Will U.S. Growth Shocks Batter EM?

27 April 2023

Read Time 2 MIN

U.S. Slowdown

The flash estimate for the U.S. Q1 GDP growth was much weaker than expected, slowing to 1.1% quarter-on-quarter annualized vs. 1.9% expected. While the print had no discernible impact on market expectations about next month’s rate hike by the U.S. Federal Reserve (88% implied probability or so), it did raise questions about potential implications for emerging markets (EM), especially if U.S. growth weakness persists due to tightening credit conditions.

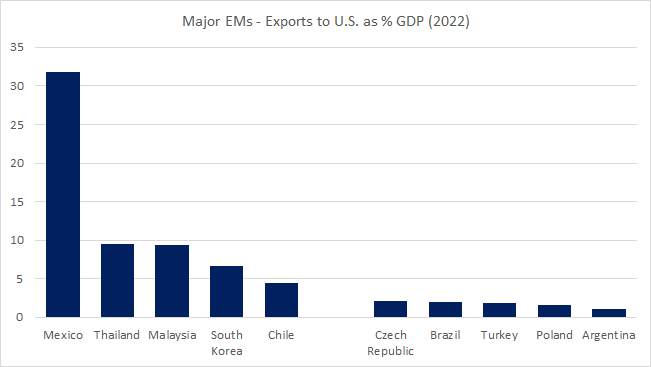

Mexico Nearshoring

There are various ways to gauge the impact of exogenous shocks on growth – one of them is to look at transmission via trade channels. The chart below shows the share of exports to the U.S. from major EMs as a percentage of their respective GDP. Mexico is a standout on this metric, and it remains to be seen whether the nearshoring story – which is a great longer-term investment theme – will help to shield the economy (and the Mexican peso) in the coming months.

EM Growth and China Rebound

Central European countries and Brazil look significantly less exposed via trade channels – the former are joined at the hip with Europe (which is why we keep an eye on tomorrow’s Q1 flash GDP print there) and the latter is a more closed economy than Mexico. Several Asian economies also have significant trade exposure to the U.S., but their stronger correlation with China’s rebound should help to mitigate the negative impact of potential growth headwinds from the U.S. Stay tuned!

Chart at a Glance: EM Exports to the U.S. – Top 10, Bottom 10

Source: VanEck Research; Bloomberg LP.

Related Insights

Related Insights

10 febrero 2026

06 marzo 2025

20 febrero 2025

10 febrero 2026

La erosión del valor de la moneda vuelve a estar en el centro de atención. A continuación, analizamos qué lo está impulsando, qué podría revertirlo y cómo estamos posicionando las carteras en ambos escenarios.

07 abril 2025

Los aranceles de Trump avivan los temores de una guerra comercial, impulsando la volatilidad del mercado, el riesgo inflacionario y la amenaza de una recesión. Ante posibles represalias globales, el crecimiento a corto plazo corre un riesgo evidente.

06 marzo 2025

Los aranceles de Trump, la próxima fase de la IA y una posible revalorización del oro estadounidense podrían sacudir los mercados; los inversores que se adelanten a estas transiciones estarán mejor posicionados.

20 febrero 2025

El avance de la IA en China, la persistente inflación, el rendimiento superior del oro y el aumento de la demanda energética ponen de relieve un panorama de inversión cambiante.

16 enero 2025

En 2025, superar los problemas significa equilibrar la innovación tecnológica, las coberturas contra la inflación, los cambios energéticos y los riesgos derivados de los recortes del gasto y la inflación.