Harnessing Growth: Online Food Delivery Brings It

November 13, 2020

Read Time 12 MIN

As emerging markets (EM) countries waver between lifting and tightening COVID-19 related restrictions, we see a reacceleration of stay-at-home behavior. This trend is implicit in digitization, including online food delivery, payments, telemedicine, video entertainment, etc. In particular, online food delivery has grown substantially. We discussed trend acceleration1 in our recent blogs on Africa, Brazil and India, and food delivery is the top player in the digital acceleration club. Its structural growth trend is persistent across emerging markets and can be found in Asia, EMEA, LatAm and Africa – home to Meituan Dianping, Delivery Hero and Prosus N.V., some of the most resilient, innovative and disruptive portfolio companies in the Consumer Discretionary space.

“The COVID crisis has moved food delivery from a luxury to utility.”

~ Dara Khosrowshahi (CEO, Uber), 2Q20 Earnings CallThe Future of Online Food Delivery: Unprecedented Growth Opportunities

The global food service delivery market is estimated to grow to $1 trillion USD in the long term.2 Urbanization, digital penetration and an increased demand for convenience (i.e., out-of-home delivery service) have been driving demand globally. In comparison to developed markets (DM), online food delivery in EM is at early stages of development, creating ample opportunity for structural growth investing and potential for alpha generation. We believe this is a long-term, sustainable, structural growth theme that will continue to trend upwards in the future.

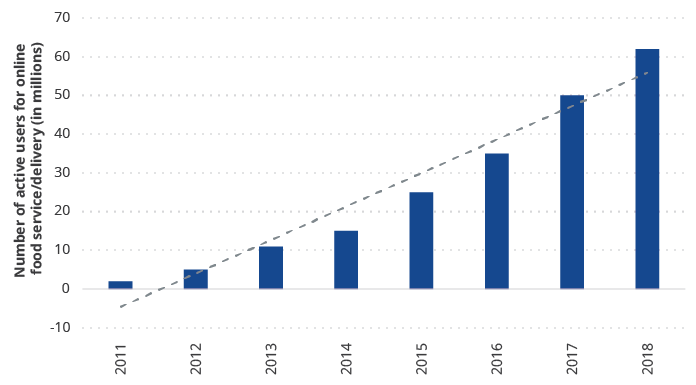

The number of active users for online food service/delivery is upward trending globally.

Source: HSBC Global Research. Data as of October 2019.

Meituan Dianping – Leading Online Food Delivery and Local Services in China

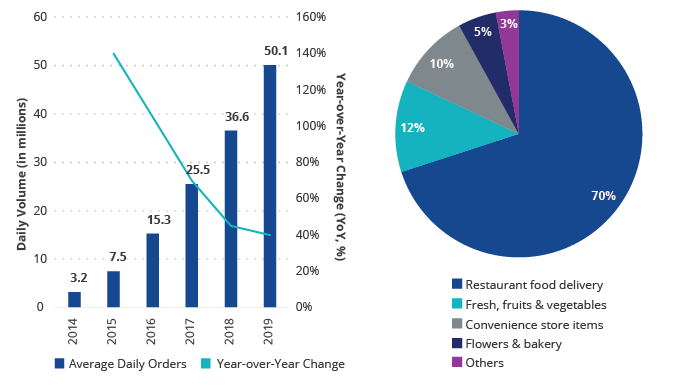

In many ways, China is at the leading edge of the online food delivery space globally. In its early years, the food delivery business model was a polarizing topic among investors. Many believed it was a model that was too difficult to build a sustainable moat around. A lack of differentiation among platforms and low user switching costs promoted aggressive price wars that bears being viewed as a race to the bottom with no path to profitability. Despite these challenges, Meituan has emerged as China’s food delivery leader. Their market leadership is built on superior execution led by their CEO Wang Xing, who is held in very high esteem in China’s tech community. As presented in charts below, the country’s total on-demand delivery orders reached over 50 million in 2019, with food delivery representing 70% of those orders.

China’s on-demand delivery markets reached over 50 million of daily orders in 2019, with food delivery representing 70% of those orders.

Source: CFLP, Company Data, Goldman Sachs Global Investment Research. Data as of June 11, 2020.

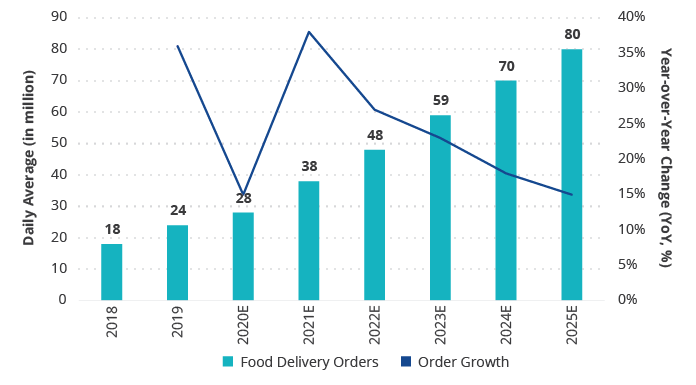

Meituan Dianping (2.19% of Strategy assets) is China’s leading e-commerce services platform company. Its apps connect consumers, including local businesses for food delivery, in-store dining, hotel bookings, among other services. Through strong execution on cross-selling an expanding array of lifestyle services to users and its merchant oriented focus, Meituan has become the largest food delivery network in the world, completing 25 million orders per day in 2Q 2020.3 We estimate Meituan’s online food delivery orders to grow to 80 million per day by 2025E.

We estimate Meituan’s online food delivery orders to grow to 80 million per day by 2025E.

Source: Company Data, Goldman Sachs Global Investment Research. Data as of August 24, 2020.

E = Estimates.

Our structural growth thesis is based on the following:

- As China’s food consumption continues its unrelenting upward trend, we expect online food delivery penetration to reach 15% by 2025E. Given Meituan’s unmatched scale and execution prowess, we view it as well positioned to capitalize and expand its dominance in the space.

- China’s online food delivery market structure remains favorable for Meituan as it continues to be highly concentrated, creating an environment where existing market participants can be incrementally more focused on profitability as opposed to aggressively pursuing market share.

- The company’s leading market share is driven by its: a) largest self-operated 1P4 team in China, solely dedicated to Meituan and its delivery model; b) growing food delivery user base of over 35 million; c) merchant coverage leadership, driven by restaurant review and local services; and d) successful track-record in cross-selling “Food” users into its “Platform.”

- As Meituan continues to evolve, its core principles remain the same with an unwavering prioritization of user activity and data. By getting users to use essential high frequency services on their platform, they gain user attention even if unprofitable. High frequency services give them data, which is the intangible asset that the company builds its platform around. This explains how it has successfully moved up the value chain in e-commerce services from low profit bike rental to ride sharing to delivery, reservations and even high margin segments like beauty treatments. Ultimately, we believe that Meituan will be successful in evolving into China’s leading e-commerce services platform.

Meituan’s recent performance further consolidates our conviction in this portfolio company. It was primarily driven by a strong recovery in revenue, accompanied by greater than expected profitability. Sentiment was further boosted by market share gains in food delivery as well as new initiatives (e.g., groceries), which should serve to meaningfully expand the company’s target addressable market in the future.

Our EME team has been monitoring Meituan since its IPO in September 2018. However, it wasn’t until March 2020 that COVID created what we viewed as a compelling buying opportunity—when the stock sold off approximately 30% from peak to trough. Since then our initial thesis has played out nicely with Meituan emerging as a winner from COVID related lockdowns in China.

Delivery Hero – Mapping Food Delivery and Growth Trajectory across EM

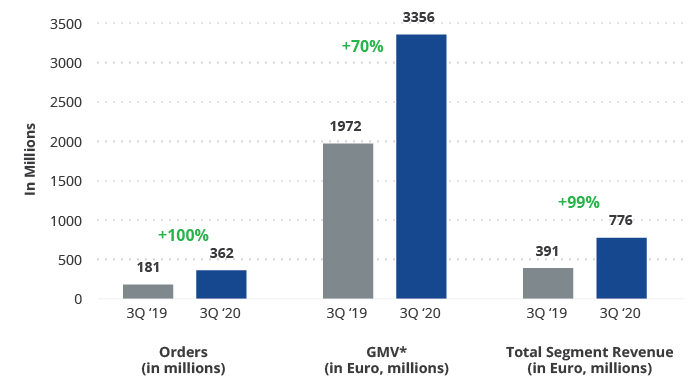

Delivery Hero (1.94% of Strategy assets)5 is an ambitious and truly inspiring food delivery service listed in Germany. While the company remains headquartered in Germany, most of its actual operations are based in emerging markets – spanning across EMEA, LatAm and Asia – operating in close to 50 countries globally and leading online food delivery in 90% of them.

Delivery Hero doubled orders with a YoY growth of 100%, while decreasing delivery time (-12% YoY).

Source: Company Data, 3Q20 Results Presentation. Data as of September 30, 2020.

*GMV = Gross Merchandise Value.

We believe that Delivery Hero’s scale and platform offer a unique play for EM structural growth. Our investment thesis is based on the following analysis:

- Leadership in low penetration online food delivery markets: The company has done a great job researching global markets, identifying markets with low penetration levels and investing heavily in these markets ahead of others and in bigger scale to establish dominance.

- Expansion through own delivery capabilities: more markets may mean more opportunities. In addition to growing through a marketplace model, Delivery Hero has invested in its own delivery services in most of its markets. This helps it further grow the addressable market by adding more restaurants and regions that were previously less accessible through the marketplace model, while also constantly improving the customer experience.

- Robust M&A activity: The company views the food delivery market as a winner takes all or most type of business, strongly lending itself to network effects (i.e., growing and sticky customer base) and large economies of scale (i.e., technology, marketing, etc.). As such, it has been active in M&A deals to capture synergies and accelerate the path to leadership and profitability.

- Room for margin expansion and higher profitability: MENA is by far the company’s strongest region, offering proven and sustained profitability. Delivery Hero has high hopes for Emerging Europe, LatAm and Asia as well. Asia remains highly competitive, but the company continues to invest in the region, given the enormous opportunity there both organically and through M&A—evidenced in its move to acquire rival Woowa in South Korea, which would significantly improve its competitive positioning and profitability in the market (currently awaiting regulatory approval). Acceleration in order growth, supported along with higher efficiency in number of deliveries per hour through optimized fleet utilization, have resulted in better unit economics across the board in 2020.

- Entering new verticals: Delivery Hero is also leveraging its experience and delivery capabilities to enter into some of the newer fast growing verticals like grocery delivery. It has launched a network of “dark convenience stores”6 under the Dmart banner and recently acquired Instashop, an online grocery delivery platform present across several markets in MENA, which positions the company well for further growth going forward.

Delivery Hero’s recent performance further reinforces our thesis – the company did, indeed, produce what we believe as “heroic” performance. There is now better appreciation that the company’s current level of investment will bear fruit. M&A activity in the sector has also shone a light on just how undervalued this sector has been. We have held a position in Delivery Hero since the IPO of the company in 2017 and continue to believe in the long-term prospects of the business.

Prosus – Buying into Online Food Delivery and Digitization across EM

Prosus N.V. (2.86% of Strategy assets), a subsidiary and recent spinoff from our long-time holding in South Africa’s Naspers7, comprises a portfolio of leading digital assets outside of South Africa across Asia, Emerging Europe, MENA and LATAM. In addition to its 31% stake in Tencent Holdings and 21% stake in Delivery Hero (both portfolio companies in the Strategy), Prosus is heavily invested in three key e-commerce verticals – direct beneficiaries of the global digitization trend – online food delivery, online classifieds and payments & fintech.

Our structural growth thesis is based on the following:

- Prosus is well positioned to benefit across its platform from the accelerated shift to digital during the pandemic.

- The company presents a strong fundamental outlook partly driven by Tencent, which should benefit from a robust pipeline of new releases and international expansion in gaming, ongoing momentum in social advertising and further improvement in cloud and payment transactions.

- Focusing more closely on food delivery, Prosus has seen an acceleration in order growth across the majority of its assets and narrowing in losses as discussed earlier with Delivery Hero. The company’s key asset in Latin America, iFood, which is majority owned by Prosus and is the dominant online food delivery player in Brazil, has done exceptionally well this year with orders doubling and GMV growth accelerating to 118% in 1H 2020 from 91% in 2019. Prosus has expressed interest in acquiring the remaining minority stake in iFood currently owned by Just Eat Takeaway, which we would like, given the high quality and fast growth nature of this asset. Prosus also owns a 39% stake in Swiggy, a strong player in the online food delivery market in India with more than 160,000 restaurant partners across 520 cities. Unlike iFood, Swiggy has faced some headwinds this year due to stricter COVID-19 related lockdowns in India with restaurants being forced to close down, putting pressure on the supply side. Swiggy has proactively entered into new verticals like grocery delivery to partially offset the pressure on the restaurant side of the business. With lockdowns now slowly easing in India, we are starting to see recovery in that side of the business and the longer term opportunity set remains attractive. Finally, Prosus also has indirect exposure to the Russian online food delivery market through its 28% stake in Mail.ru owner of Delivery Club, which has also been booming this year.

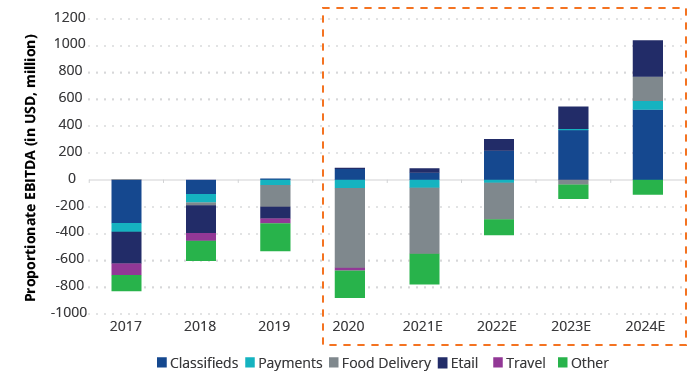

While we expect further investments in this vertical in assets like Swiggy, we believe 2020 may mark peak losses in food delivery, with focus increasingly shifting from “land-grab” to profits.

In 2020, Prosus focus shifts from “land-grab” to profits.

Source: Company Data, Goldman Sachs Global Investment Research. Data as of November 3, 2020.

E = Estimates.

Prosus’ recent and expected performance has been solid across most verticals, and the stock has done well YTD. However, we have actually seen the share price’s discount to NAV (which remains dominated by Tencent) widening to historical highs, although we expect the earnings growth of the company’s ex-Tencent assets to outpace the earnings growth of Tencent over the coming three years. This should help narrow the discount going forward. Additionally, we have seen management engage in multiple large scale M&A attempts but remaining disciplined in not overpaying for assets in this environment, while recently announcing a $5 billion share buyback program split between Naspers and Prosus shares. We take this as a vote of confidence in the company’s future outlook and a reflection of management’s eagerness to unlock shareholder value, particularly given the current attractive valuation levels.

We have only held Prosus in the portfolio since its spin-off from Naspers last year and its listing in the Netherlands to facilitate access to a wider base of global investors that may not prefer to invest in a Johannesburg Stock Exchange listed company. That said, Naspers itself is an old friend that we have held in the portfolio for many years and that has done well for us. We are encouraged by management’s increased disclosure levels and commitment to further unlock shareholder value, and we remain positive on the future prospects of the company.

Looking Forward

Trend acceleration has been quite positive for the VanEck Emerging Markets Equity Strategy. Our focus on many of these structural growth areas enabled us to invest in Meituan Dianping, Delivery Hero and Prosus N.V. These companies are showing strong growth potential and recent earnings results further solidify our conviction in these names. As a result, our outlook is optimistic for the remainder of 2020 and beyond, despite the current challenges. A key driver of our outlook for the end of 2020 and beyond is an expectation of global growth recovery, boosted by a timely introduction of a COVID-19 vaccine and its distribution schedule.

DISCLOSURES

1 The global pandemic has accelerated growth in certain sectors and industries such as digital payments, e-commerce, data centers, telemedicine and video gaming, with disruption timelines shortening. This acceleration trend is quite positive for our active VanEck Emerging Markets Equity Strategy, as we have always been forward looking, focused on many of these structural growth areas and, as a result, we currently see that positive prospects for many of our portfolio companies actually accelerated.

2 Source: HSBC Global Research. Data as of October 2019.

3 Source: Company Data, Goldman Sachs Global Investment Research. Data as of August 24, 2020.

4 1P marketplace model means that the company sells its own inventory; whereas 3P model implies that the company operates platforms for other businesses to sell its inventory.

5 Naspers owns a 21% stake in the company.

6 The term “dark convenience store,” “dark supermarket” or “dotcom centre” refers to a retail outlet or distribution centre that caters exclusively for online shopping. A dark convenience store is generally a large warehouse that can either be used to facilitate a "click-and-collect" service, where a customer collects an item they have ordered online or as an order fulfilment platform for online sales.

7 Naspers owns a majority stake (72.5%) in Prosus N.V.

The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results, are valid as of the date of this communication and subject to change without notice. Information provided by third party sources are believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. The information herein represents the opinion of the author(s), but not necessarily those of VanEck.

This is not an offer to buy or sell, or a recommendation to buy or sell any of the securities mentioned herein. Strategy holdings will vary.

Emerging Market securities are subject to greater risks than U.S. domestic investments. These additional risks may include exchange rate fluctuations and exchange controls; less publicly available information; more volatile or less liquid securities markets; and the possibility of arbitrary action by foreign governments, or political, economic or social instability.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.

Van Eck Associates Corporation

Related Funds

DISCLOSURES

1 The global pandemic has accelerated growth in certain sectors and industries such as digital payments, e-commerce, data centers, telemedicine and video gaming, with disruption timelines shortening. This acceleration trend is quite positive for our active VanEck Emerging Markets Equity Strategy, as we have always been forward looking, focused on many of these structural growth areas and, as a result, we currently see that positive prospects for many of our portfolio companies actually accelerated.

2 Source: HSBC Global Research. Data as of October 2019.

3 Source: Company Data, Goldman Sachs Global Investment Research. Data as of August 24, 2020.

4 1P marketplace model means that the company sells its own inventory; whereas 3P model implies that the company operates platforms for other businesses to sell its inventory.

5 Naspers owns a 21% stake in the company.

6 The term “dark convenience store,” “dark supermarket” or “dotcom centre” refers to a retail outlet or distribution centre that caters exclusively for online shopping. A dark convenience store is generally a large warehouse that can either be used to facilitate a "click-and-collect" service, where a customer collects an item they have ordered online or as an order fulfilment platform for online sales.

7 Naspers owns a majority stake (72.5%) in Prosus N.V.

The information presented does not involve the rendering of personalized investment, financial, legal, or tax advice. Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results, are valid as of the date of this communication and subject to change without notice. Information provided by third party sources are believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. The information herein represents the opinion of the author(s), but not necessarily those of VanEck.

This is not an offer to buy or sell, or a recommendation to buy or sell any of the securities mentioned herein. Strategy holdings will vary.

Emerging Market securities are subject to greater risks than U.S. domestic investments. These additional risks may include exchange rate fluctuations and exchange controls; less publicly available information; more volatile or less liquid securities markets; and the possibility of arbitrary action by foreign governments, or political, economic or social instability.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.

Van Eck Associates Corporation