchain cannot be best described as “transactions.” Blockspace is the more fitting unit of measurement and description of the product sold by smart contract blockchains like Ethereum. It is possible that smart contract blockchains package blockspace into a “service level agreement” to other parties to guarantee some present or future amount of compute or transaction activity. This activity will create complex, liquid blockspace futures markets that mirror commodities futures dynamics. However, we will stick with “Transaction Revenue” to keep in line with current conventions.

To deduce future ETH supply reductions from ETH base fee burns that occur from blockspace usage, we begin by applying past Ethereum burn/fee ratios. We employ a figure of 80% for the percent of burned transaction fees. In ETH terms, we then estimate a transaction cost average for both Ethereum and Layer 2 platforms with a very significant cost decline rate of roughly 60%. We speculate that the cost differential for L2s will be 1/100th that of Ethereum. After that, we calculate future MAUs on Ethereum as a function of end-market business MAUs and Ethereum’s capture of those MAUs. Ethereum capture rate of those MAUs is determined by Ethereum’s take rate of those underlying business categories’ economic activity (between 5% and 20%, depending on the end market). We do not project transactions and then extrapolate a revenue assumption from them. We simply assume a declining transaction cost in ETH and project a yearly burn amount from the base fee burn. Again, this burn amount is subtracted from the total running supply of Ethereum and significantly impacts token value as Ethereum’s FDV is spread across fewer tokens. Please note that we make significant assumptions and facts may differ from our predictions and assumptions.

MEV is considered a “bogeyman” of blockchain that many entities seek to stop, distribute and/or suppress MEV. MEV is simply the profits that can be made by ordering transactions within each produced block. In reality, MEV can be limited but cannot be destroyed. We see MEV playing an integral role in securing (paying the validators and stakers) blockchains over the long run because of MEV’s immense value. A corollary of its certain persistence is shelf space at a supermarket. There will always be more valuable shelf space (that at “eye level”), and someone will be willing to pay to occupy that space at the expense of others. Likewise, there will always be value in ordering transactions, and there is immense value to be gained by monetizing that ordering.

Because MEV is highly correlated with on-chain activity, it is difficult to predict. For our estimate, we assume that MEV is directly related to the value of all assets hosted on Ethereum. This gives us a “management fee” for keeping value on Ethereum. Currently, we estimate yearly MEV value approximates ~2.0% of on-chain TVL on Ethereum (not the value of all assets on chain) for the past year. Long term, we assume that MEV as a percentage of assets will shrink as protocols and applications act to reduce its impact, the turnover rate of on-chain assets declines, and applications remit some of its value back to users. Therefore, we see the MEV take rate dwindling to 0.15%. We assume the total value of on-chain assets relates to the total value of all hosted assets on the blockchain, and this value is derived from the share of the FBP that blockchains retain and Ethereum’s market share. Please note that the above mentioned assumptions and estimations should are not based on facts and reality may be very different.

As L2 settlement represents the long-term scaling solution for executing transactions on Ethereum, it's assumed to be the most important business line for Ethereum going forward. L2 settlement represents the line item of the transaction batches being posted to Ethereum. We predict settlement revenue as a function of L2 revenue and the margin relationship between “profits” and the cost of security to send batches to Ethereum. In our projections, we assume L2 revenue to be simply composed of MEV and transaction revenues which are both estimated by using the Ethereum framework. We then assume that L2s pay a portion of those revenues as security fees to Ethereum. We have seen the L2 “margins” fluctuate between 15% - 40% depending upon gas costs of Ethereum, although it should be noted that ths figure could be very different in reality. Over the long run, we assert that most revenue from the L2 may still accrue to Ethereum, including MEV on the L2. We assume this to be the case because we project there may be thousands of L2s competing for blockspace on Ethereum and margins. We assert a long-term margin rate of 10% for the L2s versus the current range of 15% - 40%. This estimate is admittedly arbitrary, but we expect that as thousands of competing chains may emerge to compete for Ethereum blockspace, margins for L2s will shrink dramatically. In terms of the value split, we assume that 98% of all transactions are executed on the L2s while 50% of the total value of assets rest on L2s. We assert that Ethereum will still host half of the ecosystem's value because some assets and transactions may necessitate extreme security, composability, and atomicity levels. Please note that any of the above-mentioned assumptions, predictions and projections should not be understood as facts and may differ greatly from reality.

We define Ethereum’s SaaS business as the revenues received from exporting ETH token value to back outside ecosystems, applications, and protocols. This is a burgeoning and uncertain use case for ETH that is hard to predict. To speculate on what percentage of ETH will be exported to gain fees for security provision, we look to current and past examples of bridged assets. Currently, the total percentage of ETH that is bridged off Ethereum is 0.47%, while the total supply of ATOM off-chain is around 0.5%. In the past, BTC wrapped and exported to other chains was as high as 1.7%, and during the peak of bridging activity on Ethereum, more than 15% of Ethereum’s USDC supply was bridged off the chain. As a starting point, we assume that 10% of ETH is used to provide security off-chain and that for a risk premium, it should command a 2x premium to ETH on-chain. Please note that any of the above-mentioned assumptions, predictions and projections should not be understood as facts and may differ greatly from reality.

The full analysis is available (also as PDF) for website visitors from the US.

Important Information

We publish this newsletter to inform and educate about recent market developments and technological updates, not to give any recommendation for certain products or projects. The selection of articles should therefore not be understood as financial advice or recommendation for any specific product and/or digital asset. We may occasionally include analysis of past market, network performance expectations and/or on-chain performance. Historical performance is not indicative for future returns.

ETN Disclaimer

Important information

For informational and advertising purposes only.

This information originates from VanEck (Europe) GmbH, Kreuznacher Straße 30, 60486 Frankfurt am Main. It is intended only to provide general and preliminary information to investors and shall not be construed as investment, legal or tax advice. VanEck (Europe) GmbH and its associated and affiliated companies (together “VanEck”) assume no liability with regards to any investment, divestment or retention decision taken by the investor on the basis of this information. Views and opinions expressed are current as of the date of this information and are subject to change with market conditions. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results. VanEck makes no representation or warranty, express or implied regarding the advisability of investing in securities or digital assets generally or in the product mentioned in this information (the “Product”) or the ability of the underlying Index to track the performance of the relevant digital assets market.

The underlying Index is the exclusive property of MarketVector Indexes GmbH, which has contracted with CryptoCompare Data Limited to maintain and calculate the Index. CryptoCompare Data Limited uses its best efforts to ensure that the Index is calculated correctly. Irrespective of its obligations towards the MarketVector Indexes GmbH, CryptoCompare Data Limited has no obligation to point out errors in the Index to third parties.

Investing is subject to risk, including the possible loss of principal up to the entire invested amount and the extreme volatility that ETNs experience. You must read the prospectus and KID before investing, in order to fully understand the potential risks and rewards associated with the decision to invest in the Product. The approved Prospectus is available at www.vaneck.com . Please note that the approval of the prospectus should not be understood as an endorsement of the Products offered or admitted to trading on a regulated market.

Performance quoted represents past performance, which is no guarantee of future results and which may be lower or higher than current performance.

Current performance may be lower or higher than average annual returns shown. Performance shows 12 month performance to the most recent Quarter end for each of the last 5yrs where available. E.g. '1st year' shows the most recent of these 12-month periods and '2nd year' shows the previous 12 month period and so on. Performance data is displayed in Base Currency terms, with net income reinvested, net of fees. Brokerage or transaction fees will apply. Investment return and the principal value of an investment will fluctuate. Notes may be worth more or less than their original cost when redeemed.

Index returns are not ETN returns and do not reflect any management fees or brokerage expenses. An index’s performance is not illustrative of the ETN’s performance. Investors cannot invest directly in the Index. Indices are not securities in which investments can be made.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of VanEck.

© VanEck (Europe) GmbH

This is a marketing communication for professional investors only. Please refer to the UCITS prospectus and to the Key Investor Information Document (KIID) before making any final investment decisions.

This is a marketing communication for professional investors only. Please refer to the UCITS prospectus and to the Key Investor Information Document (KIID) before making any final investment decisions. This information originates from VanEck Securities UK Limited (FRN: 1002854), an Appointed Representative of Strata Global Limited (FRN: 563834) which is authorised and regulated by the Financial Conduct Authority in the UK. The information is intended only to provide general and preliminary information to FCA regulated firms such as Independent Financial Advisors (IFAs) and Wealth Managers. Retail clients should not rely on any of the information provided and should seek assistance from an IFA for all investment guidance and advice. VanEck Securities UK Limited and its associated and affiliated companies (together “VanEck”) assume no liability with regards to any investment, divestment or retention decision taken by the investor on the basis of this information. The views and opinions expressed are those of the author(s) but not necessarily those of VanEck. Opinions are current as of the publication date and are subject to change with market conditions. Certain statements contained herein may constitute projections, forecasts and other forward-looking statements, which do not reflect actual results. Information provided by third party sources is believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Brokerage or transaction fees may apply.

All performance information is based on historical data and does not predict future returns. Investing is subject to risk, including the possible loss of principal.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of VanEck.

© VanEck Securities UK Limited

09 March 2026

09 March 2026