Opportunity in Elevated EM High Yield Corporate Bond Spreads?

May 29, 2020

Read Time 2 MIN

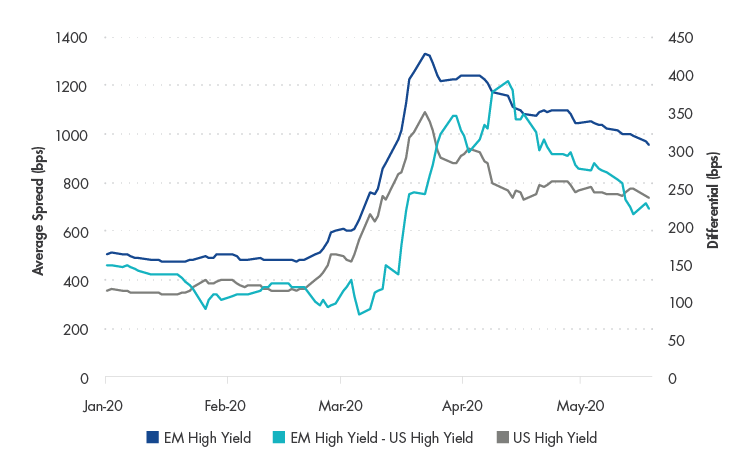

Emerging markets corporate high yield bond spreads continue to stand out following the selloff experienced in March and April. While U.S. high yield bond spreads remain elevated, they are tighter compared to the widest levels reached in late March. In addition to the magnitude of the spreads, which continue to hover around 1,000 basis points, the yield pickup versus U.S. high yield corporate bonds remains historically wide. Since 2004 this differential has averaged 108 basis points, but was 224 basis points as of May 19, 2020, nearly two standard deviations away from this long-term average.

Emerging Markets High Yield Corporate Bond Spreads Remain Elevated

Source: ICE Data Indices as of 5/19/2020. EM High Yield is represented by ICE BofA Diversified High Yield US Emerging Markets Corporate Plus Index, U.S. High Yield is represented by ICE BofA US High Yield Index

Several sectors expected by many to be most impacted by negative global growth are exhibiting distress, including Energy, Basic Industry (particularly Metals & Mining), Retail and Transportation. However, we believe emerging markets energy issuers have held up better than U.S. issuers overall due to the greater presence of quasi-sovereigns. Elevated spreads, however, are not confined to these most impacted sectors, and as shown below, these sectors do not have significantly greater weights within emerging markets compared to the U.S. market, indicating a general re-pricing of risk within emerging markets rather than sector-led weakness.

| Weight (%) | ||

| EM High Yield | U.S. High Yield | |

| Automotive | 0.37 | 5.15 |

| Basic Industry | 13.59 | 9.65 |

| Energy | 13.17 | 12.38 |

| Leisure | 2.53 | 4.81 |

| Retail | 0.71 | 4.45 |

| Transportation | 3.62 | 1.09 |

Source: ICE Data Indices as of 5/19/2020. EM High Yield is represented by ICE BofA Diversified High Yield US Emerging Markets Corporate Plus Index, U.S. High Yield is represented by ICE BofA US High Yield Index

Are these levels attractive? Clearly the market is pricing in a substantial amount of risk at these levels, including a significantly higher probability of defaults. Whether these spreads are adequate compensation will depend on the ultimate impact of the pandemic and the speed at which global growth will recover.

It is worth noting that emerging markets corporates went into this downturn with what we believe are relatively stronger fundamentals compared to U.S. counterparts, including lower levels of leverage and higher coverage ratios to service debt. Further, we expect to see more “fallen angels”—which are high yield bonds that were originally issued with investment grade ratings but subsequently downgraded—emerge. For example, Pemex1, with over $40 billion of index-eligible debt, entered the emerging markets high yield benchmark at the maximum weight of 3% at the end of April (but did not enter U.S. high yield benchmarks due to index eligibility rules). With both corporate and sovereign downgrades likely, we anticipate that more fallen angels will follow. Given the historical propensity of these bonds to sell-off prior to downgrade, enter the index at deep discounts and subsequently recover in value, these fallen angels may provide some tailwinds to the asset class.

DISCLOSURES

13.5% of fund net assets as of May 26, 2020. For a complete list of holdings in the ETF, please click here: https://www.vaneck.com/etf/income/hyem/overview/

Please note that Van Eck Associates Corporation serves as investment advisor to investment products that invest in the asset class(es) included herein.

This content is published in the United States for residents of specified countries. Investors are subject to securities and tax regulations within their applicable jurisdictions that are not addressed in this content. Nothing in this content should be considered a solicitation to buy or an offer to sell shares of any investment in any jurisdiction where the offer or solicitation would be unlawful under the securities laws of such jurisdiction, nor is it intended as investment, tax, financial, or legal advice. Investors should seek such professional advice for their particular situation and jurisdiction.

Emerging Market securities are subject to greater risks than U.S. domestic investments. These additional risks may include exchange rate fluctuations and exchange controls; less publicly available information; more volatile or less liquid securities markets; and the possibility of arbitrary action by foreign governments, or political, economic or social instability. High yield bonds may be subject to greater risk of loss of income and principal and are likely to be more sensitive to adverse economic changes than higher rated securities.

The information herein represents the opinion of the author(s), but not necessarily those of VanEck, and these opinions may change at any time and from time to time. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results, are valid as of the date of this communication and subject to change without notice. Information provided by third party sources are believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Historical performance is not indicative of future results. Current data may differ from data quoted. Any graphs shown herein are for illustrative purposes only.

ICE BofAML Diversified High Yield US Emerging Markets Corporate Plus Index comprises U.S. dollar-denominated bonds issued by non-sovereign emerging markets issuers that are rated below investment grade and that are issued in the major domestic and Eurobond markets. ICE BofAML US High Yield Index, formerly known as BofA Merrill Lynch US High Yield Index prior to 10/23/2017, is comprises below-investment grade corporate bonds (based on an average of various rating agencies) denominated in U.S. dollars.

Index returns are not Fund returns and do not reflect any management fees or brokerage expenses. Certain indices may take into account withholding taxes. Investors cannot invest directly in the Index. Returns for actual Fund investors may differ from what is shown because of differences in timing, the amount invested and fees and expenses. Index returns assume that dividends have been reinvested.

All investing is subject to risk, including the possible loss of the money you invest. Bonds and bond funds will decrease in value as interest rates rise. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.

Related Funds

DISCLOSURES

13.5% of fund net assets as of May 26, 2020. For a complete list of holdings in the ETF, please click here: https://www.vaneck.com/etf/income/hyem/overview/

Please note that Van Eck Associates Corporation serves as investment advisor to investment products that invest in the asset class(es) included herein.

This content is published in the United States for residents of specified countries. Investors are subject to securities and tax regulations within their applicable jurisdictions that are not addressed in this content. Nothing in this content should be considered a solicitation to buy or an offer to sell shares of any investment in any jurisdiction where the offer or solicitation would be unlawful under the securities laws of such jurisdiction, nor is it intended as investment, tax, financial, or legal advice. Investors should seek such professional advice for their particular situation and jurisdiction.

Emerging Market securities are subject to greater risks than U.S. domestic investments. These additional risks may include exchange rate fluctuations and exchange controls; less publicly available information; more volatile or less liquid securities markets; and the possibility of arbitrary action by foreign governments, or political, economic or social instability. High yield bonds may be subject to greater risk of loss of income and principal and are likely to be more sensitive to adverse economic changes than higher rated securities.

The information herein represents the opinion of the author(s), but not necessarily those of VanEck, and these opinions may change at any time and from time to time. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results, are valid as of the date of this communication and subject to change without notice. Information provided by third party sources are believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Historical performance is not indicative of future results. Current data may differ from data quoted. Any graphs shown herein are for illustrative purposes only.

ICE BofAML Diversified High Yield US Emerging Markets Corporate Plus Index comprises U.S. dollar-denominated bonds issued by non-sovereign emerging markets issuers that are rated below investment grade and that are issued in the major domestic and Eurobond markets. ICE BofAML US High Yield Index, formerly known as BofA Merrill Lynch US High Yield Index prior to 10/23/2017, is comprises below-investment grade corporate bonds (based on an average of various rating agencies) denominated in U.S. dollars.

Index returns are not Fund returns and do not reflect any management fees or brokerage expenses. Certain indices may take into account withholding taxes. Investors cannot invest directly in the Index. Returns for actual Fund investors may differ from what is shown because of differences in timing, the amount invested and fees and expenses. Index returns assume that dividends have been reinvested.

All investing is subject to risk, including the possible loss of the money you invest. Bonds and bond funds will decrease in value as interest rates rise. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.