Crypto Lending and the Search for Yield

February 01, 2022

Read Time 4 MIN

Please note that VanEck has exposure to Bitcoin.

Earning Yield on Cryptocurrency

One of the more notable cryptocurrency developments in recent years is the ability to earn yield by lending digital assets, including Bitcoin and stablecoins, to centralized exchanges, OTC traders and decentralized finance (DeFi) protocols.1 The underlying sources of such yield include, but are not limited to, profits from the futures-based “cash and carry”2 trade. Given the persistent contango3 in the Bitcoin futures market, the annualized roll yield on such a trade has averaged 13.7% over the last year.4

Other sources of crypto yield include trading profits from the wide-ranging arbitrage opportunities in a still-fragmented exchange market, along with the commissions charged by decentralized exchange protocols to access borrow and lending liquidity. Those trading commissions are generally denominated in the “protocol” coin of whatever DeFi exchange facilitates the trade. This means that investors looking to cash out to dollars or stablecoins must often make a series of additional intermediate transactions, incurring even more trading costs that accrue to protocol value, and eventually, comprise the source of funds to repay dollar loans.

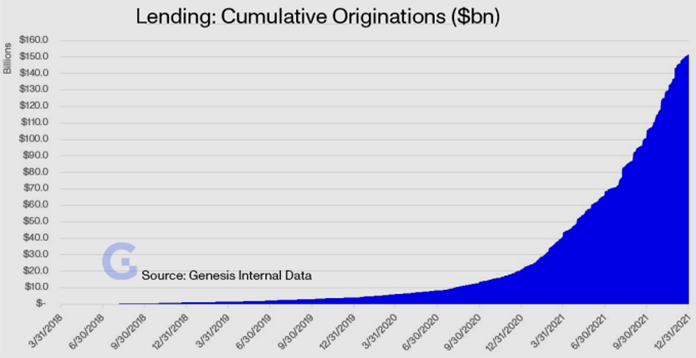

Put simply, since crypto enables micro-payments that were not previously economically rational, market participants trade more frequently. And with banks and many other financial institutions still unwilling and unable to touch crypto, a persistent shortage of dollars has created short-term lending opportunities above 8%, at potentially low volatility levels.5 As an example of the size of this market, Genesis, one of the largest OTC players, claims $150B in cumulative originations and a current loan book of $12.5B (Fig 1). VanEck participates in these “new finance” income markets via short-term loans to the larger corporate digital asset intermediaries through the VanEck New Finance Income Strategy.

Fig. 1. Crypto Lending: Genesis Cumulative Originations

Source: Genesis. Data as of 12/31/2021.

There are two primary risks with such a strategy: one macro and one micro. First, a sudden downdraft in Bitcoin and crypto assets could swamp multiple lenders’ value-at-risk models, causing mass liquidations and defaults across the space and invalidating the entire business model. In a way this is what happened to Lehman Brothers and the rest of Wall Street in 2008. Many bears who see no value in digital assets assume this end-game. And yet remarkably, despite five separate 35% declines in Bitcoin since the start of 2020, including two consecutive 30%+ intraday down days in March 2020, the ecosystem has never seen a major bankruptcy.

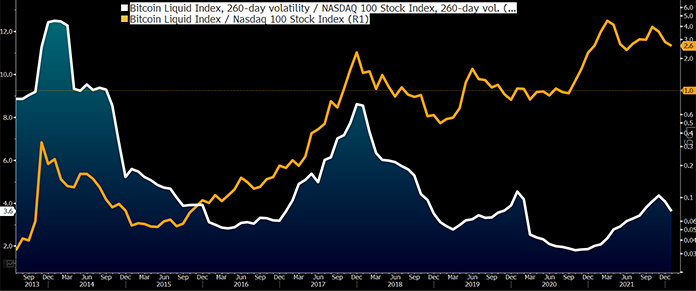

That resilience was tested yet again over the January 22-23 weekend, when algorithmic market maker and proprietary trading firm Tantra Labs reportedly liquidated after suffering “performance degradation” and failing to raise fresh capital.6 Still, as can be seen in fig. 2, there was no major liquidation cycle among BTC futures participants this time. Bitcoin price volatility may be high, but in relative terms it continues to fall (fig. 3). It seems the larger lenders are positioned for worse.

Fig. 2. Bitcoin Aggregated Liquidations

Source: Glassnode, as of 1/28/2022.

Fig. 3. Bitcoin Price Volatility & Performance vs. Nasdaq 100

Source: Bloomberg, as of 1/28/2022. Orange Line = Bitcoin Price / Nasdaq Price. White Line = Bitcoin vol / Nasdaq Vol.

The second major risk to a lending strategy such as this involves the individual counterparty and its unique risk management processes and abilities. Better-capitalized counterparties with emerging brand value are likely to shield their lenders from some losses by smoothing out the more volatile rates in DeFi. This allows them to capture healthy spreads in both good and bad markets but also use financial resources when necessary to support franchise value and maintain good relations with the fixed income markets via attractive yields.

Certainly there is plenty of leeway on this front: for context, Coinbase’s ROA (return on assets) is 7.8% in 2020, and JPMorgan’s is 1.3% in 2021.7 We believe traditional credit analysis, supplemented by NDAs, is possible in this market, and we talk regularly with potential borrowers to discuss their own onboarding process, loan approval process, loan durations, position monitoring, concentration risks, worst case scenario-modeling and more. Given the high single digit yields we observe at extremely low volatility levels, the opportunity cost of not doing this work is too high.

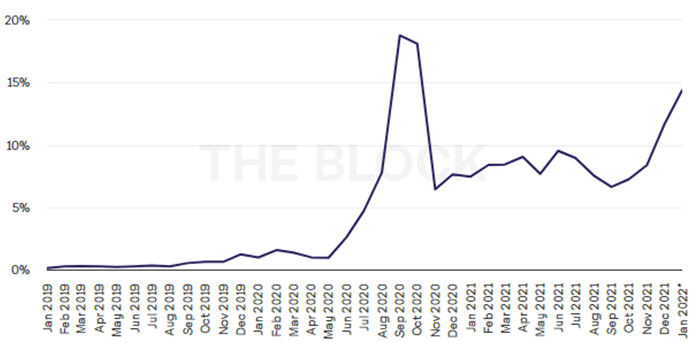

Though decentralized finance platforms continue to take market share in global trading (fig. 4), the vast majority of the world’s banks still won’t touch them. JPMorgan Chase just shut the personal bank account of Uniswap’s founder.8 The result is a shortage of USD in the crypto ecosystem and an attractive risk/return profile in the short-term lending markets. And though some yields have fallen alongside the collapse in Bitcoin futures contango, we expect our fundamental approach to counterparty analysis in this space will continue to produce attractive risk adjusted-returns for our clients.

Fig. 4. Decentralized Exchange to Centralized Exchange Spot Trade Volume (%)

Source: TheBlock, as of 1/28/2022.

Fig. 5. Bitcoin: Futures Annualized Rolling Basis

Source: Glassnode.

To receive more Digital Assets insights, sign up in our subscription center.

DISCLOSURES

Important Information Regarding Cryptocurrencies

VanEck assumes no liability for the content of any linked third-party site, and/or content hosted on external sites.

The information herein represents the opinion of the author(s), an employee of the advisor, but not necessarily those of VanEck. The cryptocurrencies discussed in this material may not be appropriate for all investors. The appropriateness of a particular investment or strategy will depend on an investor’s individual circumstances and objectives.

This material has been prepared for informational purposes only and is not an offer to buy or sell or a solicitation of any offer to buy or sell any cryptocurrencies, or to participate in any trading strategy. Past performance is no guarantee of future results.

Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results, are valid as of the date of this communication and subject to change without notice. Information provided by third party sources are believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. VanEck does not guarantee the accuracy of third party data. References to specific securities and their issuers or sectors are for illustrative purposes only.

Cryptocurrency is a digital representation of value that functions as a medium of exchange, a unit of account, or a store of value, but it does not have legal tender status. Cryptocurrencies are sometimes exchanged for U.S. dollars or other currencies around the world, but they are not generally backed or supported by any government or central bank. Their value is completely derived by market forces of supply and demand, and they are more volatile than traditional currencies. The value of cryptocurrency may be derived from the continued willingness of market participants to exchange fiat currency for cryptocurrency, which may result in the potential for permanent and total loss of value of a particular cryptocurrency should the market for that cryptocurrency disappear. Cryptocurrencies are not covered by either FDIC or SIPC insurance. Legislative and regulatory changes or actions at the state, federal, or international level may adversely affect the use, transfer, exchange, and value of cryptocurrency.

Investing in cryptocurrencies, such as Bitcoin, comes with a number of risks, including volatile market price swings or flash crashes, market manipulation, and cybersecurity risks. In addition, cryptocurrency markets and exchanges are not regulated with the same controls or customer protections available in equity, option, futures, or foreign exchange investing. There is no assurance that a person who accepts a cryptocurrency as payment today will continue to do so in the future.

Investors should conduct extensive research into the legitimacy of each individual cryptocurrency, including its platform, before investing. The features, functions, characteristics, operation, use and other properties of the specific cryptocurrency may be complex, technical, or difficult to understand or evaluate. The cryptocurrency may be vulnerable to attacks on the security, integrity or operation, including attacks using computing power sufficient to overwhelm the normal operation of the cryptocurrency’s blockchain or other underlying technology. Some cryptocurrency transactions will be deemed to be made when recorded on a public ledger, which is not necessarily the date or time that a transaction may have been initiated.

- Investors must have the financial ability, sophistication and willingness to bear the risks of an investment and a potential total loss of their entire investment in cryptocurrency.

- An investment in cryptocurrency is not suitable or desirable for all investors.

- Cryptocurrency has limited operating history or performance.

- Fees and expenses associated with a cryptocurrency investment may be substantial.

There may be risks posed by the lack of regulation for cryptocurrencies and any future regulatory developments could affect the viability and expansion of the use of cryptocurrencies. Investors should conduct extensive research before investing in cryptocurrencies.

1 Decentralized finance (DeFi) protocols are software programs that run on top of another cryptocurrency as a means to automate a financial service without a centralized institution.

2 Cash and carry is an arbitrage strategy that involves the mispricing between a futures contract and its underlying asset.

3 Contango is a scenario in which the futures price of a commodity is higher than the spot price.

4 Glassnode, 365-day moving average as of 1/27/22.

5 VanEck research.

6 The Block “Crypto trader Tantra to liquidate”.

7 Source: latest filings, Coinbase full year 2020, JPMorgan full year 2021. JPMorgan’s 2020 ROA was 97bps.

8 Source: Twitter, 1/23/2022 update by user @haydenzadams.

Information provided by Van Eck is not intended to be, nor should it be construed as financial, tax or legal advice. It is not a recommendation to buy or sell an interest in cryptocurrencies.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.

Related Funds

DISCLOSURES

Important Information Regarding Cryptocurrencies

VanEck assumes no liability for the content of any linked third-party site, and/or content hosted on external sites.

The information herein represents the opinion of the author(s), an employee of the advisor, but not necessarily those of VanEck. The cryptocurrencies discussed in this material may not be appropriate for all investors. The appropriateness of a particular investment or strategy will depend on an investor’s individual circumstances and objectives.

This material has been prepared for informational purposes only and is not an offer to buy or sell or a solicitation of any offer to buy or sell any cryptocurrencies, or to participate in any trading strategy. Past performance is no guarantee of future results.

Certain statements contained herein may constitute projections, forecasts and other forward looking statements, which do not reflect actual results, are valid as of the date of this communication and subject to change without notice. Information provided by third party sources are believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. VanEck does not guarantee the accuracy of third party data. References to specific securities and their issuers or sectors are for illustrative purposes only.

Cryptocurrency is a digital representation of value that functions as a medium of exchange, a unit of account, or a store of value, but it does not have legal tender status. Cryptocurrencies are sometimes exchanged for U.S. dollars or other currencies around the world, but they are not generally backed or supported by any government or central bank. Their value is completely derived by market forces of supply and demand, and they are more volatile than traditional currencies. The value of cryptocurrency may be derived from the continued willingness of market participants to exchange fiat currency for cryptocurrency, which may result in the potential for permanent and total loss of value of a particular cryptocurrency should the market for that cryptocurrency disappear. Cryptocurrencies are not covered by either FDIC or SIPC insurance. Legislative and regulatory changes or actions at the state, federal, or international level may adversely affect the use, transfer, exchange, and value of cryptocurrency.

Investing in cryptocurrencies, such as Bitcoin, comes with a number of risks, including volatile market price swings or flash crashes, market manipulation, and cybersecurity risks. In addition, cryptocurrency markets and exchanges are not regulated with the same controls or customer protections available in equity, option, futures, or foreign exchange investing. There is no assurance that a person who accepts a cryptocurrency as payment today will continue to do so in the future.

Investors should conduct extensive research into the legitimacy of each individual cryptocurrency, including its platform, before investing. The features, functions, characteristics, operation, use and other properties of the specific cryptocurrency may be complex, technical, or difficult to understand or evaluate. The cryptocurrency may be vulnerable to attacks on the security, integrity or operation, including attacks using computing power sufficient to overwhelm the normal operation of the cryptocurrency’s blockchain or other underlying technology. Some cryptocurrency transactions will be deemed to be made when recorded on a public ledger, which is not necessarily the date or time that a transaction may have been initiated.

- Investors must have the financial ability, sophistication and willingness to bear the risks of an investment and a potential total loss of their entire investment in cryptocurrency.

- An investment in cryptocurrency is not suitable or desirable for all investors.

- Cryptocurrency has limited operating history or performance.

- Fees and expenses associated with a cryptocurrency investment may be substantial.

There may be risks posed by the lack of regulation for cryptocurrencies and any future regulatory developments could affect the viability and expansion of the use of cryptocurrencies. Investors should conduct extensive research before investing in cryptocurrencies.

1 Decentralized finance (DeFi) protocols are software programs that run on top of another cryptocurrency as a means to automate a financial service without a centralized institution.

2 Cash and carry is an arbitrage strategy that involves the mispricing between a futures contract and its underlying asset.

3 Contango is a scenario in which the futures price of a commodity is higher than the spot price.

4 Glassnode, 365-day moving average as of 1/27/22.

5 VanEck research.

6 The Block “Crypto trader Tantra to liquidate”.

7 Source: latest filings, Coinbase full year 2020, JPMorgan full year 2021. JPMorgan’s 2020 ROA was 97bps.

8 Source: Twitter, 1/23/2022 update by user @haydenzadams.

Information provided by Van Eck is not intended to be, nor should it be construed as financial, tax or legal advice. It is not a recommendation to buy or sell an interest in cryptocurrencies.

All investing is subject to risk, including the possible loss of the money you invest. As with any investment strategy, there is no guarantee that investment objectives will be met and investors may lose money. Diversification does not ensure a profit or protect against a loss in a declining market. Past performance is no guarantee of future results.