What Fallen Angel Bonds Offer a Portfolio

June 24, 2020

Read Time 4 MIN

The fallout from recent market volatility included a series of corporate bond credit downgrades that expanded the fallen angel high yield bond universe. Fallen angel bonds are unique in that they are corporate bonds that were originally issued as investment grade before being downgraded to junk status. As interest rates remain low and spreads tighten, we believe fallen angel bonds may present an attractive opportunity for investors.

Welcoming New Fallen Angel Bonds—at Deep Discounts

The fallen angel market has welcomed several big names this year, including Kraft, Ford and Occidental Petroleum. After the most recent entrants at the end of May, the year to date total fallen angel market value reached $199B.1 Historically, strong returns and outperformance vs. the broad high yield market have followed years where there has been high volume of fallen angels.

In this year’s fallen angel wave, we have seen a familiar technical pattern: investment grade managers selling bonds that were downgraded to junk and driving down the bond’s price. This is when the contrarian approach of fallen angel investing comes into play: buying bonds that other market participants are selling, usually at high discounts.

For example, bonds of ArcelorMittal (Basic Industry/Steel Producer) and Services Property Trust (REIT), which became fallen angels in May, experienced an average price return of -12.44% over the six months prior to downgrade.2 Year to date, fallen angels have entered the Fallen Angel U.S. High Yield Index3 at average discounts more than twice as large as the average discount for the past 10 years. Energy sector bonds have entered at discounts even higher than the overall average for fallen angels this year.

| Past 10 Years* | YTD Fallen Angels | May Fallen Angels | June Fallen Angels | YTD Energy Fallen Angels | |

| Average 6-month Price Return Prior to Entering Index | -6.90% | -18.01% | -22.15% | -12.44% | -24.53% |

| Average Price When Entering Index | 92.01 | 85.02 | 80.47 | 91.19 | 77.82 |

Source: Factset, ICE. Data as of 5/31/2020.

*Data from 12/31/2009-12/31/2019

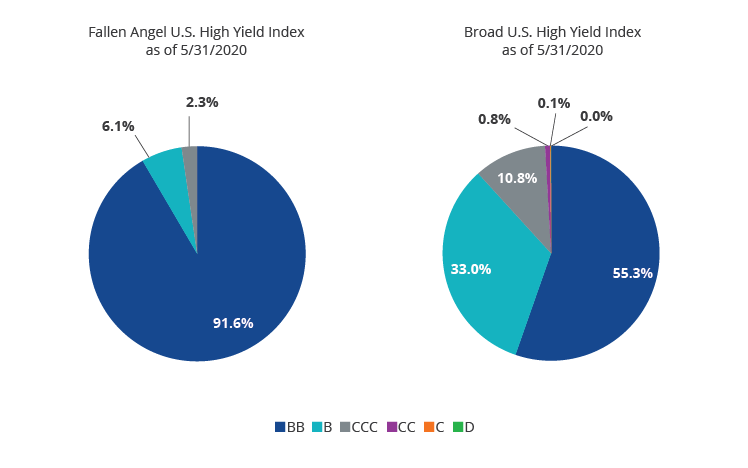

Lower Credit Risk Relative to Broad High Yield

A majority of the bonds that become fallen angels end up in the BB bucket, which means less credit risk for investors compared to the broad high yield market. After the fallen angel index welcomed a significant number of new issuers in April-month-end, it had 92% concentration to BB. In comparison, only 56% of the broad U.S. high yield market4 were rated BB. In May-month-end, the two new fallen angels were both rated BB, which kept the index’s BB exposure steady at 92% vs 55% of the broad U.S. high yield market.

Higher Credit Quality Relative to Broad High Yield

Source: ICE.

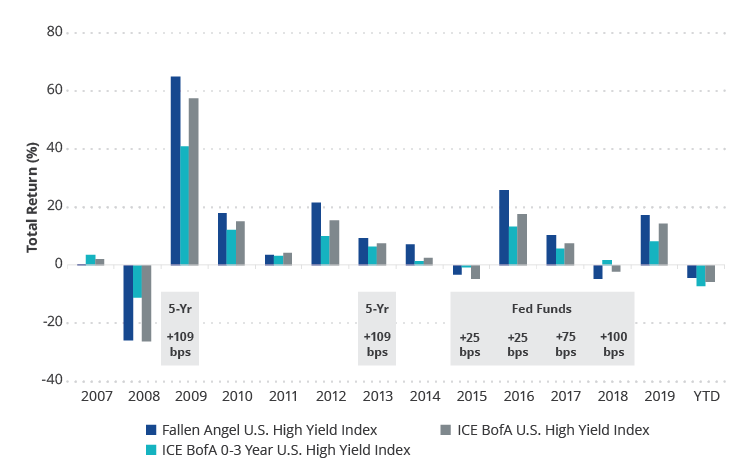

Outperformance Through Market Cycles

Investment-grade issuers tend to have lower risk, lower funding costs and better access to capital markets, and therefore tend to have bonds with longer maturities, which results in longer duration. As a result, fallen angels typically exhibit higher duration compared to original issue high yield bonds.

Although there has been a small increase in duration year to date from 5.9 on 12/31/2019 to 6.3 as of 5/31/2020 as interest rates have declined, the substantial fallen angel volume has not led to a drastically different duration profile for the fallen angel index.

Further, when interest rates have gone up historically, fallen angel bonds have outperformed the broad high yield and the short duration high yield market5 in most years, despite the longer duration, based on returns for the Fallen Angel U.S. High Yield Index, the ICE BofA US High Yield Index and the ICE BofA 0-3 Year US High Yield Index.

Historical Outperformance vs. Broad High Yield and Short Duration High Yield

Source: ICE.

For example, from 2015-2018 period, interest rates rose from 0.75% in December 2015 to 3% in December 2018 following a series of rate hikes, while credit spreads overall were nearly unchanged. Although fallen angels underperformed by an average of 40 basis points in the months in which the Federal Reserve raised interest rates, fallen angels as represented by the Fallen Angel U.S. High Yield Index outperformed over the entire period, returning 6.40% (annualized) while short high yield as represented by the ICE BofA 0-3 Year US High Yield Index only returned 4.98% (annualized).

What explains this? Often, credit spreads tighten in higher growth environments, while interest rates rise. This will generally benefit longer duration credit sensitive bonds. However, in this period, the outperformance of fallen angels was primarily driven by an overweight to energy and basic industry sector bonds. These sectors, which experienced a strong price recovery following a selloff and ratings downgrades in 2014 and 2015, drove fallen angel’s strong outperformance over this period due to the impact of buying deeply discounted bonds.

Fallen Angels vs. Short Duration High Yield in a Rising Rate Environment – 2015-2018

Source: ICE and St Louis Fed.

We anticipate 2020 to be a record year for fallen angel bond volume. Our forecast is for $250B - $300B of fallen angel volume this year. For investors, we believe this increase in volume and the discounts seen in new entrants, along with the current low interest rate environment—expected to remain in place until 2022—and continued tightening of spreads make this an attractive time to invest in fallen angel high yield bonds.

DISCLOSURES

1 Source: ICE

2 Source: ICE

3 Fallen angel index refers to the ICE US Fallen Angel High Yield 10% Constrained Index (H0CF, Index)

4 Broad U.S. High Yield refers to the ICE BofA High Yield Index (H0A0)

5 Refers to ICE BofA 0-3 Year US High Yield Index (HSA0)

Please note that Van Eck Securities Corporation (an affiliated broker-dealer of Van Eck Associates Corporation) may offer investments products that invest in the asset class(es) included herein.

This content is published in the United States for residents of specified countries. Investors are subject to securities and tax regulations within their applicable jurisdictions that are not addressed in this content. Nothing in this content should be considered a solicitation to buy or an offer to sell shares of any investment in any jurisdiction where the offer or solicitation would be unlawful under the securities laws of such jurisdiction, nor is it intended as investment, tax, financial, or legal advice. Investors should seek such professional advice for their particular situation and jurisdiction.

The information herein represents the opinion of the author(s), but not necessarily those of VanEck, and these opinions may change at any time and from time to time. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results, are valid as of the date of this communication and subject to change without notice. Information provided by third party sources are believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Any discussion of specific securities/financial instruments mentioned in the commentary is neither an offer to sell nor a recommendation to buy these securities. Historical performance is not indicative of future results. Current data may differ from data quoted. Any graphs shown herein are for illustrative purposes only.

ICE BofAML US High Yield Index (H0A0, “Broad HY Index”), formerly known as BofA Merrill Lynch US High Yield Index prior to 10/23/2017, is comprised of below-investment grade corporate bonds (based on an average of various rating agencies) denominated in U.S. dollars.

ICE US Fallen Angel High Yield 10% Constrained Index (H0CF, Index) is a subset of the ICE BofA US High Yield Index and includes securities that were rated investment grade at time of issuance.

ICE BofA 0-3 Year US High Yield Index (HSA0) is a subset of the ICE BofA US High Yield Index and includes securities with a remaining term to maturity of less than three years.

ICE Data Indices, LLC and its affiliates (“ICE Data”) indices and related information, the name "ICE Data", and related trademarks, are intellectual property licensed from ICE Data, and may not be copied, used, or distributed without ICE Data's prior written approval. The licensee's products have not been passed on as to their legality or suitability, and are not regulated, issued, endorsed, sold, guaranteed, or promoted by ICE Data. ICE Data MAKES NO WARRANTIES AND BEARS NO LIABILITY WITH RESPECT TO THE INDICES, ANY RELATED INFORMATION, ITS TRADEMARKS, OR THE PRODUCT(S) (INCLUDING WITHOUT LIMITATION, THEIR QUALITY, ACCURACY, SUITABILITY AND/OR COMPLETENESS).

All investing is subject to risk, including the possible loss of the money you invest. Bonds and bond funds will decrease in value as interest rates rise. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.

Related Funds

DISCLOSURES

1 Source: ICE

2 Source: ICE

3 Fallen angel index refers to the ICE US Fallen Angel High Yield 10% Constrained Index (H0CF, Index)

4 Broad U.S. High Yield refers to the ICE BofA High Yield Index (H0A0)

5 Refers to ICE BofA 0-3 Year US High Yield Index (HSA0)

Please note that Van Eck Securities Corporation (an affiliated broker-dealer of Van Eck Associates Corporation) may offer investments products that invest in the asset class(es) included herein.

This content is published in the United States for residents of specified countries. Investors are subject to securities and tax regulations within their applicable jurisdictions that are not addressed in this content. Nothing in this content should be considered a solicitation to buy or an offer to sell shares of any investment in any jurisdiction where the offer or solicitation would be unlawful under the securities laws of such jurisdiction, nor is it intended as investment, tax, financial, or legal advice. Investors should seek such professional advice for their particular situation and jurisdiction.

The information herein represents the opinion of the author(s), but not necessarily those of VanEck, and these opinions may change at any time and from time to time. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results, are valid as of the date of this communication and subject to change without notice. Information provided by third party sources are believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Any discussion of specific securities/financial instruments mentioned in the commentary is neither an offer to sell nor a recommendation to buy these securities. Historical performance is not indicative of future results. Current data may differ from data quoted. Any graphs shown herein are for illustrative purposes only.

ICE BofAML US High Yield Index (H0A0, “Broad HY Index”), formerly known as BofA Merrill Lynch US High Yield Index prior to 10/23/2017, is comprised of below-investment grade corporate bonds (based on an average of various rating agencies) denominated in U.S. dollars.

ICE US Fallen Angel High Yield 10% Constrained Index (H0CF, Index) is a subset of the ICE BofA US High Yield Index and includes securities that were rated investment grade at time of issuance.

ICE BofA 0-3 Year US High Yield Index (HSA0) is a subset of the ICE BofA US High Yield Index and includes securities with a remaining term to maturity of less than three years.

ICE Data Indices, LLC and its affiliates (“ICE Data”) indices and related information, the name "ICE Data", and related trademarks, are intellectual property licensed from ICE Data, and may not be copied, used, or distributed without ICE Data's prior written approval. The licensee's products have not been passed on as to their legality or suitability, and are not regulated, issued, endorsed, sold, guaranteed, or promoted by ICE Data. ICE Data MAKES NO WARRANTIES AND BEARS NO LIABILITY WITH RESPECT TO THE INDICES, ANY RELATED INFORMATION, ITS TRADEMARKS, OR THE PRODUCT(S) (INCLUDING WITHOUT LIMITATION, THEIR QUALITY, ACCURACY, SUITABILITY AND/OR COMPLETENESS).

All investing is subject to risk, including the possible loss of the money you invest. Bonds and bond funds will decrease in value as interest rates rise. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.