Welcome to VanEck

Select Investor Type

03 December 2019

High yield emerging markets corporate bonds have had a solid year so far, against a backdrop of stable credit fundamentals and low default rates. Breaking down the sources of year-to-date returns, we believe that, in an environment of continued global growth and accommodative monetary policy, the asset class may continue to perform well as we look ahead to 2020.

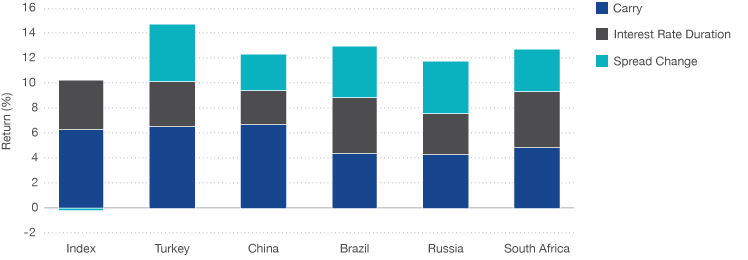

Top contributors to performance of the ICE BofAML Diversified High Yield US Emerging Markets Corporate Plus Index this year, in terms of country of issuer, include many of the countries with the highest weightings. With positive fundamentals in Russia and the prospect of structural reforms in Brazil, these countries are, not surprisingly, among the top contributors this year. Perhaps more surprising is that China, Turkey and South Africa are also outperforming, given the various domestic and geopolitical issues impacting those countries.

What explains the outperformance of the issuers from these countries? In some cases, such as China and Turkey, it reflects a recovery following last year’s underperformance. Tighter credit spreads among Chinese, Turkish, Brazilian, Russian and South African companies have contributed significantly to performance, but spread movements on the index overall have had a neutral return impact. Carry, with yields in excess of 7%, explains the majority of this year’s returns overall, followed by duration given the decline in U.S. interest rates over the year.1 The nearly 150 basis point spread pickup by the asset class above U.S. high yield, as represented by ICE BofAML US High Yield Index, suggests that emerging markets high yield bonds could benefit from upside growth scenarios in China, and globally, in 2020.2

Source: FactSet as of 31/10/2019.

Finally, the differences between equity and high yield returns within countries is significant in many cases. For example, Turkish high yield corporates have returned nearly 15% this year, compared to equity returns of less than 2%. South African high yield has returned approximately 13%, versus nearly flat equity returns. In contrast, Russian high yield bonds have returned approximately 12%, significantly lagging equities.3 These differences underscore the diversification benefits that emerging markets high yield corporate bonds can provide within a broader emerging markets portfolio.

1Source: ICE Data Indices. Data as of 31/10/2019.

2Source: ICE Data Indices. Data as of 31/10/2019.

3Source: FactSet and Morningstar, as of 31/10/2019.

This is a marketing communication. Please refer to the prospectus of the UCITS and to the KID before making any final investment decisions.

This information originates from VanEck Switzerland AG which has been appointed as distributor of VanEck products in Switzerland by the Management Company VanEck Asset Management B.V., incorporated under Dutch law and registered with the Dutch Authority for the Financial Markets (AFM). VanEck Switzerland AG’s registered address is at Genferstrasse 21, 8002 Zürich, Switzerland.

The information is intended only to provide general and preliminary information to investors and shall not be construed as investment, legal or tax advice. VanEck Switzerland AG and its associated and affiliated companies (together “VanEck”) assume no liability with regards to any investment, divestment or retention decision taken by the investor on the basis of this information. The views and opinions expressed are those of the author(s) but not necessarily those of VanEck. Opinions are current as of the publication date and are subject to change with market conditions. Certain statements contained herein may constitute projections, forecasts and other forward-looking statements, which do not reflect actual results. Information provided by third party sources is believed to be reliable and have not been independently verified for accuracy or completeness and cannot be guaranteed. Brokerage or transaction fees may apply. A copy of the latest prospectus, the Articles, the Key Information Document, the annual report and semi-annual report can be found on our website www.vaneck.com or can be obtained free of charge from the representative in Switzerland: First Independent Fund Services Ltd, Feldeggstrasse 12, 8008 Zurich, Switzerland. Swiss paying agent: Helvetische Bank AG, Seefeldstrasse 215, CH-8008 Zürich.

All performance information is based on historical data and does not predict future returns. Investing is subject to risk, including the possible loss of principal.

No part of this material may be reproduced in any form, or referred to in any other publication, without express written permission of VanEck.

© VanEck Switzerland AG

11 December 2025

11 December 2025