Market Recap: Rebuilding for Resiliency

June 25, 2026

Read Time 5 MIN

Key Takeaways:

- The crisis will pass. The lesson won't: COVID and Iran are different events with the same message — systems built purely for efficiency will break under stress.

- Resilience is the new growth theme: The world is shifting from decades of optimization to a multi-year rebuild of energy, manufacturing, and infrastructure.

- AI and reshoring are telling the same story: Two powerful forces are converging on the same real assets, and the opportunity is where they meet.

- The builders are already winning: Markets are rewarding companies at the center of this structural shift, and we believe the trend has significant runway ahead.

Rebuilding for Resiliency

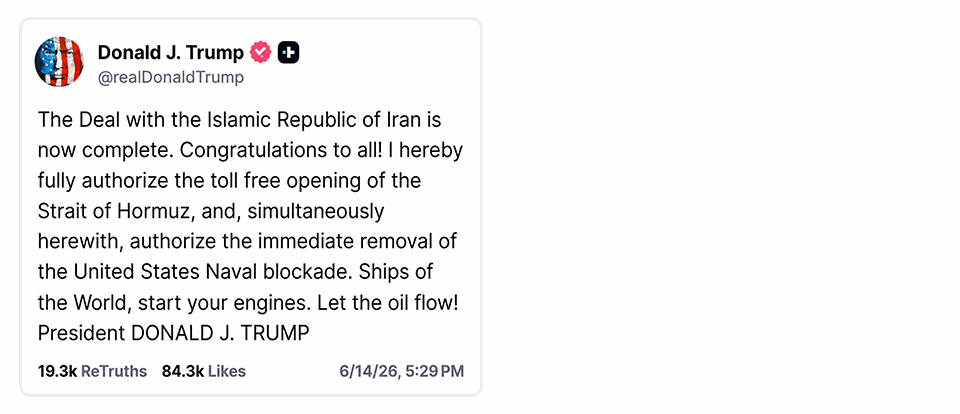

A Reason to Celebrate

Markets rallied on news of an initial deal with Iran. They should. Lower and more stable oil prices ease inflation and reduce a threat to growth.

Got it.

Source: Truth Social, 6/14/26.

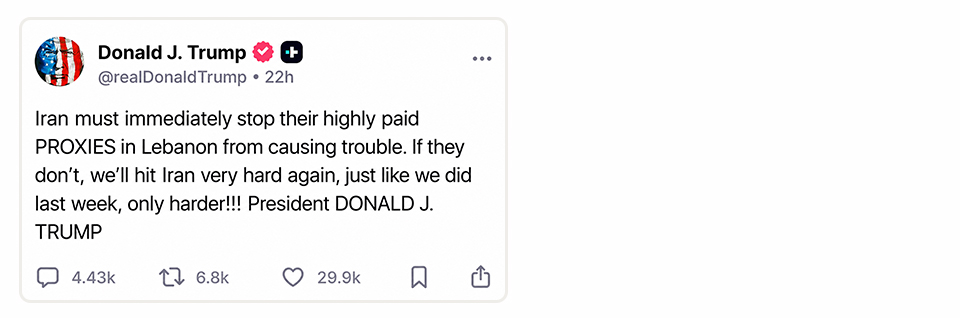

A Reason to Pause

We are not out of the woods yet.

Since the conflict began, President Trump repeatedly declared victory. The deal was days away. Then weeks away. Then days away again. Today we appear genuinely closer to resolution. That is encouraging. But the last several months should remind us that geopolitical conflicts rarely follow a straight line.

A positive outcome is not the only possible outcome.

Source: Truth Social, 6/21/26.

If the agreement falters and oil prices rise materially, inflation reaccelerates. That alone is manageable. What is not manageable is a Fed that panics and responds with easy money. Iran would be the spark. The Fed would be the fan. That combination could produce a second inflationary wave not unlike 2022.

We don't expect that to happen. The deal will hold. Neither side will be completely satisfied, both will act up, and eventually both will declare victory. That is how these things end.

The chart below compares the current inflation regime to the inflation regime of the 1970s. It shows how historical inflation regimes typically present in waves. At this point, we believe that the current inflation spike will not transform into an inflation wave.

But that is not the big story.

The Wave that Wasn’t

Source: BLS, 05/2026. Past performance is not a guarantee of future results. Estimates may not materialize as predicted and are subject to change.

The Second Wake-Up Call

The big story is that this is the second time in five years we have been reminded how fragile the systems we depend on truly are.

COVID was the first wake-up call.

Most of us remember walking into grocery stores and finding empty shelves. It was jarring. The extraordinary efficiencies built over decades collapsed the moment the system was stressed.

Iran was the second.

A country on the other side of the world threatened a single chokepoint responsible for roughly 20% of the world's oil supply. The result was an immediate energy shock. This chart shows the tanker vessel crossings plummet in the Strait of Hormuz.

The Day the Strait Went Silent

Source: Bloomberg, 6/18/26. Past performance is not a guarantee of future results. Estimates may not materialize as predicted and are subject to change.

At first glance, the two events appear unrelated. One was a pandemic. The other was a geopolitical conflict.

Both exposed the same flaw: critical systems are only as strong as their weakest link.

Iran was not the story. Iran was the reminder.

Recommended subscription

The Lesson

COVID was temporary. The lesson was not.

Iran will prove temporary too. The lesson is not.

For decades, the global economy was built for efficiency. Lower costs. Higher margins. Lean supply chains. Just-in-time everything. It produced extraordinary productivity and cheaper goods.

It also produced a system with almost no slack. Anything pushed to an extreme eventually breaks. Even globalization.

The next system will be built differently. Not for efficiency alone, but for efficiency and resilience. That means more domestic manufacturing, more energy security, more critical mineral production, more infrastructure, and more redundancy throughout the system.

Put simply: we expect to rebuild at home critical industries that today exist abroad.

Not because we want to. Because we must. And we are unlikely to be alone. Much of the developed world is reaching the same conclusion.

That is one of the key forces behind the next great global infrastructure buildout.

Building the Future

This shift did not begin with COVID and will not end with Iran. Both events accelerated a trend already underway.

Governments and corporations are increasingly willing to pay for security and redundancy. That means more manufacturing, more energy investment, more power generation, more grid modernization, more critical mineral development, and more security across the board.

In short: more spending.

But the story goes beyond reshoring.

At the same time the world is rebuilding for resilience, it is building for a new technological era. For most of human history, knowledge was scarce. Artificial intelligence is ending that scarcity. That changes everything.

But AI does not scale without real assets. The new world does not happen without the old world building it.

AI and reshoring are driving demand for the same things: power generation, critical minerals, manufacturing capacity, and infrastructure.

Different forces. Same destination.

Markets are already rewarding the beneficiaries. The UBS US Reshoring Index, which includes companies such as Caterpillar, Rockwell Automation, Steel Dynamics, and United Rentals, has outperformed the S&P 500 Index over the past three years. These are not AI companies. They are the companies building the world AI requires.

The Builders are Winning

Source: Bloomberg, 06/18/26. Past performance is not a guarantee of future results. Estimates may not materialize as predicted and are subject to change.

The world is moving from the economy we know today to one shaped by artificial intelligence. Getting there requires one of the largest infrastructure buildouts in modern history. What began as a technology spending cycle is becoming a global infrastructure upgrade cycle.

Where We See Opportunity

The market is focused on whether the Iran deal holds.

We are focused on what it reminded us of.

COVID exposed the supply chain fragility. Iran exposed the energy system fragility. Artificial intelligence is accelerating infrastructure demand.

These are not separate trends. They are reinforcing each other.

The world spent decades building for efficiency. It may spend the next decade or two building resilience.

The crisis will pass.

The trend will not.

To receive more Model Portfolio insights, sign up in our subscription center.

Important Disclosures:

Index definitions

The S&P 500® Index consists of 500 widely held common stocks covering industrial, utility, financial and transportation sector; as an Index, it is unmanaged and is not a security in which investments can be made.

The UBS US Reshoring Index consists of a static basket of 39 US-listed common stocks covering the industrial, construction, materials and electrical-equipment sectors representing the US AI and reshoring theme; as an Index, it is unmanaged and is not a security in which investments can be made.

The Bloomberg Strait of Hormuz Tanker Vessel Crossings Index (TRHBTKCD Index) is based on AIS-based vessel tracking with a roughly 30-minute refresh and a rolling 24-hour window; as an Index, it is unmanaged and is not a security in which investments can be made.

This is not an offer to buy or sell, or a recommendation to buy or sell any of the securities, financial instruments or digital assets mentioned herein. The information presented does not involve the rendering of personalized investment, financial, legal, tax advice, or any call to action. Certain statements contained herein may constitute projections, forecasts and other forward-looking statements, which do not reflect actual results, are for illustrative purposes only, are valid as of the date of this communication, and are subject to change without notice. Actual future performance of any assets or industries mentioned are unknown. Information provided by third party sources are believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. VanEck does not guarantee the accuracy of third party data. The information herein represents the opinion of the author(s), but not necessarily those of VanEck or its other employees.

The models are not mutual funds or other types of securities and will not be registered with the Securities and Exchange Commission as investment companies under the Investment Company Act of 1940, as amended, and no units or shares of the models will be registered under the Securities Act of 1933, as amended, nor will they be registered with any state securities regulator. Accordingly, the models are not subject to compliance with the requirements of such acts.

The portfolio holdings presented represent securities held as of the period indicated and may not be representative of current or future investments. Such data may vary for each client in the strategy due to, but not limited to, asset size, market conditions, client guidelines and the diversity of portfolio holdings. Portfolio holdings are subject to change without notice and are being provided for illustrative purposes only. Nothing contained herein should be construed as (i) an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. This material is being provided for illustrative purposes only. Past performance is no guarantee of future results.

An investment in the strategies may be subject to risks which include, among others, equity securities, market, volatility, futures contract, investments related to bitcoin and bitcoin futures, derivatives, social media analytics, information technology, communication services, consumer discretionary, software and internet software, financials and semiconductor industries, emerging market securities, counterparty, foreign securities, foreign currency, non-U.S. issuers, investment capacity, target exposure and rebalancing, small- and medium-capitalization companies, borrowing and leverage, indirect investment, credit, interest rate, illiquidity, investing in other investment companies, management, non-diversified, operational, portfolio turnover, regulatory, repurchase agreements, tax, cash transactions, authorized participant concentration, no guarantee of active trading market, trading issues, fund shares trading, premium/discount and liquidity of fund shares, U.S. government securities, debt securities, municipal securities, securitized/asset-backed securities, and sovereign bond risks, all of which could significantly and adversely affect the strategies.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future performance.

© Van Eck Associates Corporation.

Intelligently-designed exposure across asset classes for diversified portfolios

Important Disclosures:

Index definitions

The S&P 500® Index consists of 500 widely held common stocks covering industrial, utility, financial and transportation sector; as an Index, it is unmanaged and is not a security in which investments can be made.

The UBS US Reshoring Index consists of a static basket of 39 US-listed common stocks covering the industrial, construction, materials and electrical-equipment sectors representing the US AI and reshoring theme; as an Index, it is unmanaged and is not a security in which investments can be made.

The Bloomberg Strait of Hormuz Tanker Vessel Crossings Index (TRHBTKCD Index) is based on AIS-based vessel tracking with a roughly 30-minute refresh and a rolling 24-hour window; as an Index, it is unmanaged and is not a security in which investments can be made.

This is not an offer to buy or sell, or a recommendation to buy or sell any of the securities, financial instruments or digital assets mentioned herein. The information presented does not involve the rendering of personalized investment, financial, legal, tax advice, or any call to action. Certain statements contained herein may constitute projections, forecasts and other forward-looking statements, which do not reflect actual results, are for illustrative purposes only, are valid as of the date of this communication, and are subject to change without notice. Actual future performance of any assets or industries mentioned are unknown. Information provided by third party sources are believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. VanEck does not guarantee the accuracy of third party data. The information herein represents the opinion of the author(s), but not necessarily those of VanEck or its other employees.

The models are not mutual funds or other types of securities and will not be registered with the Securities and Exchange Commission as investment companies under the Investment Company Act of 1940, as amended, and no units or shares of the models will be registered under the Securities Act of 1933, as amended, nor will they be registered with any state securities regulator. Accordingly, the models are not subject to compliance with the requirements of such acts.

The portfolio holdings presented represent securities held as of the period indicated and may not be representative of current or future investments. Such data may vary for each client in the strategy due to, but not limited to, asset size, market conditions, client guidelines and the diversity of portfolio holdings. Portfolio holdings are subject to change without notice and are being provided for illustrative purposes only. Nothing contained herein should be construed as (i) an offer to buy any security or (ii) a recommendation as to the advisability of investing in, purchasing or selling any security. This material is being provided for illustrative purposes only. Past performance is no guarantee of future results.

An investment in the strategies may be subject to risks which include, among others, equity securities, market, volatility, futures contract, investments related to bitcoin and bitcoin futures, derivatives, social media analytics, information technology, communication services, consumer discretionary, software and internet software, financials and semiconductor industries, emerging market securities, counterparty, foreign securities, foreign currency, non-U.S. issuers, investment capacity, target exposure and rebalancing, small- and medium-capitalization companies, borrowing and leverage, indirect investment, credit, interest rate, illiquidity, investing in other investment companies, management, non-diversified, operational, portfolio turnover, regulatory, repurchase agreements, tax, cash transactions, authorized participant concentration, no guarantee of active trading market, trading issues, fund shares trading, premium/discount and liquidity of fund shares, U.S. government securities, debt securities, municipal securities, securitized/asset-backed securities, and sovereign bond risks, all of which could significantly and adversely affect the strategies.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future performance.

© Van Eck Associates Corporation.